Over the holiday break, the International Monetary Fund (IMF) released a report entitled Housing Market Stability and Affordability in Asia-Pacific, which warned that New Zealand has one of the most “misaligned” housing markets in the world, thus leaving the nation exposed to a price crash.

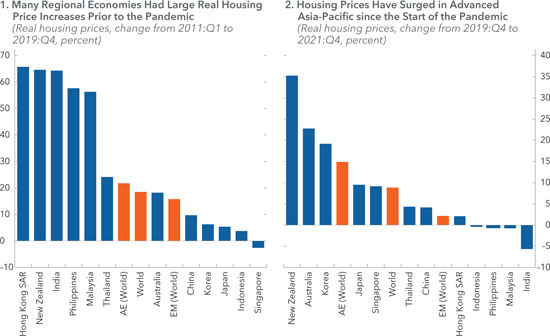

The next chart shows that New Zealand experienced the second largest real house price appreciation in the Asia-Pacific region between 2011 and 2019, as well as by far the strongest price growth over the pandemic:

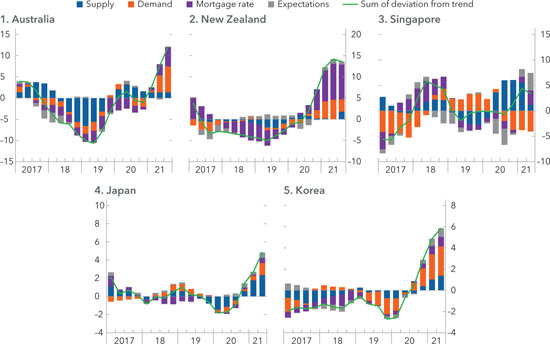

Low mortgage rates have been the primary driver of New Zealand’s extreme house price growth, according to the IMF:

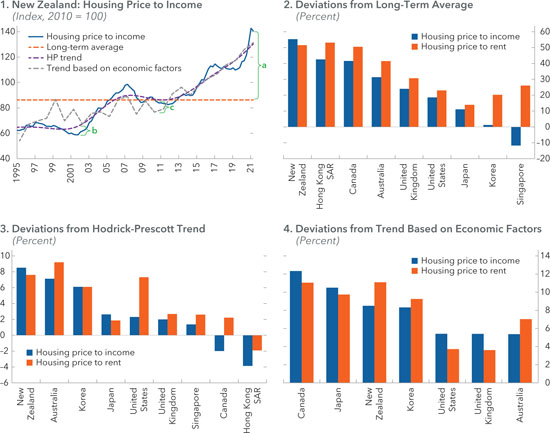

And this extreme price growth has left New Zealand housing particularly misaligned with incomes and rents:

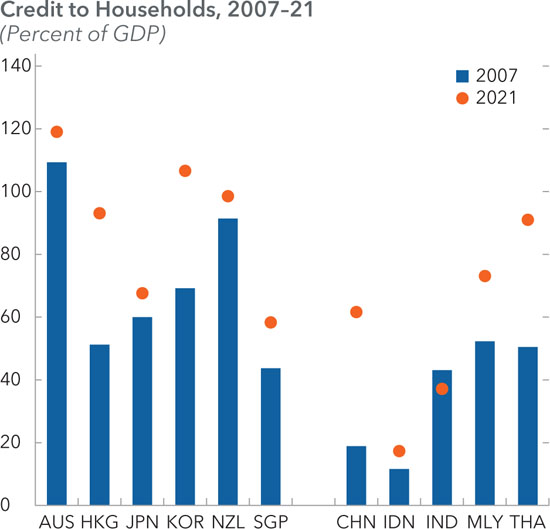

New Zealand households are also highly leveraged compared with their Asia-Pacific peers, albeit less so than Australians:

The IMF explicitly warns that “misalignment in housing prices, combined with the expected rise in interest rates as central banks normalize monetary policy, suggests a significant risk of a correction in housing prices”.

“Rising interest rates going forward will add to downside price risks… With interest rates rising significantly in 2022, and with more hikes expected going forward, higher interest rates will add even further to downside risks to housing price growth”.

New Zealand house prices declined by 13.7% in the year to November 2022, according to the REINZ House Price Index, which takes into account changes in the mix of properties sold each month.

Meanwhile, the Reserve Bank of New Zealand has forecast a recession in 2023, a further increase in the official cash rate to 5.5% (from 4.25% currently), alongside a 20% peak-to-trough decline in house prices.

New Zealand led the global house price boom over the pandemic. Now it is leading the bust on the back of the Reserve Bank’s ultra-aggressive monetary tightening.