It’s been caught long into the bust, you see, and needs a bag holder.

JPM started it last week:

“We still hold a base case view that a recession will be avoided and a stimulus-fueled recovery in China’s outsized demand in the coming months could tighten base metals markets and stabilize prices. However, with Chinese demand so far underwhelming, the consensus view of our clients sees base metals prices more fully susceptible to potentially deteriorating economic growth in the US and Europe.”

Goldman joined in a few days later:

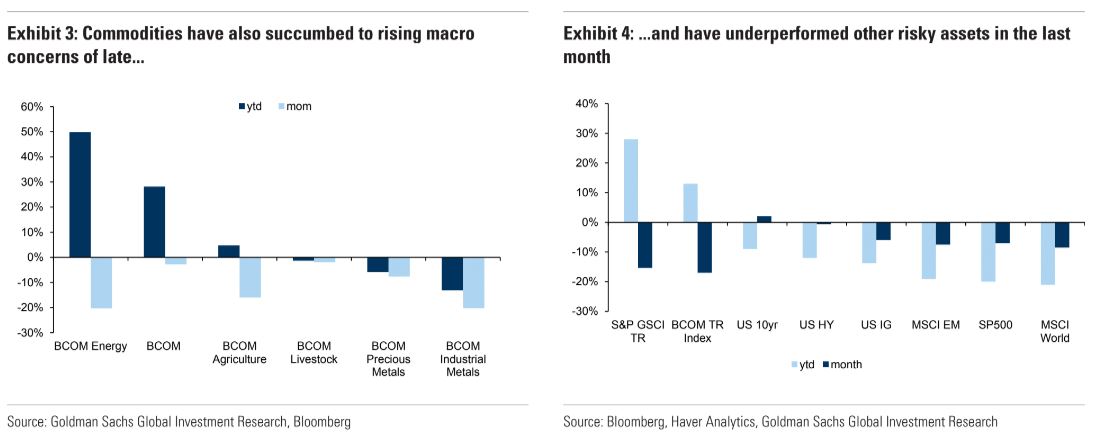

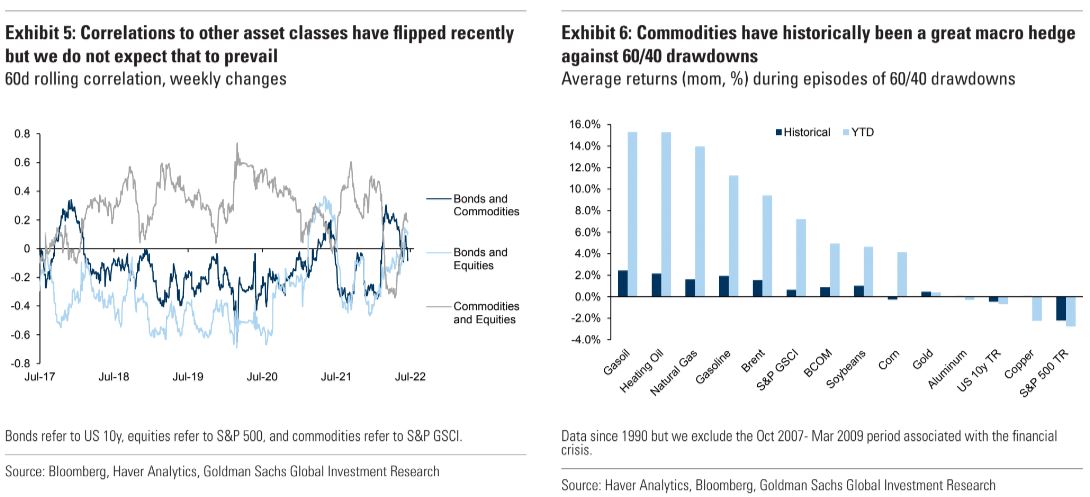

Recession risks now dominate all macro markets. Concerns over the deteriorating economic growth outlook in the US and Europe have dominated all markets lately, with commodities no exception. The BCOM and S&P GSCI total return indices respectively shed -18% and -16.5% relative to their YTD peak hit as the sell-off that initially started in industrial metals not only broadened to other sectors but intensified significantly over recent trading days. As recession fears have gripped risky assets, commodities have become positively correlated to equity and bond markets and negatively correlated to the US Dollar, a stark departure from previous months when commodities delivered outstanding diversification benefits to investors.

