The greatest construction boom in history is over and iron ore is yet to fully realise it.

Goldman describes the obvious:

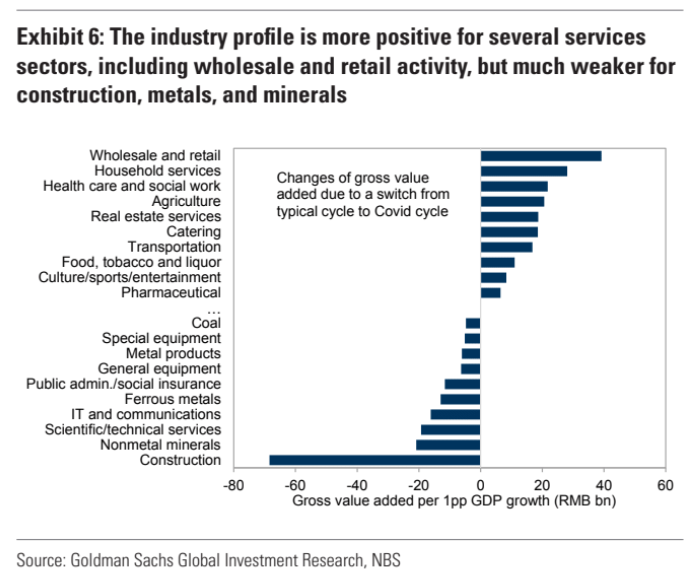

China’s current economic recovery has been concentrated in the services sector, as expected. Around the world, Covid restrictions typically disrupted services(consumption) more than goods, so the subsequent post-Covid “reopening recoveries” have been services-centric as well. In contrast, China’s historical economic recoveries have been driven more by investment.

…in terms of international spillovers, a consumer services-led recovery induces only about 1/3 as much goods imports as a typical investment-led recovery. Given a significant fraction of China’s imports are raw materials, this also has implications for commodity demand.

The activity is there meaning no need for stimulus. It’s just not construction.

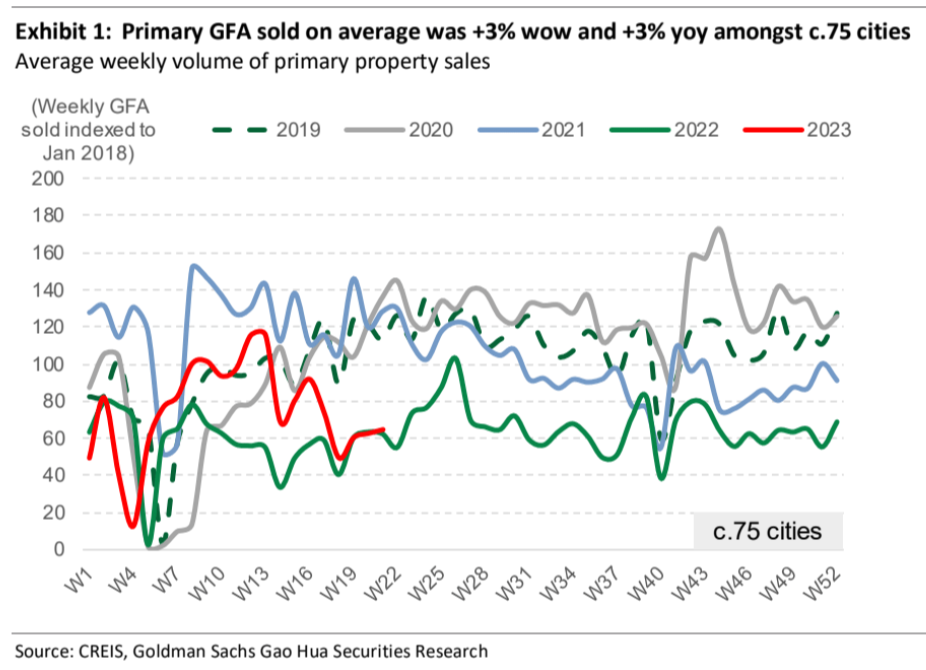

The property market is the core of the weakness. The sales recovery is all but over:

Advertisement

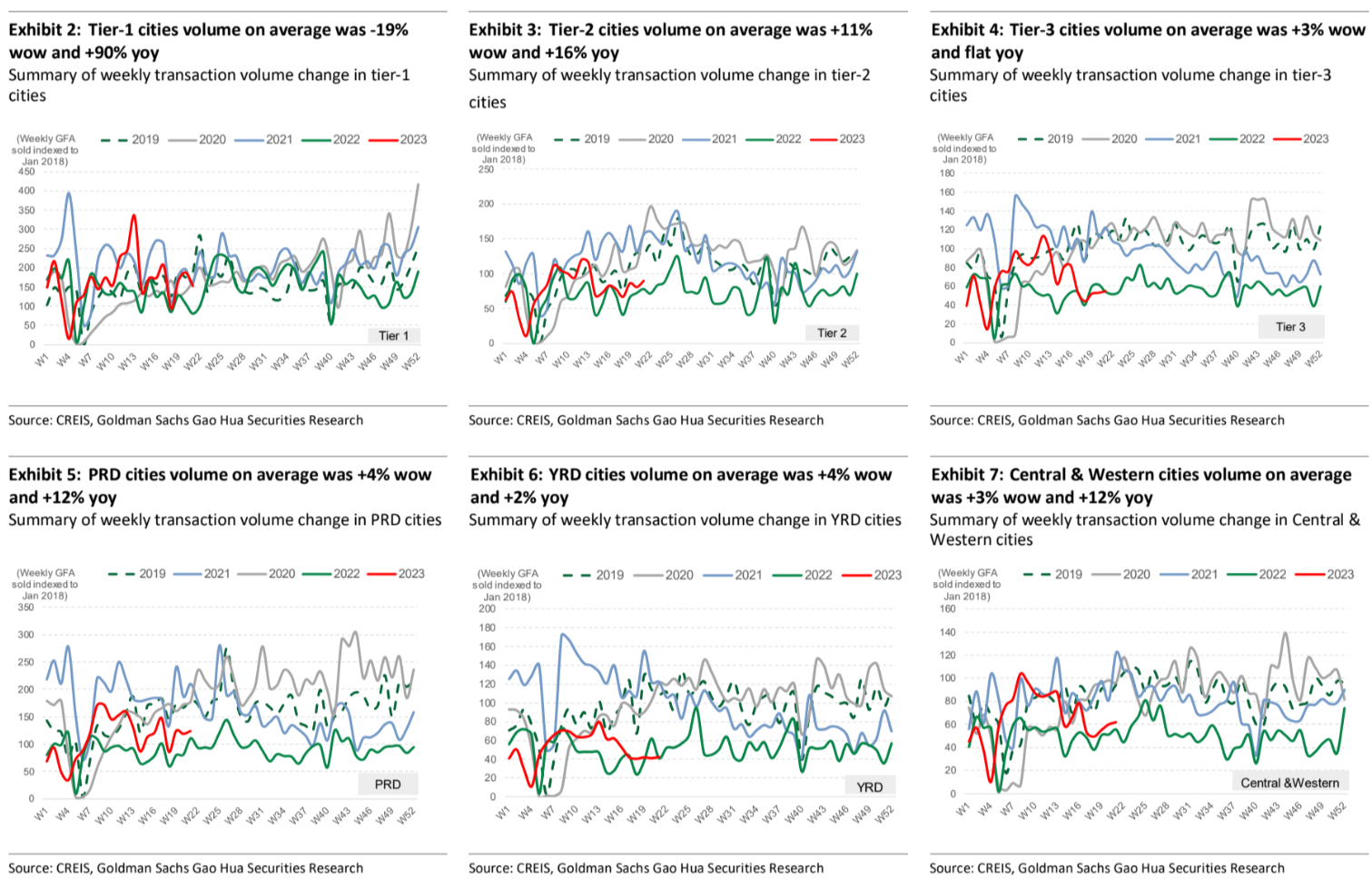

Ghost cities are so yesterday. The further from civilisation you are, the worse it gets:

Advertisement

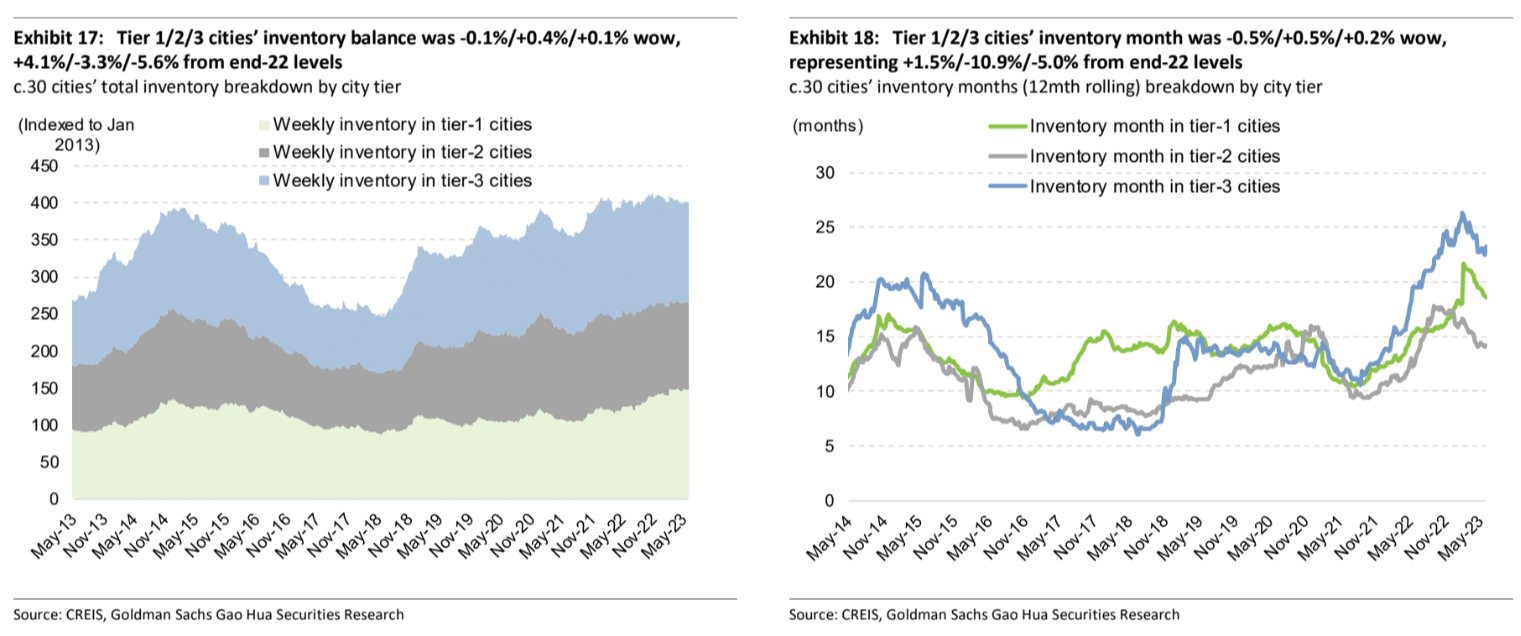

There is two years of inventory!

