TS Lombard has written a note arguing that the traditional inverse relationship between unemployment and prices – known as the Phillips Curve – has broken down across the world’s economies because authorities have lost control of inflation expectations.

This, in turn, means the world’s central banks will adopt a paradigm of “whatever it breaks”, in that they will aggressively hike interest rates to bring inflation down, even if it pushes their economies into recession.

Judging by their recent rhetoric, it seems central banks are prepared to burn down everything in order to restore “price stability”…

And they are keen to emphasize their willingness to engineer a “hard landing”, perhaps even a deep recession, if that is the only way to force the CPI back into line with their targets. It is hard to overstate the significant of this shift in monetary “reaction function”. For decades, the authorities pursued a policy of “whatever it takes”, whereby they always did everything in their power to boost economic growth and support asset prices. If we view their claims at face value, we are now in a policy era of “whatever it breaks”, one in which central banks are prepared to tolerate significant economic and financial destruction if that is what is necessary to get inflation down…

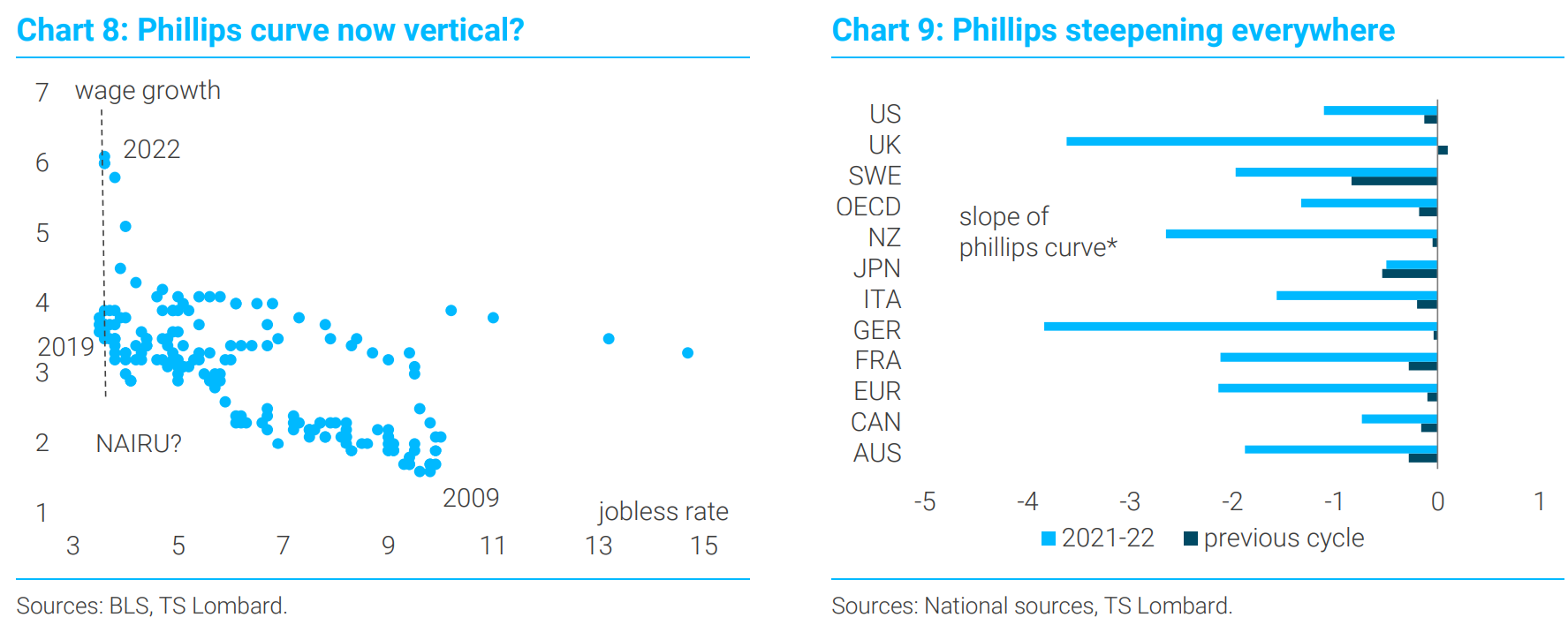

Worryingly, as we have emerged from the COVID-19 crisis, Phillips curves everywhere have steepened (Chart 9). Despite unemployment rates only modestly below their 2019 levels, wages and prices are accelerating everywhere. For officials who have the horrors of the 1970s “Great Inflation” embedded in their psyche, this is eerily similar to what happened half a century ago: the Phillips curve steepened in the late 1960s, which produced persistent stagflation. Central banks are worried about similar dynamics today, either because inflation expectations have become “deanchored” or because the pandemic and the war in Ukraine have combined to damage the supply capacity of the global economy. If the central banks lose control of inflation now, they believe they will need to generate a much deeper recession in the future. The “trade-off” is no longer between growth and inflation now, but between a mild recession today and a nastier one later…

We have always been sceptical about the idea that the world economy is about to relive the experience of the 1970s, a lengthy period of very high inflation and wage-price spirals. While there are obvious superficial similarities with the situation 50 years ago, the structure of the global economy is entirely different. Forty years of neoliberalism has crushed worker power, which means it is hard to envisage a replay of the “power conflict” that was at the heart of the Great Inflation. But, unfortunately, it does not matter what we think. Our reputations are not on the line to the same degree as those of central bankers; and if we get our assessment wrong, nobody will still be discussing our error in 50 years’ time. Naturally, Powell, Lagarde et al. are in a different position. Not only are they directly responsible for inflation; no official wants to become a case study in the topic of “historical monetary failures”. Better to have a recession, which can happen to any central banker, rather than a once-in-a-generation “paradigm shift”, reserved for the few. And recent CPI data, which continue to deteriorate, are making officials only more hawkish…

It is already clear that having plotted their course to neutral, most central banks think they will need to raise interest rates to restrictive levels in 2023. Inflation is sequentially stronger and broader than they expected at the start of the year, and they are worried that persistent labour shortages will eventually spark a wage-price spiral. Financial markets have already absorbed this message, which is why “terminal interest rates” – the highest point in the yield curve – have recently moved above central banks’ neutral estimates…

With policymakers determined to get inflation down, regardless of the short-term impact on financial markets and the economy, the risk of overtightening has increased… Understandably, many investors are already starting to worry about a recession, either now or in 2023. They think central banks will make the same mistake they always make – namely, raising interest rates until “something breaks”…

The authorities’ threat is credible because they clearly believe the short-term costs of such action are significantly lower than the eventual damage they would need to inflict on the economy if they lose control of inflation (not to mention what it would mean for their personal reputations as central bankers).,,

Unfortunately, the odds of a hard landing are increasing…

Today’s workers have much less bargaining power in the modern, globalised and high-tech economy.

In Australia’s case, centralised wage fixing was abolished decades ago. Only around 15% of Australian workers today are in a union, versus the majority of workers in the 1970s. De-unionisation, insecure work, deregulation of the wage-setting process, and the immigration system have all conspired together to shift the balance of power away from workers.

The upshot is that Aussie workers have been left with little bargaining power, thus eliminating the prospect of a wage-price spiral eventuating.

Advertisement

Basically, the working class as a cohesive social force no longer exists in Australia, nor globally. In turn, inflation won’t stick around because workers lack the power to make it do so.

Eventually inflation will subside as supply shocks from the pandemic and war fade and real spending power is eroded.

But rather than acknowledging these facts, central banks will tighten too far and risk plunging the global economy into recession.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.