Stuff.co.nz’s Miriam Bell has done a terrific job summarising the budding New Zealand housing crash, which has seen house prices and sales collapse at their fastest pace in decades.

The key headline is the 13.7% decline recorded by the Real Estate Institute of New Zealand’s (REINZ) House Price Index, which takes into account changes in the mix of properties sold each month.

“Wellington prices have fallen 20.8% from the peak, Auckland’s are down 18.4%, and there has been some decline in every region”, according to Bell. In turn, “the national median price at $810,000 in November, down from $925,000 at the same time last year”.

Forecasts of how far New Zealand house prices will fall vary, with ASB leading the pack tipping a 25% decline from peak (-40% adjusted for inflation). This is followed by -22% for ANZ (-32% adjusted for inflation), -21% for Kiwibank and Westpac, and -20% for CoreLogic and the Reserve Bank.

Property sales volumes have similarly collapsed to only 67,000 this year, which is the lowest number of sales since 2010 and the third lowest yearly figure in three decades.

At the other end of the spectrum, there were 28,449 properties listed on the market nationwide in November, which was 48% higher than the same time last year.

Hence, New Zealand has significantly fewer buyers chasing a far higher number of properties for sale.

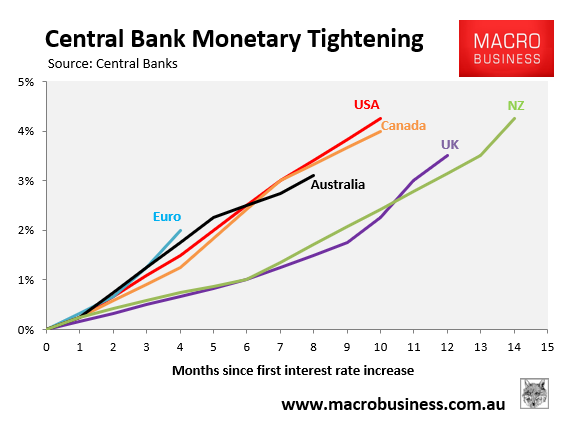

The key factor driving the collapse in prices and sales is obviously the Reserve Bank’s world-beating monetary tightening, which has lifted the official cash rate to 4.25%, with further rises to 5.5% expected in 2023:

New Zealand leads interest rate race.

According to Miriam Bell, “this year’s story has been one of record price falls, a wary buyer pool with FOOP (fear of over-paying) rather than FOMO (fear of missing out), and slow sales”.

“Rates had already climbed from around 2.5% last year to around 6.5%. But, since then, many banks have raised them again”.

“Now, some fixed term rates are nudging 7%, or above it, and floating rates are around 8%, and borrowers are wondering how much higher they could go”.

New Zealand led the global house price boom over the pandemic. Now it is leading the bust on the back of the Reserve Bank’s uber aggressive tightening.

The timing could not be worse for Prime Minister Jacinda Ardern, who will head to the polls late next year with Kiwi households experiencing severe mortgage pain, drowning in negative equity, and the economy likely in recession.