Until recently, oil was busy wrecking the business cycle. But, in the last few weeks, it has come off fast and is in the process of lifting economic activity. Where do we go from here? My own view is that it will hang on the Fed. Oil is not in sufficient deficit to drive the cycle from this point. If the Fed remains hawkish then it will keep falling as DXY climbs and demand falls. If the Fed pivots too early then the underlying oil deficit will reassert itself quickly. We may even see a sample of that in the near future if the bear market rally lasts much longer. Goldman with more.

—

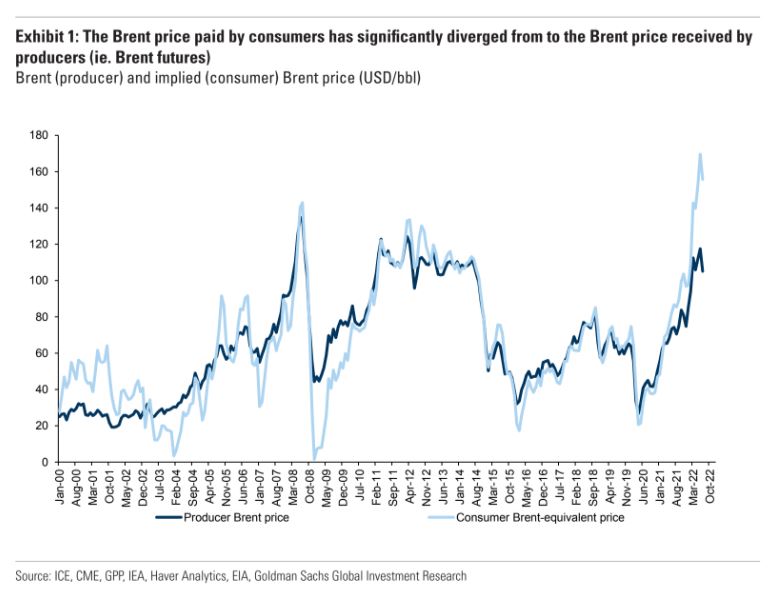

Brent prices have declined 25% since early June, driven by low trading liquidity and a mounting wall of worries: recession, China’s zero-Covid policy and real estate sector, the US SPR release, and Russian production recovering well above expectations. We believe that the case for higher oil prices remains strong, even assuming all these negative shocks play out, with the market remaining in a larger deficit than we expected in recent months.