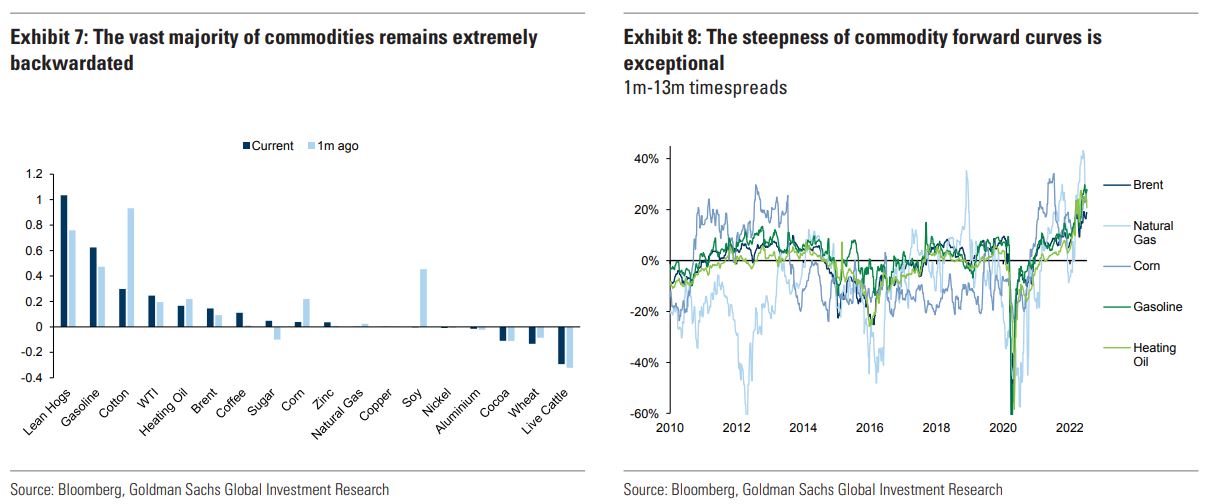

Commodities are disassociated from micro fundamentals. We find this latest commodity sell-off de-linked from physical fundamentals and driven by financial liquidation. Inventories of energy and metals continue to fall from already uncomfortably low levels as demand remains above supply in all cyclical commodities, except iron ore. Time spreads, the single most accurate measure of underlying fundamentals, trade at unprecedented levels of backwardation, irrespective of the price sell-off. Mobility remains robust globally and continues to recover strongly in China and the oil market is pointing to a 1 mn b/d deficit. US and European aluminium premia remain historically high, while physical order books for metals remain strong. Micro scarcity thus paints a fundamentally constructive outlook for commodities despite the rising probability of a US and European recession over the coming 12 months, which commodities stand to weather on China’s large-scale counter-cyclical stimulus.

Commodities remain the best macro hedge. Although we expect spot prices to remain vulnerable to spec length liquidations triggered by negative economic news flow, we believe it is premature for commodities to succumb to recession concerns when the global economy is still growing and markets remain in deficit on strong demand. Thus, we view this price pullback as a longer-term buying opportunity. Barr a large synchronous negative global demand shock that creates a level-shift down in demand, we believe demand rationing will remain the dominant theme for energy and food commodities while an accelerated stimulus program in China should help to create a turnaround in base metals pricing in Q3. Thus, we believe the correlation between commodities and other risky assets is set to decline again given that commodities are spot assets while risky assets discount future expectations that have turned more negative. It is important to remember that, with the exception of the GFC, commodities have been a great macro hedge, with all sectors delivering positive returns during large drawdowns in 60/40 portfolios since 1990.

