TS Lombard with the note:

2022 fundamental drivers

1. Developed markets put Covid containment behind them. The year 2020 was dominated by Covid containment and 2021 by vaccines and hopes of reopening, but 2022 was the year that DMs put the virus behind them. Now it seems unreal, but at the beginning of 2022, many were worried about further lockdowns on the back of the new Omicron variant. It turned out that the new variant and its high infectivity/low morbidity characteristics were a sign that the pandemic as we knew it was coming to an end. Lockdown and its clamp on growth were over, releasing two years of pent-up demand into the economy.

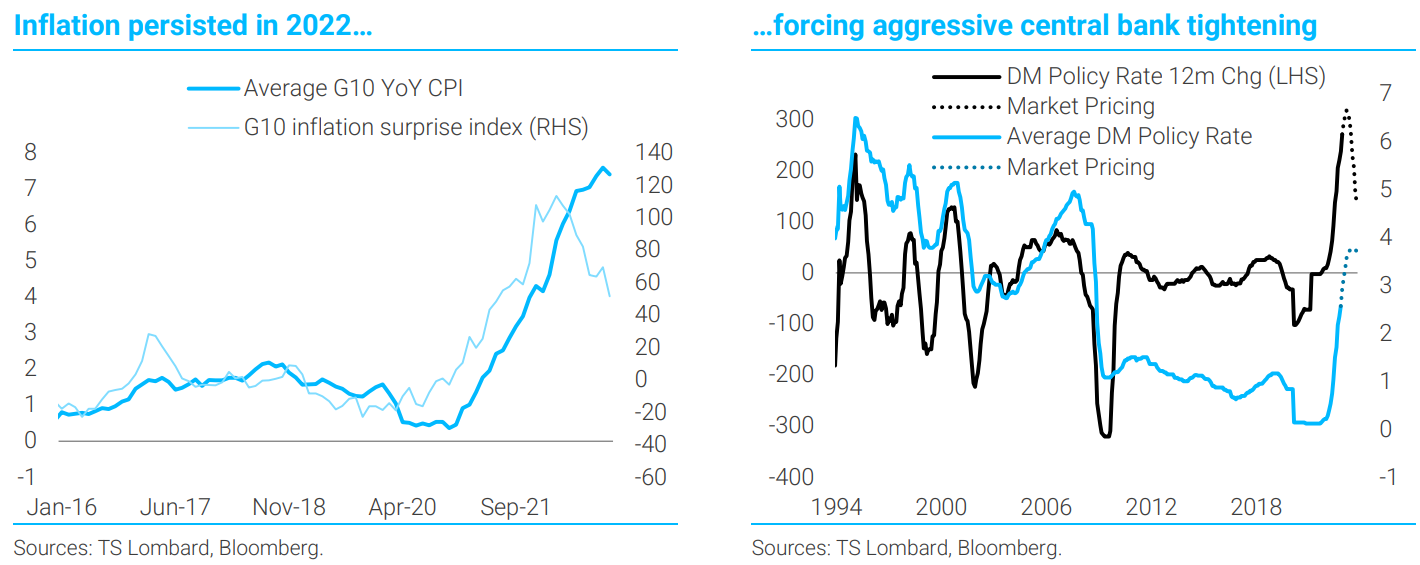

2. Inflation was persistent. Inflation has been hot and heavy throughout 2022, spurred on by both demand (Covid fiscal & pent-up demand, as noted above) and supply-side factors (energy shock – see below). Inflation surprises globally rose into positive territory at the beginning of 2021 and have remained there since, as inflation continued to beat upwardly revised expectations. We can say with some confidence now that inflation has peaked, with risk assets cheering two encouraging CPI prints. But US YoY CPI is still higher than at the beginning of 2022 (7.0% in Dec 2021 vs 7.1% in Nov 2022). Then as now, markets signalled what is likely false confidence that inflation would return to target quickly.