The ferrous complex was smashed on August 4, 2022:

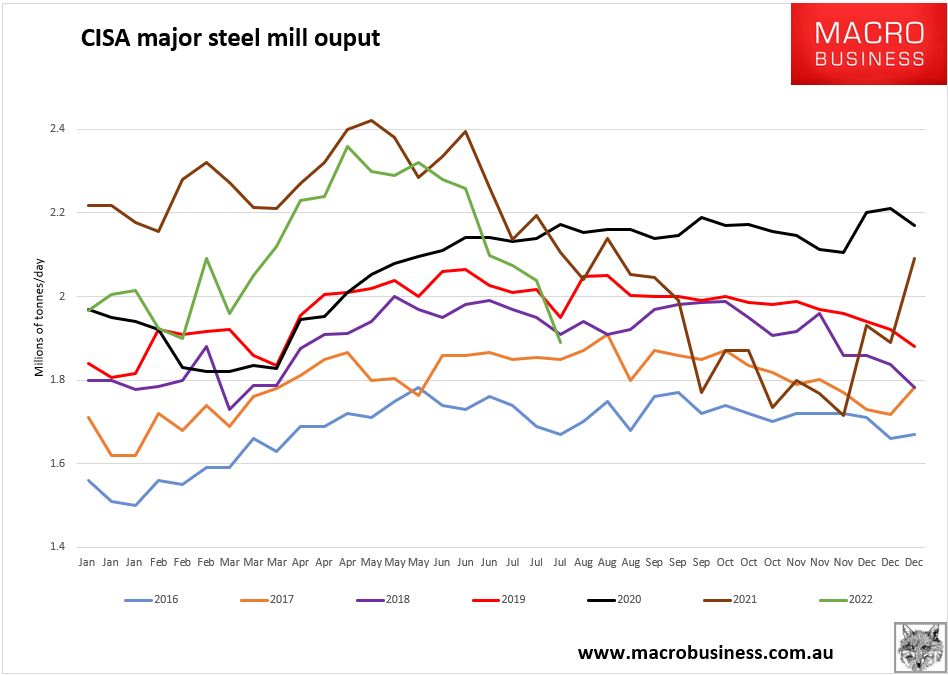

Late July CISA output was out too and as expected we are free falling into the pit. There was some solace in inventories also falling 13%:

GLJ Research points out the obvious:

Advertisement

The ferrous complex was smashed on August 4, 2022:

Late July CISA output was out too and as expected we are free falling into the pit. There was some solace in inventories also falling 13%:

GLJ Research points out the obvious:

The full text of this article is available to MacroBusiness subscribers