Volatility trap is gaining momentum. That said, while many commodity markets remain remarkably backwardated so is volatility, making them harder to invest in. Trading frictions have pushed up near-dated volatility and raised initial margins to extreme levels, thus pushing more market participants off-exchange, which has cemented a negative spiral between low liquidity and high volatility. Price adjusted AUMs in commodity indices are down 24% YTD, as a result. Net, while current price levels do not seem to reflect current micro conditions nor the full impact of Russian sanctions, long-term investors in commodities will likely have to continue to stomach higher volatility in return for a significant total return pay-off.

Goldman is especially bullish oil:

Advertisement

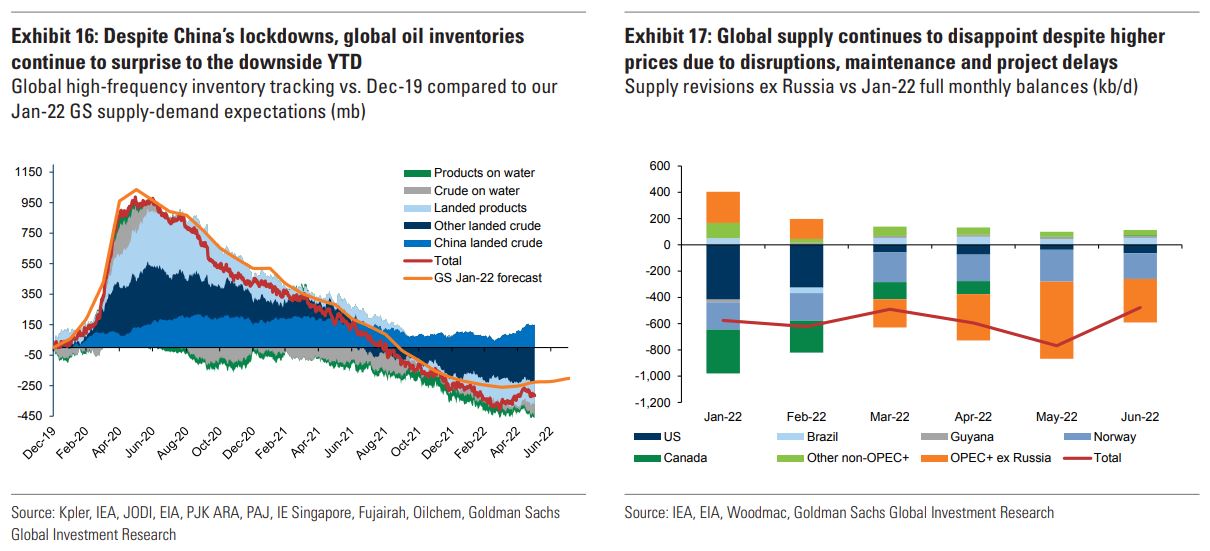

We view the recent sharp sell-off in crude oil prices as driven by growing recession fears in the face of low trading liquidity, with technicals exacerbating the sell-off. The declines in prices and refining margins since mid-June are now equivalent to the oil market pricing in a 1.1% downward revision to 2H22-2023 global GDP growth expectations. We believe this move has overshot – while risks of a future recession are growing, key to our bullish view is that the current oil deficit remains unresolved, with demand destruction through high prices the only solver left as still declining inventories approach critically low levels.

So, let’s unpack this:

In its various bubble-blowing commodity notes over the last year, which can now go down as ringing the bell at the top of this mania, Goldman constantly sidelined plunging Chinese demand as relevant to commodity prices. Yet now that falling Chinese demand is playing a role, new stimulus is suddenly going to drive commodity prices higher! Cognitive dissonance anyone?

Chinese stimulus is still fighting an unprecedented property crash. That is, the stimulus is slowing the decline of commodity demand, not lifting it.

The looming trade shock will make this worse.

