In a detailed analysis of the Reserve Bank of Australia’s (RBA) latest Statement of Monetary Policy, CBA Economics’ Gareth Aird and Stephen Wu explain why the RBA is unlikely to hike again this cycle.

The CBA’s view is based on its take of the RBA’s reaction function.

In short, the the economic data will need to print stronger than the RBA’s updated forecasts for them to increase the cash rate again, which the CBA views as unlikely.

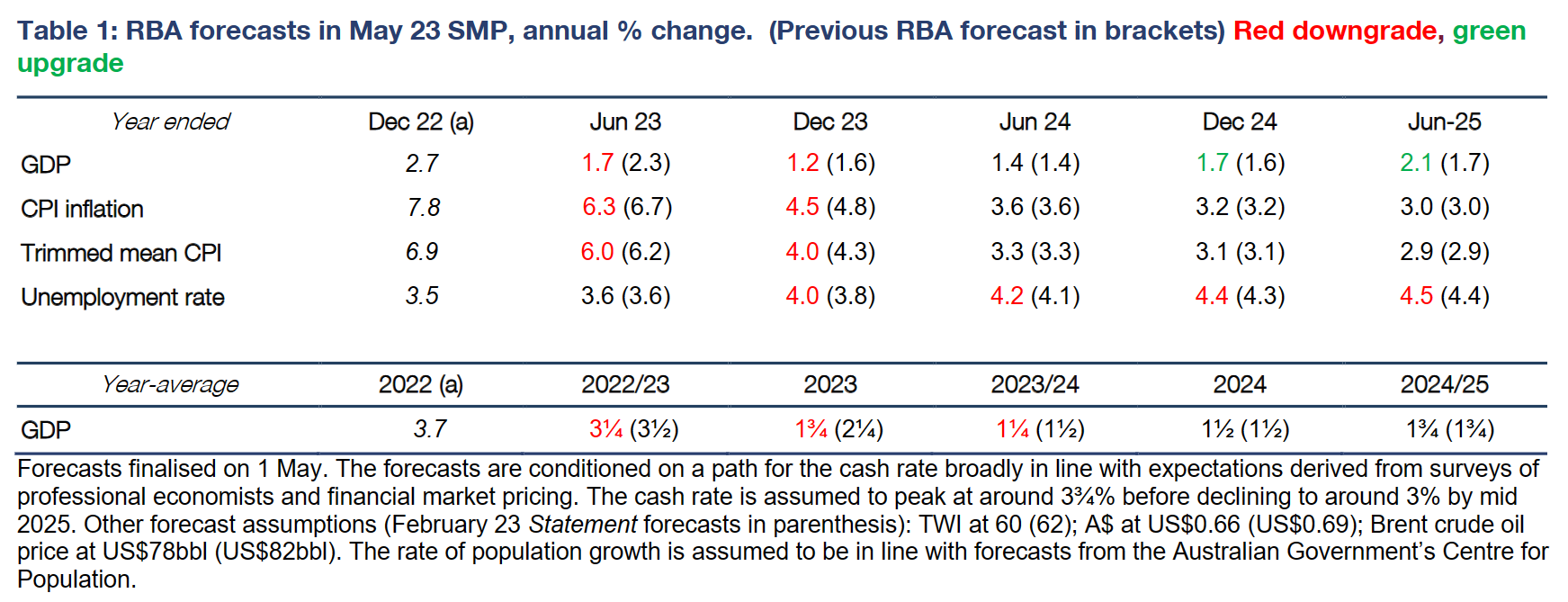

- The RBA has downwardly revised their near term forecasts for inflation but retained their inflation forecasts in2024 and 2025.

