The global trade shock and reverse bullwhip effect has begun. Pantheon with the details.

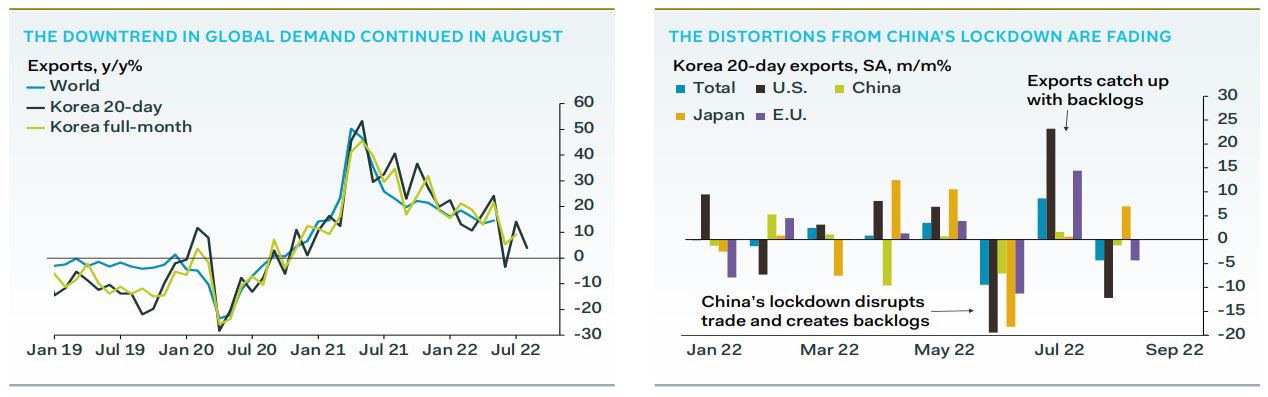

The early signs from Korean exports in August are not good. Export growth slowed sharply in the first twenty days of the month, to 3.9% year-over-year, from 14.5% in July, despite a surge in the ten-day numbers. It is highly likely that global demand for goods continued to slow in August, as implied by our first chart. Further slowdowns, and even an outright fall in global trade values, seem inevitable. In prior months, the Korean trade data were distorted by fluctuations in the number of working days. But working-day adjusted export growth has worsened, slowing to 0.9% year-over-year in August, from 14.2% in July. We can’t blame this underwhelming performance on base effects. Exports fell 4.3% month-to-month, seasonally adjusted, from growth of 8.6% in July. The deterioration in trade looks genuine, and likely reflects a reversion to the trend, which has been in place from the start of 2021.

We argued last month that July’s trad performance did not mark the start of a sustainable bounce in global demand. Instead, it reflected distortions emanating from China, where the economy was reopening following a particularly intense zeroCovid lockdown. The lockdown disrupted regional supply chains in May and June, creating a backlog of orders in the process.