China is about to resume exporting commodity deflation as its huge energy advantage comes to bear on processed metals.

Whether the US and Europe are headed for mild recessions is highly speculative. My own view is that they will be materially worse than that. Once the Fed slows the US consumer enough, the odds favour a large US inventory destocking cycle that will reverse bullwhip China and Europe.

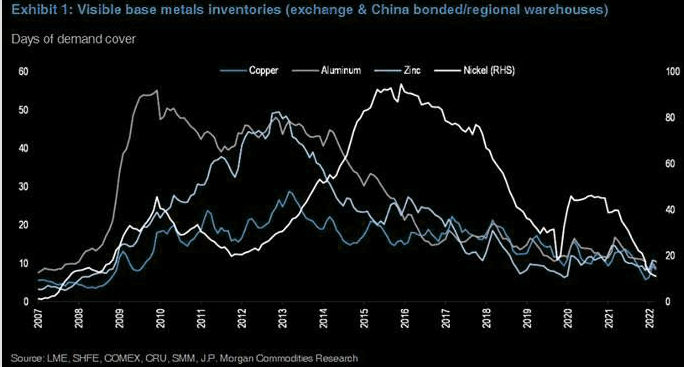

As noted many times, it is always wise to be suspicious of commodity inventories in warehouses. They are often held by speculators, like JPM and GS, and do not provide a reliable take on underlying availability. Moreover, the moment you get a recession of any size, inventories explode.

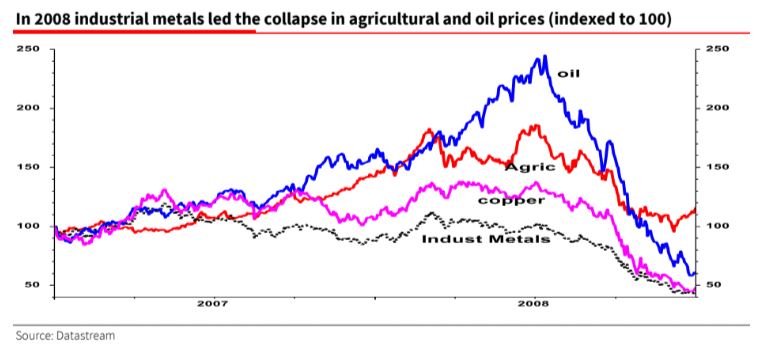

Indeed, low inventories is a strong contrarian sell signal for commodities, especially when they are so central to creating the very inflation they are supposed to hedge. See 2008:

There is one more argument being made for commodities now. Ironically, by alleged contrarians like the Bear Traps Report:

Advertisement

In times of real stress – risk data, old fashion financial conditions – move at 10x the speed of their economic counterparts. It’s a dynamic we experience maybe once or twice in twenty years. An entire theater full of economists and strategists all oblivious to the changing of the guard around them – all still living in a lost world.

The great awakening is near. In the US, central bankers have brought forward recession risk, by so aggressively pulling back accommodation – as promised with an economy already in contraction They now face creeping deflation risk – something these academics have been fighting for decades – this darkness surging at the fastest pace since Q 1 2020. They over cooked the Porterhouse, hold the Béarnaise, please Much like last year – we suspect the large drawdowns in commodity sector equities are a buy . There is no question – economic risk is higher – but the Fed cannot embark on a long protracted hiking cycle with a mountain of data pointing towards a sharp recession.

The “D” word is even in play. The ONLY way to get inflation back to the 2 neighborhood is depression, this is a price the Fed just isn’t willing to pay.