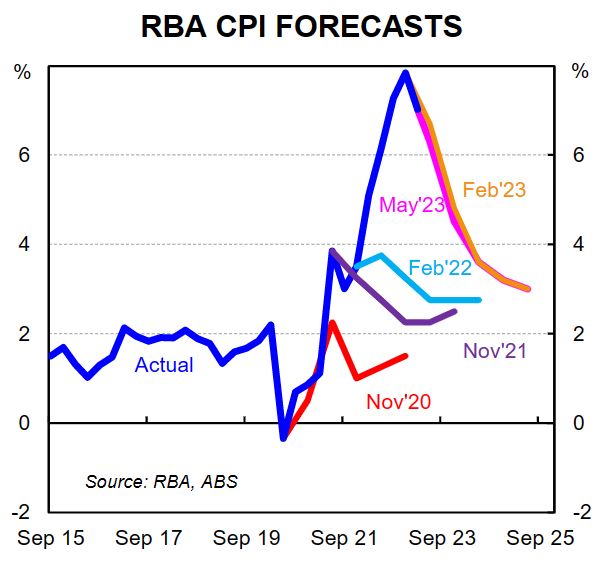

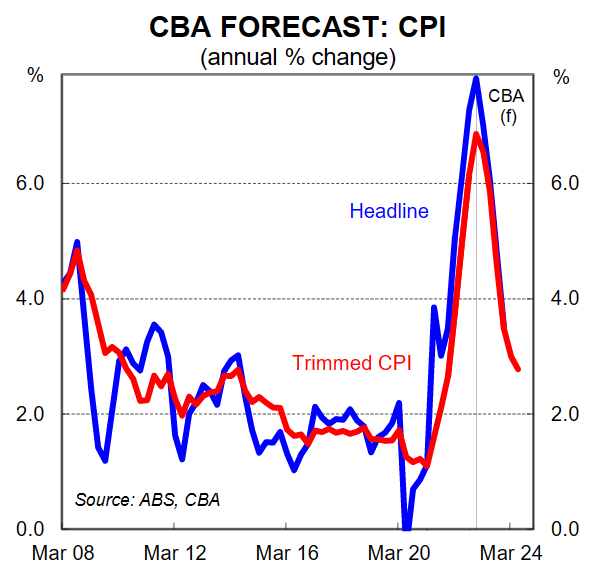

- The RBA expects annual inflation to be 4.5% in Q4 23 and 3.2% in Q4 24. Inflation does not return to the top of the target band on the RBA’s forecasts until Q2 25.

- The annual rate of underlying inflation is forecast to be 4.0% in Q4 23 and 3.1% in Q4 24.

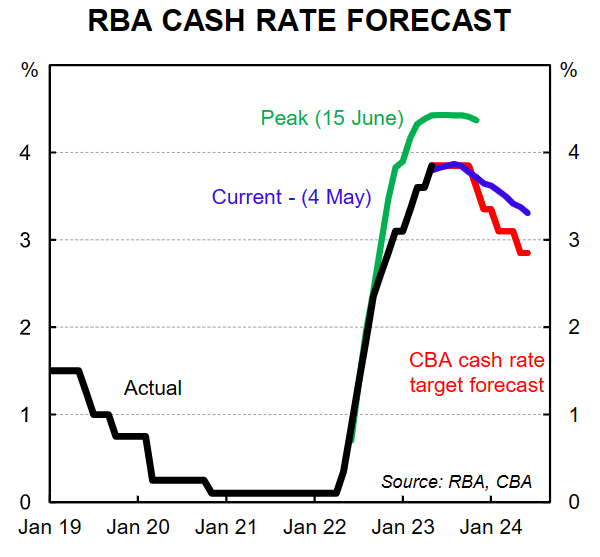

- The RBA’s forecasts assume a peak in the cash rate of around 3¾% (the cash rate target is currently 3.85%).

- The RBA have downwardly revised their 2023 GDP forecast to 1.2%/yr in Q4 23 (from 1.6%/yr previously). An upward revision to their population growth assumption implies a GDP per capita recession (now in line with the CBA view).

