Below is an edited extract of Westpac’s latest weekly economic commentary, which tips another 1.50% of rate hikes from the Reserve Bank in order to tame stubbornly high inflation.

Westpac warns that more than half of New Zealand’s mortgage borrowers will soon refix to rates that are 3% higher than they are currently paying, which will dramatically slow domestic demand.

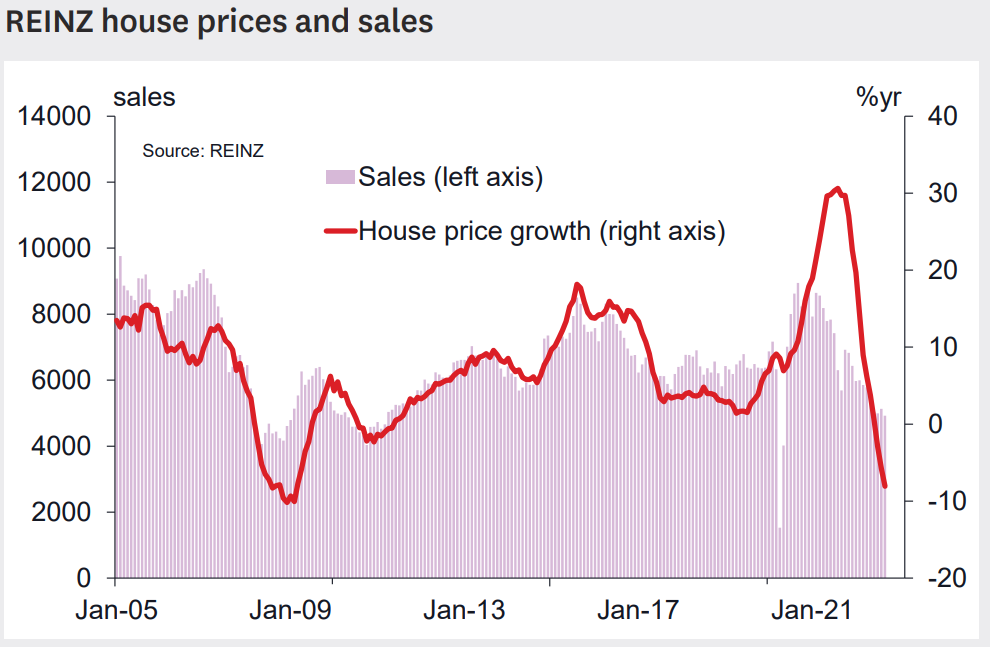

Westpac also notes that “correction in New Zealand’s housing market continues at pace, with prices down by 11% since last November”, and the rising interest rates “point to further price declines to come”.

____________________________________________________________________________________________

Inflation pressures are continuing to run red-hot in every corner of the economy. Consumer prices rose by 7.2% over the past year, and food price inflation hit a 14 year high of 10% in October.

Crucially for the Reserve Bank, expectations for inflation over the coming years have also been pushing higher, as seen in the RBNZ’s own survey of businesspeople and professionals.

Notably, the closely watched gauge of expected inflation in two years’ time has risen sharply, jumping from 3.1% in the September quarter to 3.6% now. That’s the highest this measure has been since 1991 and well above the RBNZ’s medium-term target of 2%.

The elevated level of inflation expectations is a big worry for the RBNZ. Expectations, especially over longer horizons, are a key influence on how businesses adjust prices and wages. Their recent rise signals that the current inflation cycle could be even more protracted.

Compounding the challenges for the RBNZ is that once inflation expectations do rise, it can be difficult to pull them down again. Doing so often requires a protracted fall in inflation, and that can mean a period of weak economic activity.

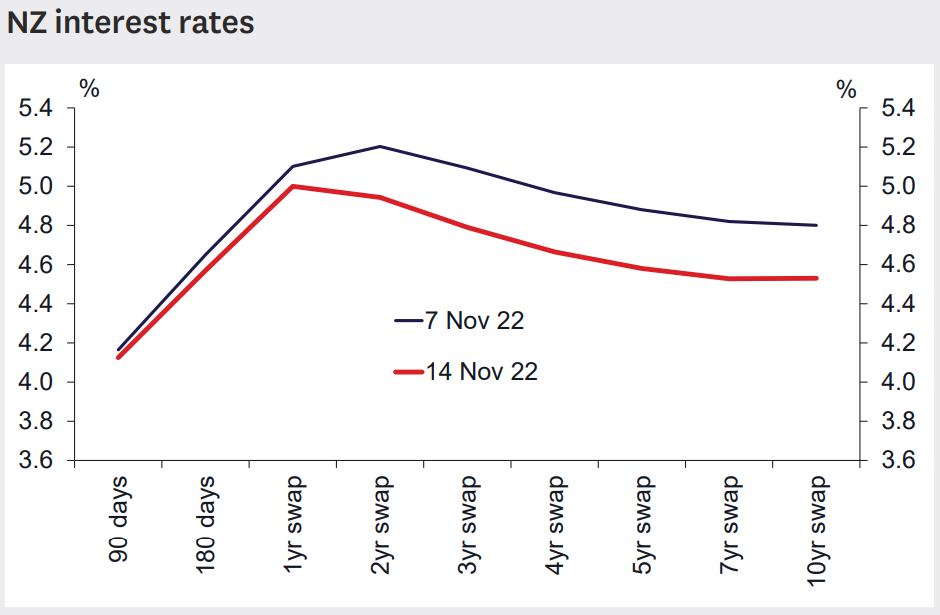

In response to those surging inflation pressures, the RBNZ has been hiking the Official Cash Rate at a rapid pace, with the cash rate rising by 325 bp since October last year. However, a year after the tightening cycle began, inflation is showing few signs of cooling.

At the same time, the drivers of inflation have changed. Initially, the upswing in prices was mainly due to Covid-related supply disruptions and a sharp rise in import costs. However, inflation pressures are now increasingly related to domestic factors, particularly the pressures in the labour market. With businesses across the country struggling to attract and retain workers in the face of firm demand, wage costs have been surging, with average hourly earnings in the private sector up a whopping 8.6% over the past year.

To head off those red-hot domestic inflation pressures, we’re forecasting that the RBNZ will deliver a jumbo-size 75 bp hike at its 23 November policy meeting, and we expect that will be followed by continued rate increases in early 2023.

We expect the Reserve Bank to lift the Official Cash Rate to 5% and to hold it there for the next couple of years, before reducing it to a more sustainable level in the following years.

Indeed, if the RBNZ doesn’t get in front of those pressures soon, the New Zealand economy could realistically find itself mired in a wage-price spiral. That would impose serious harm on households and the economy more generally, with ongoing pressure on living costs and weakness in economic activity.

One of the major complications in the RBNZ’s fight against inflation is the prevalence of mortgage rate fixing. Around 90% of New Zealand mortgages are on fixed rates, and many of those are still locked in at the very low interest rates that were on offer in the early stages of the pandemic. That’s meant large numbers of households are yet to feel the impact of rate hikes to date, which has allowed them to maintain their spending patterns.

That picture will change dramatically over the coming months, with more than half of all mortgages coming up for repricing over the next 12 months. In many cases borrowers will face refixing at rates that are 3 percentage points higher than those they are currently on. And as that occurs, we’re certain to see a slowing in domestic demand.

The correction in New Zealand’s housing market continues at pace, with prices down by 11% since last November. That has only taken them back to where they were in April last year, highlighting the ferocity of the price rise over 2020 and 2021.

Higher interest rates have been the key driver of the correction, and they point to further price declines to come.