TSLombard with a note. This goes to whether today’s inflation breakout is structural or cyclical. I am still in the latter camp so think of this more as a few years of interlude as global energy rearranges itself without Russia than it is the end of the Great Moderation. Aussie households had better hope I’m right because the local housing bubble is about a pure figment of the GM that I can pinpoint.

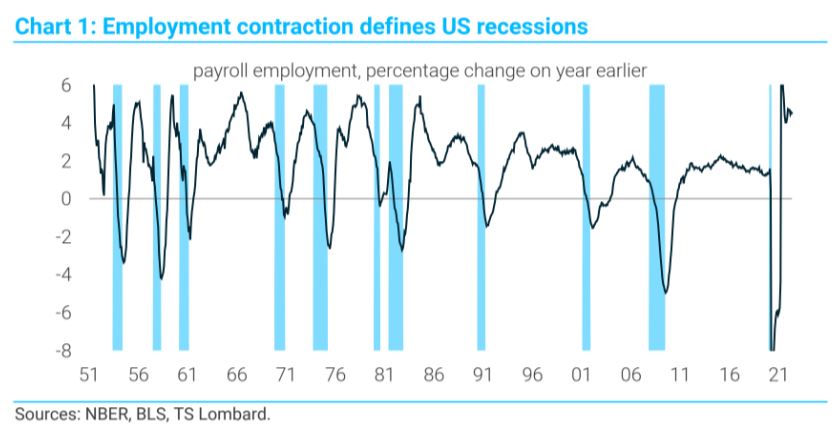

Everyone is talking about a global recession, an issue that will become even more heated this week if the US prints a second consecutive decline in real GDP. But as I explained in my latest Macro Picture, whether economies record a “technical” recession is largely irrelevant at this point. It makes more sense to focus on what is happening in labour markets. There are two reasons why the jobs market, though lagging now, are crucial for the broader outlook. First, a decline in employment usually brings dangerous “reflexivity”, leading to more spending cuts and additional rounds of jobs losses. That is why once employment cracks, there is always massive uncertainty about the ultimate depth and duration of any downturn. Second,

central banks are extremely worried about inflation. But an economic downturn that does not involve significant job losses is unlikely to generate sustained disinflation. And given current labour shortages, we are a long way from the sort of downturn that will cause serious reflexivity or allow a genuine “monetary pivot”.

More generally, the “recession” we are discussing today looks very different from those of the past 30 years. Investors are obsessed with the R-word precisely because they have been accustomed to long US economic expansions punctuated by a sudden plunge in asset prices, which usually happened alongside sharp declines in employment and output. Excluding the artificial COVID-19 downturn, every US recessionhas had a distinctive “end of cycle” vibe, which was always linked to developments in financial markets.Investors needed to anticipate cyclical turning points in order to avoid catastrophic losses. This was theera policymakers dubbed, without irony, the Great Moderation. Most of the time everything seemed good.