The Reserve Bank of New Zealand (RBNZ) today hiked the official cash rate (OCR) another 0.75% – the largest single increase since the OCR was introduced in 1992.

This lifted the OCR to 4.25%, up from the record low 0.25% in August 2021. It also took the OCR to its highest level since December 2008.

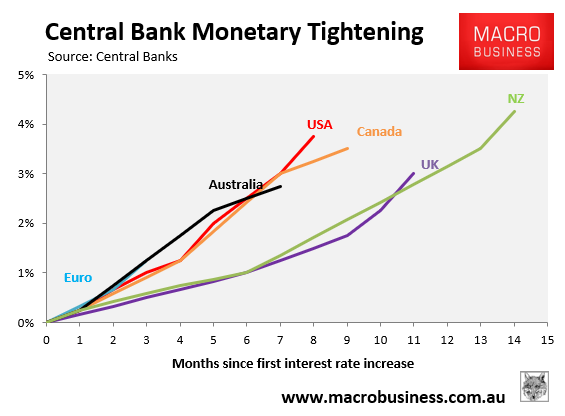

New Zealand now sits atop the global rate tightening table:

In announcing its decision, the RBNZ noted that higher interest rates are needed to tame runaway inflation:

The Committee agreed that the OCR needs to reach a higher level, and sooner than previously indicated, to ensure inflation returns to within its target range over the medium term. Core consumer price inflation is too high, employment is beyond its maximum sustainable level, and near-term inflation expectations have risen…

New Zealand household spending remains resilient, especially considering the rise in debt servicing costs, the fall in house prices, and low levels of consumer confidence. Employment levels are high, and income growth and household savings are supporting spending…

The productive capacity of the economy is being constrained by broad-based labour shortages, and wage pressures are evident. Aggregate demand continues to outstrip New Zealand’s capacity to supply goods and services, with a range of indicators continuing to signify broad-based inflation pressure.

The RBNZ also flagged further monetary tightening:

Committee members agreed that monetary conditions needed to continue to tighten further, so as to be confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range. The Committee remains resolute in achieving the Monetary Policy Remit.

The RBNZ is treading a dangerous path given there are huge numbers of cheap fixed rate mortgages scheduled to expire over the next six months, which will reset to double or triple their current rates.

The decision to continue tightening also means that house prices, which are already down around 12%, will continue to fall.