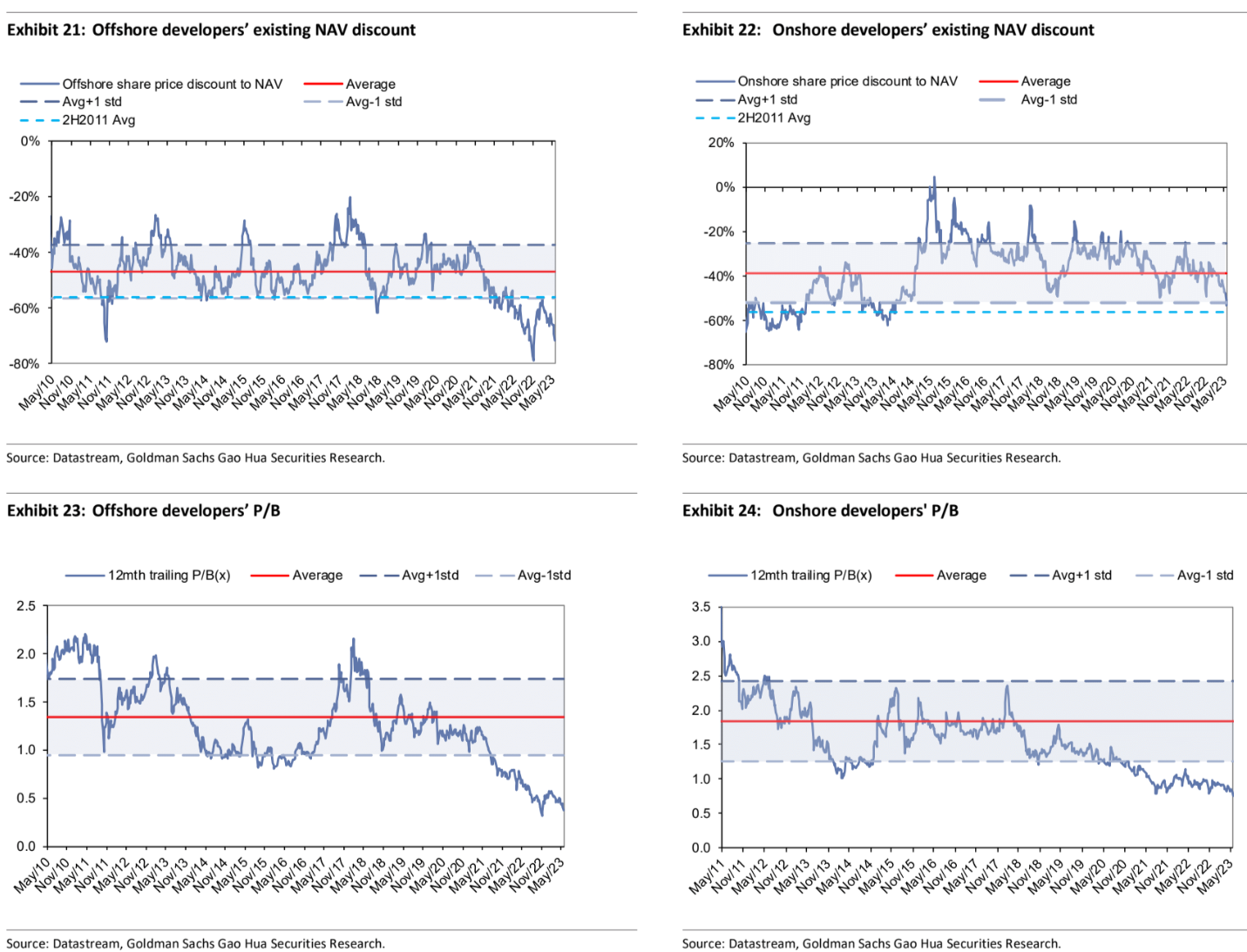

The equity market is screaming that it is all over:

Advertisement

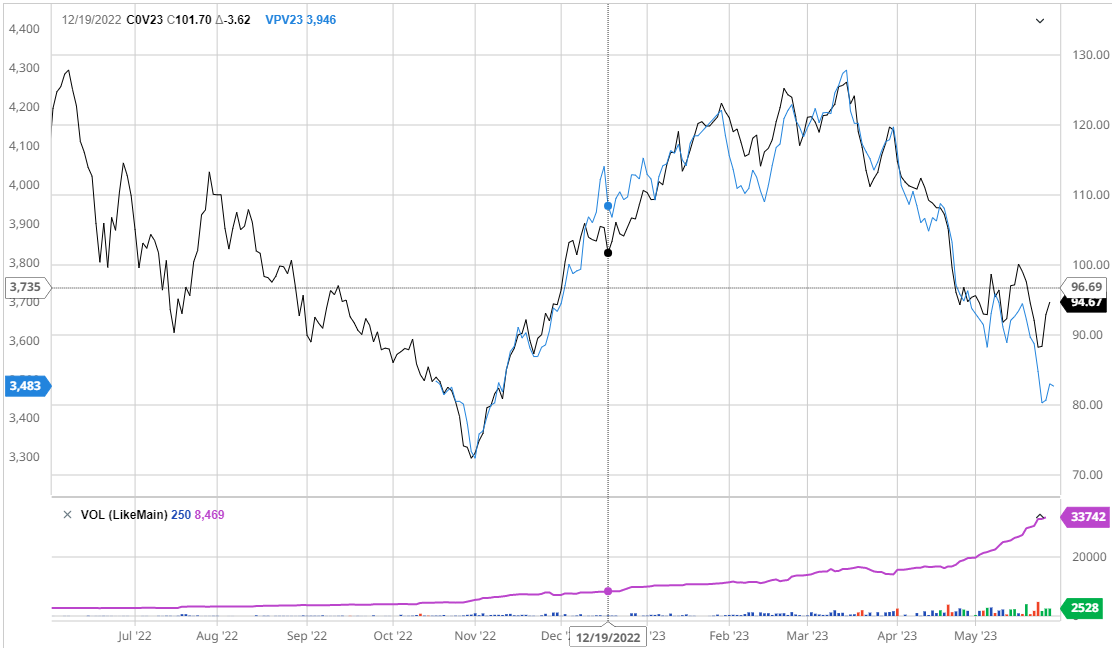

Steel mills are low on iron ore stocks so there’ll be price pops from time to time:

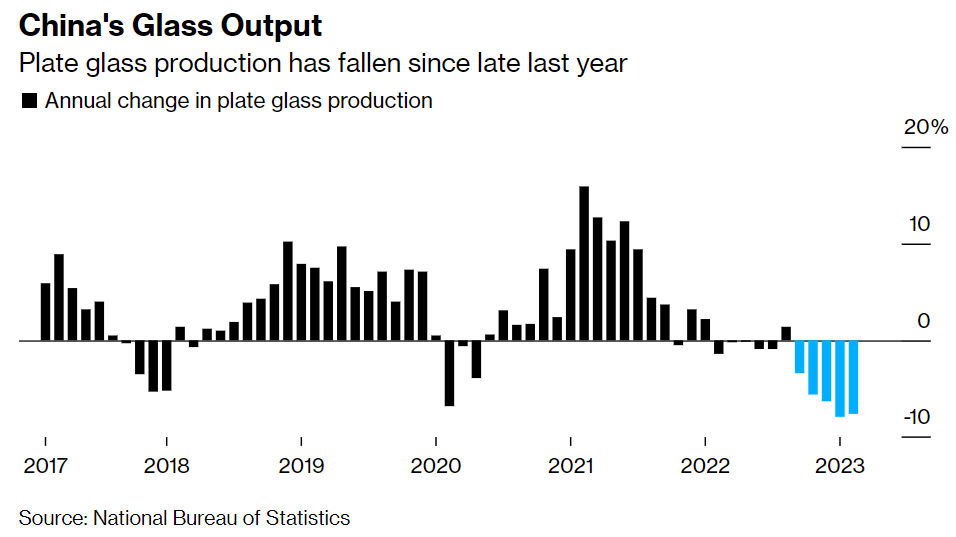

But underlying demand is only going to get worse and you can’t fight gravity forever as fewer and fewer shiny steel towers are erected:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.