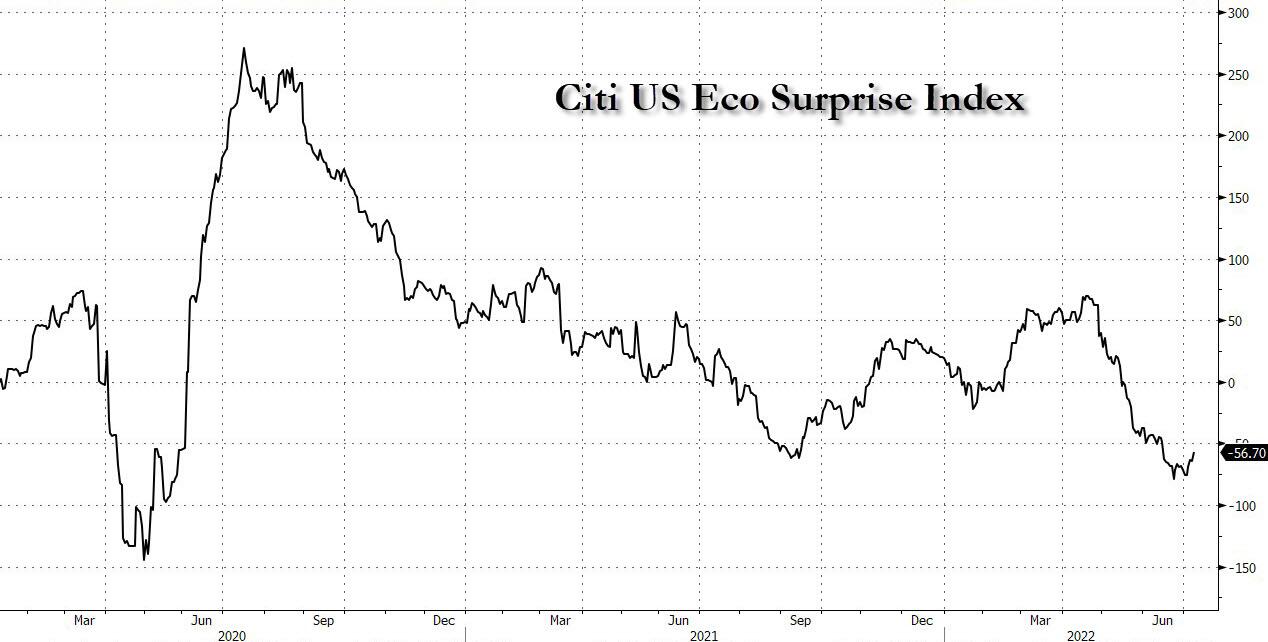

In this note, we look at ISM, Richmond Fed, Dallas Fed data, Atlanta Fed data, and a U S labor market rolling over faster than Cape Cod’s Humpback whale – always one of the summer’s finest attractions in the North Atlantic. With conviction – we believe the US is in recession now. The CESI (Citi Economic Surprise Index) and consumer confidence data are just wow.

Ultimately if we look around the planet as to where recession is MOST priced in – all eyes are on Europe, NOT the US. This means the Fed has only one viable option – play a cat and mouse game with markets.

Think of back-and-forth monetary policy – there will be no straight line we witnessed from 2016 to 2018 and from 2004 to 2007. The strong dollar is destroying our planet’s economy, once again – the Fed is under immense pressure to arrest the global wrecking ball. Above all, with China’s lockdowns ending – fiscal and monetary support is picking up in Asia – we view beaten down global cyclicals in the commodity space as a buy.

Cyclicals are “over the valley” trades, which means you buy them when you are at the early stage of recession as you are walking down into the valley, as opposed to being at the bottom of the valley looking up. Which no one can time.

Clearly, a smart entry point is key as there are still colossal headwinds coming from Europe and a slowing U.S. Bottom line – as the wounded US economy plays catch up with the Rest of the World – the US Dollar implodes over the next 12 months.

The hot money exit found today in commodity names is a buying opportunity – lots of weak hands, the late comers chasing commodity plays just got flushed. In our view, the early flush is most tradable.

Our Take

Clearly, we are in a recession. As we stressed last week, with Biden and the Press Secretary, pounding the table “no recession.” On the Hill for his June testimony, Powell was forced to defend his President Good cop, he needs a bad cop, the data is the bad cop. Bad data gives Powell cover to toss the White House under the bus.