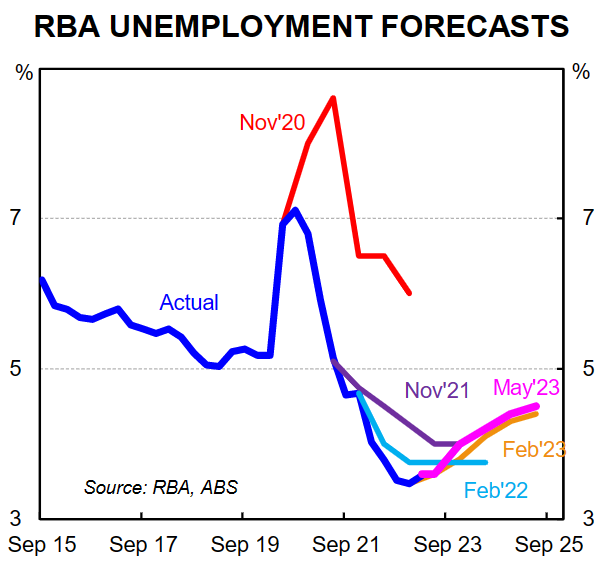

- The GDP downgrade has resulted in an upward revision to the RBA’s profile for the unemployment rate – the RBA expects the unemployment rate to be 4.0% in Q4 23 (from 3.8% previously) and 4.4% in Q4 24 (we forecast the unemployment rate to be4.2% in Q4 23).

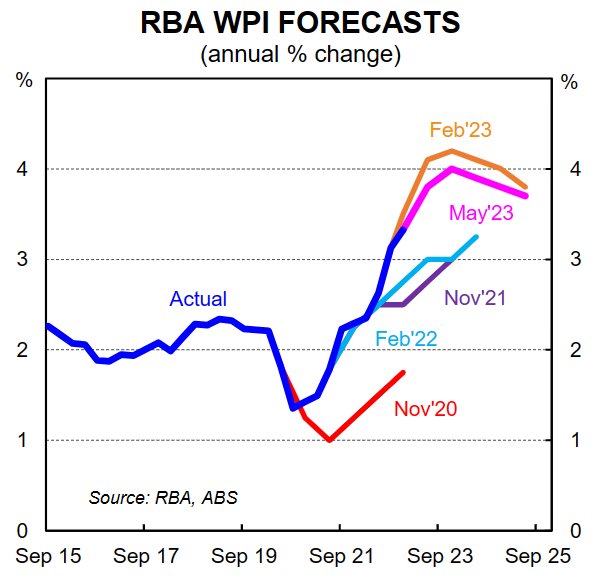

- The RBA have made as light downward revision to their forecasts for annual wages growth and expect it to be peak at 4.0% in Q4 23 (from 4.2% previously) before edging lower to be 3.8% in Q4 24 (we forecast wages growth to peak at 3.8%/yr).

The RBA’s updated forecasts should mean that 3.85% is the peak in the cash rate

The RBA’s May Statement on Monetary Policy (SMP) comes in the wake of the 25bp rate hike at the May Board meeting, which took the cash rate to 3.85%.

We expected the RBA to raise the cash rate at the May Board meeting. But the decision was not anticipated by financial markets or the majority of the forecasting community.

For context, money markets had priced a negligible ~12% chance of a 25bp rate increase in May.

Key to our call for the Board to hike the cash rate in May was the expectation that the RBA would leave their forecast for inflation to only return to the top of the target band by mid-2025 unchanged.

The Governor’s Statement accompanying the May Board decision confirmed that the RBA kept that 2025 inflation profile intact. But there was a lack of detail on the RBA’s assessment on the near term trajectory for inflation.

The May SMP provides this detail as it tables the key semi-annual point forecasts to the RBA’s inflation profile to mid-2025. The May SMP also provides updated point forecasts for GDP, wages growth and the unemployment rate.

These point forecasts are all important as they provide markers in which we can assess if the economic data is printing stronger, weaker, or in line with the RBA’s expectations over 2023.

By extension there are implications for the near term monetary policy outlook depending on how the data evolves.

In the Governor’s Statement accompanying the May Board decision it was stated that, “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon how the economy and inflation evolve”(our emphasis in bold).

This line was repeated in the Governor’s speech at the Board Dinner on Tuesday evening. And it appeared again today in the SMP.

Our take on this important forward guidance is that the Board is willing to raise the cash rate again in this cycle. But another rate increase would require the economic data, particularly around inflation, GDP, the unemployment rate and wages, to come in stronger than their updated forecasts.

