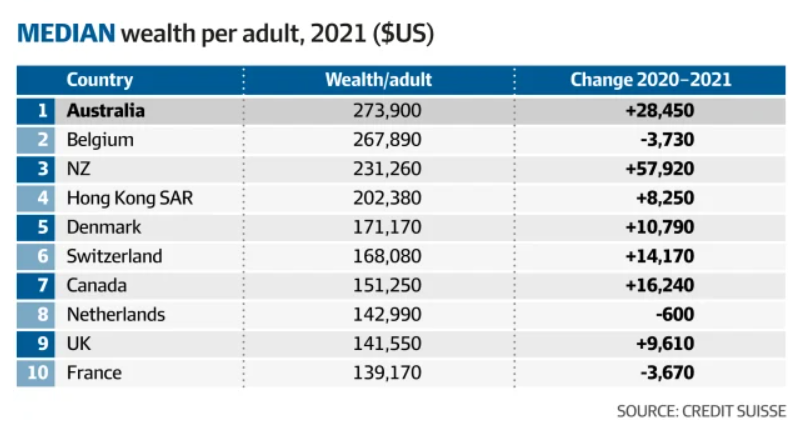

The Credit Suisse Global Wealth Report has once again declared Australian households the world’s richest thanks to their expensive property assets:

The report says that “the overall composition of assets or wealth has not changed a great deal in Australia since 2000” and that Australians display a relatively large preference for housing assets relative to their global peers…

Financial assets such as shares comprised about 39.5 per cent of Australians’ gross assets in 2021, which was below the typical level for a high-income country of 55 per cent.

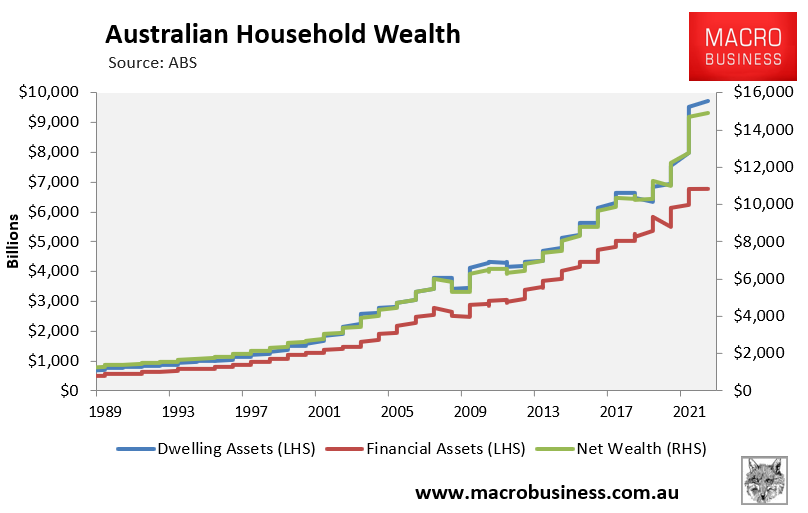

The latest Australian Bureau of Statistics (ABS) Finance and Wealth data showed a record increase in household wealth over the pandemic on the back of the property boom:

Since March quarter 2020, household wealth has increased 35.3 per cent. This was driven by asset prices appreciating, which resulted in wealth per capita increasing by $146,008…

Residential property accounted for most of the growth in household wealth since the start of the pandemic, rising 39.9 per cent.

Advertisement

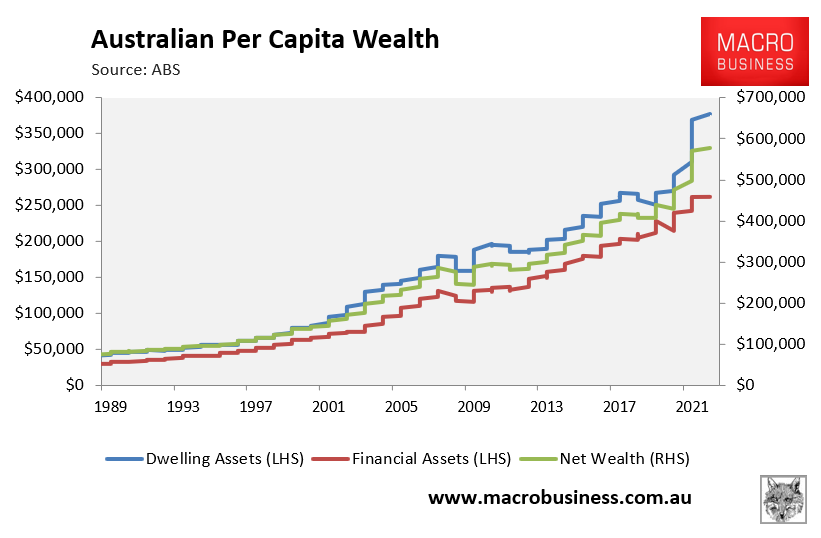

When divided by Australia’s estimated resident population, Australia’s dwelling assets were worth a record $377,000 per head of population in the March quarter, up from the 2019 trough of $251,000:

Property boom fuels Australia’s household wealth.

Is having so much wealth locked up in expensive homes really beneficial to Australian?

Advertisement

Everyone needs somewhere to live and expensive housing serve little purpose to the overwhelming majority of owner-occupiers, who typically must sell and buy into the same market.

Expensive housing also punishes recent entrants or those locked-out of the market. The former is required to take-out mega-mortgages and serve a life of debt slavery, whereas the latter are forced to rent.

Would Australia really be worse-off if the median dwelling price was $370,000 instead of $740,000, aggregate mortgage debt was 70% of disposable incomes instead of 140%, and the banking sector was smaller and less profitable?

Advertisement

The answer is clearly no. Having lower debt loads to service would make Australian households better-off, whereas the broader economy would benefit from the productivity-boosting effects of lower land prices, increased business lending (investment), and a more balanced economy overall.

In any event, Australian home values are now falling quickly in response to the Reserve Bank of Australia’s aggressive interest rate tightening.

Whether it knocks Australia from first place on median household wealth remains to be seen.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.