High Conviction – A colossal secular change is upon us: inflation will normalize at a much higher plain than in the previous regimes. Inflation is taking growth out at the knees. The Fed is stuck in a stale narrative – they are hiking aggressively in a recession bringing forward deep recession risk, and deflation risk. “We are looking at the largest Fed policy mistake since the 1930’s” – Federated CIO this week, a former bull

Recession and Inflation

At best the U S economy is going nowhere and at worst we are in a full blown recession. If inflation goes down, it won’t go back to 2 by the time the Fed lowers rates. And that will set off another wave of inflationary expansion that will force inflation to rebound to even higher levels than exist today after the recession induced moderation in inflation has concluded. We need to think several moves ahead, not just one move ahead. Meanwhile Powell is looking one move into the past!

This is hyperbole. Even a mild recession in the US will trigger an unwind of the great US inventory pile and a spillover trade shock into weak domestic demand in Europe and China. This is not depression. It is regulation global recessionary dynamics that happen every cycle:

Advertisement

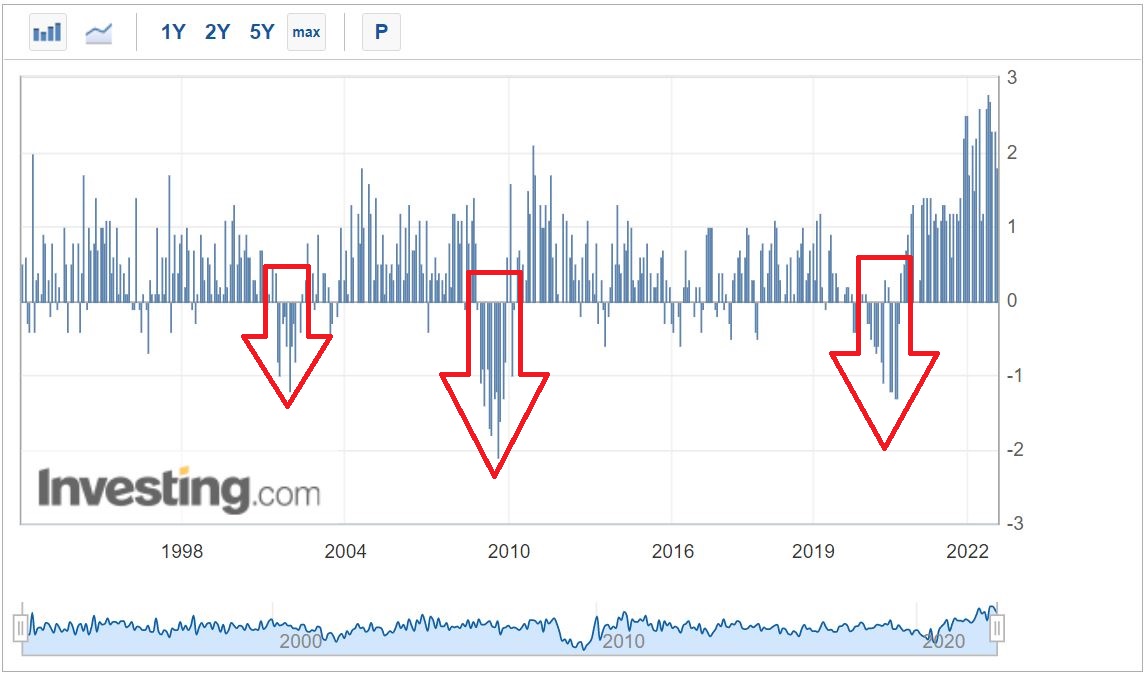

Check out the enormous growth in inventories over the past year. This is over-ordering as part of unsustainable goods demand born of stimulus and supply chain inflation panics.

As they resolve and inflation plunges, the Himalayan pile of goods is going to liquidate and form a feedback loop of doom with commodities.