Put another way, we do not think the RBA will lift the cash rate again if the economic data print in line or weaker than their forecasts.

The near term forecasts are very important for markets

The RBA’s forecast for headline CPI to be 6.3%/yr in Q2 23 means that the RBA expects a 1.1%/qtr outcome in Q2 23.

For trimmed mean inflation the RBA has forecast 6.0%/yr in Q2 23 which means the RBA expects a 1.1%/qtr outcome.

We do not expect Q2 23 CPI to print stronger than the RBA’s forecasts which is why we have no further rate hikes in our profile.

But a near term rate hike remains the risk given the actual outcomes could come in stronger than the RBA’s forecasts –we don’t think there is a lot of wriggle room and our current forecastforQ2 23 trimmed mean CPI is0.9%/qtr and 5.9%/yr.

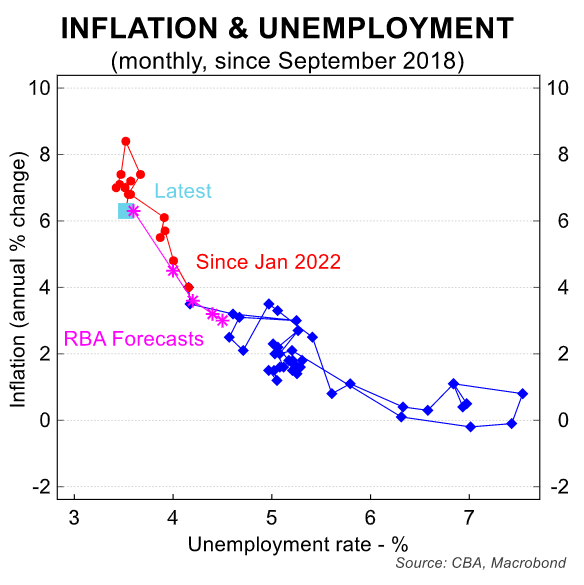

On the unemployment rate the RBA has forecast it to average 3.6% over Q2 23. The unemployment rate was 3.5% in March 2023. So the RBA is not expecting the labour market to loosen much on that measure alone over the next few months.

We broadly agree with that assessment. But we expect to see other measures of the labour market loosen. More specifically we anticipate job advertisements to continue to trend down and for the underemployment rate to drift higher.

Some workers will seek additional hours to cover higher rent or higher mortgage repayments as well as the general increase in the cost of living.

The bigger picture

We expect the economy to slow more quickly than the RBA does from here. The RBA forecasts GDP growth to be 1.2%/yr in Q4 23. In contrast we see GDP growth at 0.9%/yr in Q4 23. Both the CBA and RBA forecasts for GDP in 2023 imply a per capita recession given population growth will soon be 2.0%/yr.

Our expectation for growth to be softer than the RBA means we forecast the unemployment rate to rise a little more quickly.

Indeed the RBA’s forecast for the unemployment rate to get to 4.2% by mid-2024 looks too optimistic to us. We forecast it will reach that level by the end of 2023.

To be clear, these are both still low unemployment rates in a historical context. The unemployment rate was 5.2% on the eve of the pandemic. But we do have a slightly different take on the economic outlook.

Put simply, we think that the lagged impact of the already delivered rate rises will slow the consumer and by extension aggregate demand in the economy by more than the RBA does.

This view also leads us to expect inflation to recede more quickly than the RBA. And we forecast wages growth, as measured by the wage price index (WPI), to peak at 3.8%/yr, compared with the RBA’s forecast of a peak in wages growth of 4.0%/yr.

Note that the RBA’s liaison has indicated wages growth expectations for the next 12 months have moderated over recent months (see section below).

The global backdrop matters

The RBA views the global backdrop as having improved from three months prior.

Growth in Australia’s major trading partners (MTP) has been upgraded a touch, but is still expected to remain well below its pre-pandemic average.

While global inflation has fallen, progress towards returning to many central banks’ inflation targets has slowed.

