It is an idea gathering some fans. Goldman is pushing it as part of its soft landing scenario for the US. TSLombard is mulling it today as well. Not my base case, still, the further the reflation rally gets, the more it comes into focus.

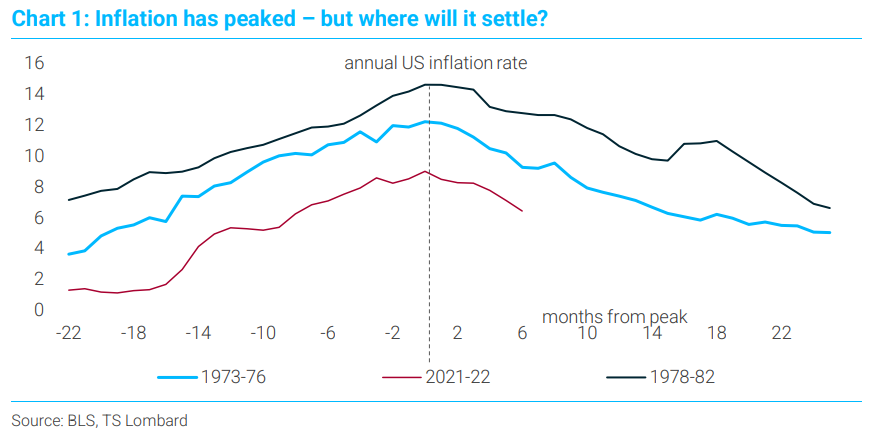

If we had to summarize 2022 in one word, “stagflation” surely fits the bill. Inflation hit 40-year highs, global growth unexpectedly stalled and central banks, fearing a nightmare return to the 1970s, tightened policy at an unprecedented pace. This combination of events created an extremely toxic environment for markets. Looking ahead, the big question for 2023 is whether the stagflationary impulse continues or whether – either through good luck or successful policy – central banks can put inflation back onto a more benign trajectory without triggering a gutwrenching recession. In terms of the short-term CPI outlook, there are good reasons why the “peak inflation” narrative is gaining traction. Food and energy prices have fallen significantly since the summer, while weaker manufacturing demand combined with normalization in global supply chains could deliver broad-based declines in “core” good prices through 2023. With a bit of luck, headline inflation rates could drop even faster than the consensus expects, providing great relief for policymakers. Yet there is still a lot that could go wrong. The peak inflation narrative is particularly vulnerable to further supply shocks, which puts investors in an uncomfortable position given the continued war in Ukraine, the risk of further problems in European energy markets, and China’s determination to drop its COVID restrictions faster than analysts expected.

While lower inflation would ease part of the 2022 stagflationary impulse, there is a widespread belief that it will have to come at the cost of even weaker economic growth. Indeed, the consensus sees a further deterioration in the global economy in 2023, with most economists now expecting mild recessions in the US and across much of the developed world. On one level, these gloomy predictions make sense. Global growth has stalled, most leading indicators continue to deteriorate, and yield curves are deeply inverted – which are all classic recession markers. Also, central banks have tightened monetary policy aggressively and such actions usually come with “long and variable lags”, which means it can take time – up to 18 months – for their full impact of to reach the economy. Investors should watch property markets particularly closely, because a housing crash is the most likely catalyst for a broader and deeper economic contraction. But it is also important to remember that we are not living through a normal business cycle. With postCOVID distortions and the war in Ukraine amplifying the weakness in global manufacturing, traditional leading indicators seem be exaggerating the cyclical risks to the world economy. And we should not forget that high inflation has itself become a source of economic pain. If inflation evaporates, even temporarily, real incomes will rebound and the world economy could prove far more resilient than the consensus expects, especially with faster nominal wages.