Don’t take my word for it. Albert Edwards of Societe General has been here many times before:

Advertisement

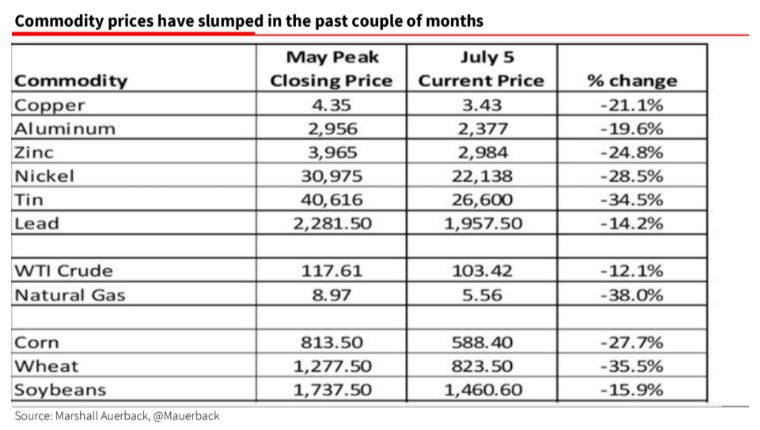

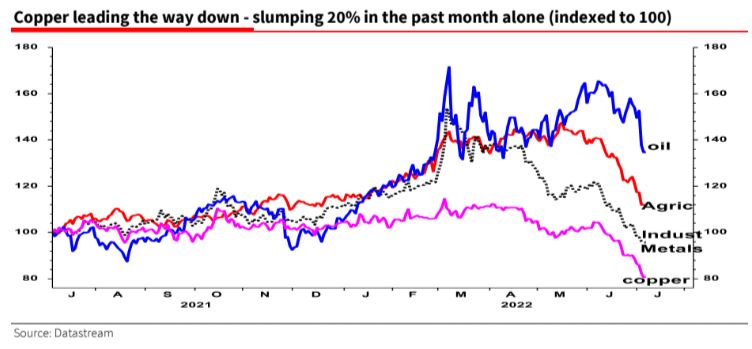

Two weeks ago we wrote that the slide in commodity prices was starting to look eerily like 2008, but the past two weeks has seen a stunning collapse. And it’s not just within the industrial metals complex, with copper down some 25% in just a month, but also most surprisingly, agricultural prices. This is not so much a canary in the coalmine as a rout. Just as in mid-2008 I now see the recessionary gorilla charging towards us out of the mist.

The commodity complex is now seeing a collapse in prices, and this shows great similarity to what we saw in mid-2008. Although the oil price decline is slower and lagging, likely because of the Ukraine war, other industrial commodity prices are in virtual freefall. Soft-landing

advocates must now face the overwhelming evidence of economic collapse and extricate their heads from the sand.

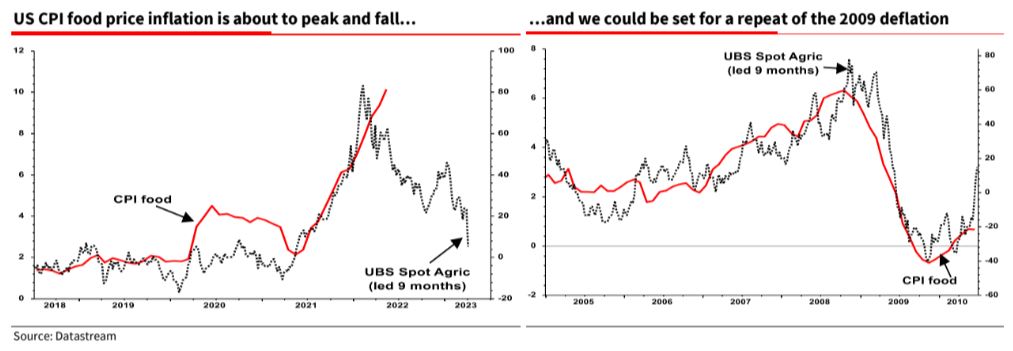

Despite the fallout from the Ukraine war, agricultural prices too have also imploded, and that will sound a note of caution for those who think the oil price cannot fall as quickly as other industrial commodity prices. With the oil price having slid from $125/b to under $100 in a month, it should not be long before the yoy comparisons are negative, as with food prices.