The concern is that services inflation could prove stickier than otherwise thought – something that Governor Lowe had mentioned in his post-meeting Statement accompanying the May decision.

The RBA does not produce their own forecasts for most other economies; instead it simply takes the consensus of market economists’ forecasts. It does, however, produce in-house forecasts for China –our largest trading partner – so it’s worth exploring how their assessment on China has shifted.

The RBA has upwardly revised their forecast for China’s economic growth. Growth is forecast to ‘comfortably exceed’ the Chinese authorities’ growth target of around 5%.

The RBA cites the smaller-than-expected disruption over late 2022 to the Chinese economy from pandemic restrictions as a key driver of the upward revision.

Risks to the Chinese economic outlook are seen to be balanced. On one hand, goods demand in China remains weak and household consumption could well stall after the initial rebound.

There could also be a larger-than-expected slowdown in economic growth in some of China’s export markets.

On the other hand, more supportive fiscal policy and a turnaround in the Chinese property market could instead support stronger domestic economic outcomes.

Financial stability concerns emanating from the US banking system are judged to have subsided. And the RBA views the contagion risks to be low given Australia’s well regulated banking system (more detail can be found in the RBA’s April Financial Stability Review).

Nevertheless, these global financial risks are a key source of uncertainty and, if these risks were to flare up again, could impact Australia’s exports, consumption and investment.

RBA business liaison insights

Since November last year, the RBA has released a summary of insights derived from their business liaison program in each of their quarterly Statements. The key takeaways from the ~225 contacts interviewed each quarter (70-80 a month) are:

Increasing pressures on household budgets have meant spending has slowed and a rising number of households are turning to community services for assistance.

Households are increasingly trading down to cheaper products, purchasing fewer items, and this has been most pronounced in lower-income areas. But domestic tourism demand remains strong.

We think this reflects the disparate strength of household balance sheets across age demographics, where older Australians –particularly those without mortgage debt, have not been as affected by rising interest rates.

Business investment intentions have pared back a little recently because of heightened uncertainty. By sector, activity in residential construction is expected to fall once the current backlog is worked through.

In contrast, education and tourism exports are expected to rise further.

Expectations for wages growth over the year ahead have moderated over recent months. This reflects a combination of lower job turnover, improving labour supply from the lift in population growth, easing labour demand, slowing business conditions and increased internal focus on cost control.

This information has likely influenced the RBA’s downgrade of their wages profile. However, many businesses are uncertain around how the national minimum wage will increase this year.

The Fair Work Commission will hand down their decision in mid to late June.

Businesses’ input cost growth has moderated in line with lower shipping costs, slower global demand. But domestic costs could remain elevated owing to higher labour costs.

Reflecting this, businesses expect inflation to moderate gradually. Goods retailers see price declines while other services firms anticipate further price increases.

The outlook for the cash rate

From a monetary policy perspective we think that the RBA will not hike the cash rate again in this cycle. This is simply based on our take of the Board’s reaction function from here.

That is, the economic data will need to print stronger than the RBA’s updated forecasts for them to increase the cash rate again. And that is not our base case.

But no economist has a crystal ball and the data could surprise to the upside, particularly given the housing market is showing signs of renewed strength.

As such, the near term risk sits with another rate increase and markets should be aware of this.

Looking further ahead our base case sees the RBA commence an easing cycle in late 2023.

Monetary policy works with a lag in both directions. And we think that with inflation receding more quickly than the RBA expects and unemployment rising more quickly the Board will want to take the cash rate down from a deeply restrictive setting to keep the economy ‘on an even keel’ in 2024.

The runway of course is getting shorter. And if the data holds up a bit firmer than we expect the easing cycle is more likely to start in Q1 24.

We also don’t know the Board’s reaction function to ease policy.

Our working assumption is that the annual rate of inflation does not need to return to target before the RBA cuts the cash rate. Rather we think a six month annualised pace of inflation that is close to target would be sufficient for the Board to ease policy given inflation is a lagging indicator.

Overall we are looking for 125bp of policy easing by end-2024 that would take the cash rate to ~2.5%.