Aussie mortgage collapse signals house price doom

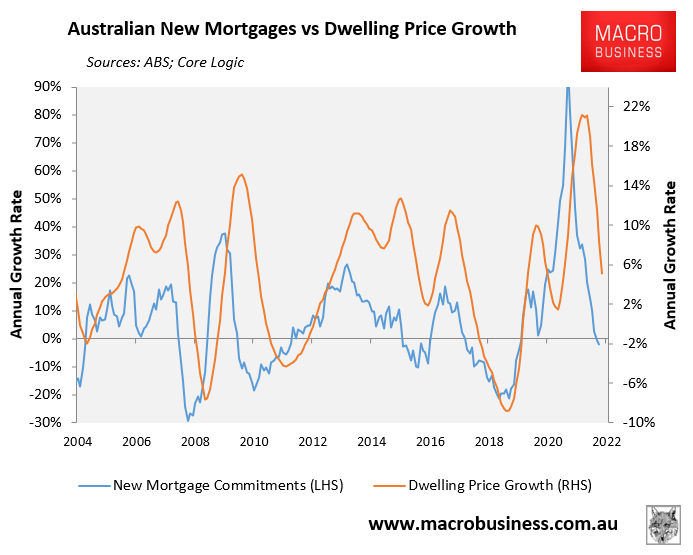

Data released on Tuesday by the Australian Bureau of Statistics (ABS) shows that mortgage commitments fell by 4.4% June, which was the biggest monthly decline since May 2020.

This decline in mortgage commitments captured the first two RBA rate hikes – i.e. 0.25% in May and 0.50% in June – but obviously has not captured the 0.50% rises in July and August.

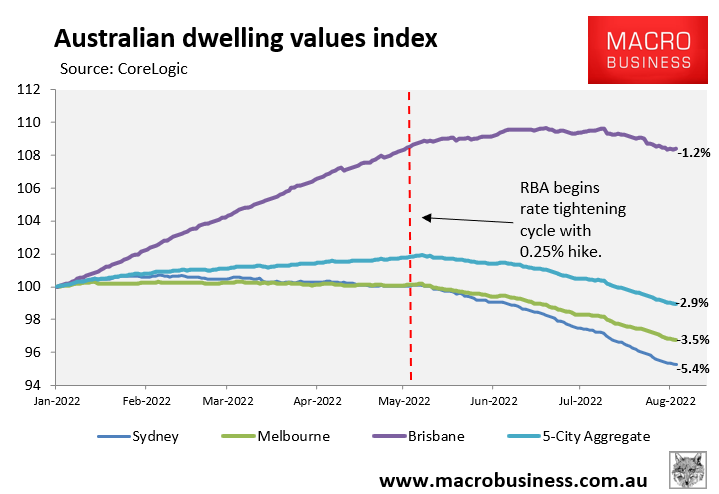

As we know, Australian dwelling values have fallen sharply since the RBA first began hiking rates, with values down 2.9% at the 5-city aggregate level, driven by heavy falls across Sydney (-5.4%) and Melbourne (-3.5%):

Heavy house price falls following rate rises.

Mortgage growth has historically been a strong leading indicator for house price growth. Therefore, the sharp fall in mortgage commitments in the year to June indicates further price falls nationally:

Falling mortgage demand signals house price falls.

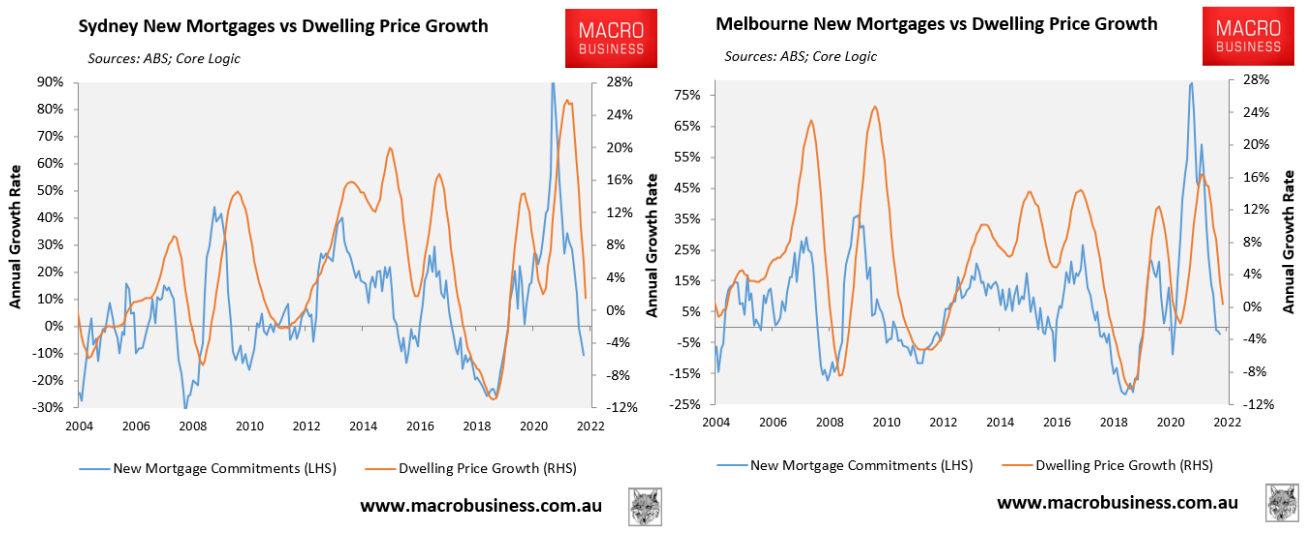

The situation is especially acute for Sydney and Melbourne, which are leading Australia’s house price bust:

Demand collapses across Sydney and Melbourne.

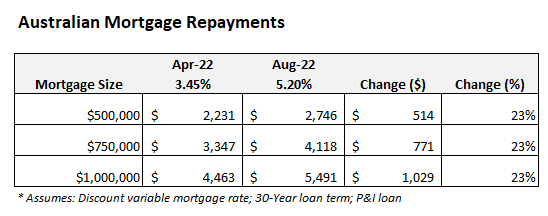

As explained yesterday, the four consecutive interest rate hikes from the RBA has already reduced borrowing capacity by 23%, which is one of the reasons why mortgage demand has shrunk:

Borrowing capacity has already shrunk by 23%.

The other key factor is that “fear of overpaying” or FOOP has taken over from “fear of missing out” [FOMO].

The situation will obviously get worse if the RBA continues to hike interest rates aggressively, as predicted by ANZ, Westpac and the financial markets.

FOOP will intensify, buyers will stay on the sidelines, mortgage commitments will fall, and Aussie house prices will continue to fall.