Headline CPI inflation will likely turnnegative, and the inflation narrative will then evaporate (temporarily), so trigging a collapse in US 10y yields back below 1%. What a shock that will be!

The collapse in industrial metals prices over the past few weeks has been spectacular. Most attention has focused on the copper price as it is seen to be a bellwether for the health of the global economy, but the collapse has spread rapidly throughout the industrial metals complex.

There are times in economics (and here in the UK, in politics) when it is obvious the game is up and it’s time to get your head out of the sand.

All these data are consistent with the global economy plunging into a deep recession. Soft-landers (now as rare as flat-earthers) claim that this is just excess speculative froth being blown off, but the bulls said that too in 2008 and look how that ended up!

For those who believe this collapse is due to hedge fund speculative positions being closed, I invite you to check out Ed Yardeni’s regular updates on the CRB Raw Industrials Spot Index, which minimizes the influence of hedge fund speculative activity on that index. It too has slumped. I actually also heard someone say the level of the copper price was still too high for there to be a global recession. What nonsense! It is the rate of change that matters, not the level. One thing that surprised me though is that agricultural prices are falling as fast as industrial metals. Is that due to long speculative positions unwinding? Or is it like a decade ago when QE2 ‘triggered’ the Arab Spring, where agricultural prices were not just driven by fundamentals, but by QE. Are falling commodity prices now driven by QT – just like the repo market blew up in 2019?

The long and the short of it is that US CPI food price inflation is set to collapse into yoy deflation, just as it did in 2008/9 (see chart above). The same thing should happen with oil if there is a global recession despite the war in Ukraine. Oil prices this time last year were between $75-80/b, so it won’t take much of a fall from here to get into a yoy deflationary environment. And that will be the big surprise in the next six months. As commodity prices slump – reflecting the unfolding global recession – headline CPIs will collapse around the world, and with them the inflation narrative (although the reprieve might prove temporary).

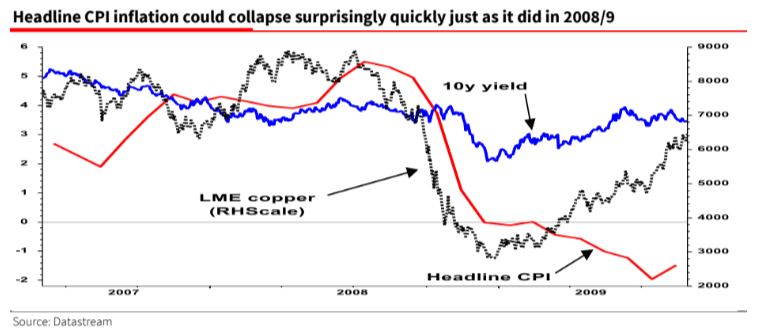

But just to quickly remind ourselves of the power of ‘Dr Copper’ to accurately spot an ailing economy well ahead of economists, let’s look at what happened in 2008 in the chart below where headline CPI fell from 5½% to below zero in just a few short months. The secular story might have transitioned away from the Ice Age to the Great Melt (where the cycle will bring higher highs and higher lows in interest rates, bond yields and inflation), but first a cyclical bust awaits and that will feel very much like a full-blown return to deflation.

For me, the jury is still out about commodities and whether inflation has structurally bottomed. I have my doubts. Despite the arguments about ESG, deglobalisation etc, commods are super-fungible, easily dug up, and, biggest of all, China is slowing structurally and fast.

What is in no doubt is that the Wall Street commodities bubble of the past year is bursting and the base case remains that it has further to go as a global recession takes hold.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.