As we keep saying, commodity supply-side adjustments are wildly dynamic and take manifold forms. The current energy shock will work itself through in a few years.

In the shorter term, I am of the view that oil will need to fall a lot more than the low-$100s to placate the Fed and recession will do it.

JPM with the note.

—

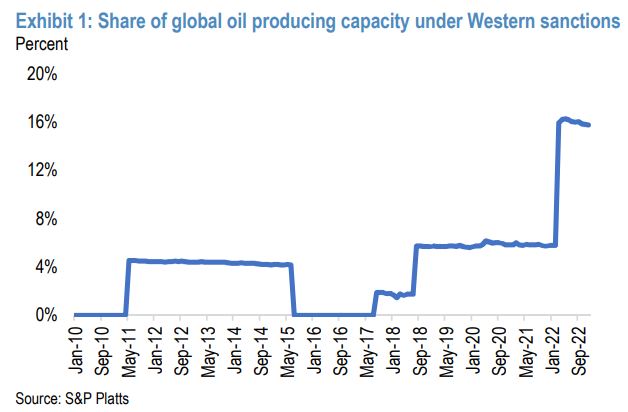

With 16% of global oil capacity under sanctions, there is no cheap way to keep Russian barrels out of the market

Group of Seven leaders agreed to develop solutions aimed at reducing Russia’s hydrocarbon revenues while minimizing the negative impacts of high energy prices. In a mandate announced as the three-day G7 summit ended Tuesday, the G7 leaders instructed ministers to evaluate the “feasibility” of implementing temporary price caps on imports of Russian energy. The G7 agreement considers a wide range of approaches, including options for a “possible comprehensive prohibition” on the transportation of Russian seaborne oil to non-European countries, unless it is priced at or below a predetermined price. The cap could be enforced via limits on availability of European insurance for Russian oil cargoes as well as shipping services and US finance.

The background:

The EU and UK agreed in May to prohibit insurance on tankers carrying Russian oil, as part of the EU’s sixth package of sanctions on Russia. The EU has now put its ban into law, which was enacted on June 3.

The UK agreed to mirror Brussels’ insurance ban—thus ensuring that the Lloyd’s of London insurance market is held to equal standards—but has not laid out its own measures yet.

The EU has proposed a six-month phase-in period for the ban.

The European insurance industry (the so-called “The 13 P&I Clubs”) provides marine liability cover (protection and indemnity) for about 90% of the world’s ocean-going tonnage and covers virtually every type of vessel. The Group relies on Lloyd’s for reinsurance cover.

One key area of marine insurance is liability cover, which covers ship owners for accidents such as oil fuel spills that can incur multi-billion dollar claims. Without such cover from an internationally recognized insurer, many ports would decline entry to a vessel.

Passage through the Suez Canal requires two types of insurance: internationally accepted P&I (protection and indemnity) and H&M (hull and machinery) insurance, which is now provided by The 13 P&I Clubs.

Market impact:

At the onset of the Russian-Ukraine war, many oil market analysts and traders assumed that the impact of sanctions would increase over time. We assumed the opposite: that interruptions to Russian oil supplies would be most acute immediately following the invasion due to self-sanctioning. Given that almost 1/5 of global oil producing capacity today is under some form of sanctions (Iran, Venezuela, Russia), we believed there is no practical way to keep these barrels out of a market that was already exceptionally tight (Exhibit 1). Essentially, our view was that, given time, Russia would be able to reroute its deeply-discounted oil to willing buyers who aim to curb domestic inflationary pressures.

Behind our view was the estimate that Russia would be able to source shipping capacity to transport about 3.2 mbd of its crude oil—enough to offset all its pre-war crude exports to the EU, US and UK and most of its exports of products (Oil Weekly: We placed a price on oil freedom. It’s $400 billion, 24 May 2022). Tanker volumes could potentially increase 11x were Russia to be successful to expand both its oil exporting ports and its East SiberiaPacific Ocean pipeline (ESPO) in Russia’s Far East.

We also believed that countries would begin to provide sovereign insurance to allow the flow of deeply discounted Russian oil. For example, the state-run Shipping Corporation of India has in the past carried Iranian oil for state-run Indian refiners when the West first sanctioned Iran in 2012. In case the insurance-related sanctions hit the shipping industry carrying Russian oil, the Indian government has previously approved coverage from staterun insurers setting a precedent that it could do so again in the future, should the need arise. Similarly, China’s COSCO vessels have in the past transported Iranian oil in 2013 with Iran commenting that insurance was handled by the “Chinese side.” Similarly, Japan had also guaranteed up to $1 billion of insurance claims for Iranian shipments made in 2012.

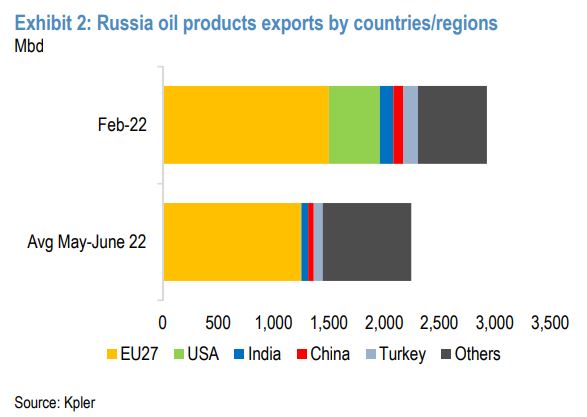

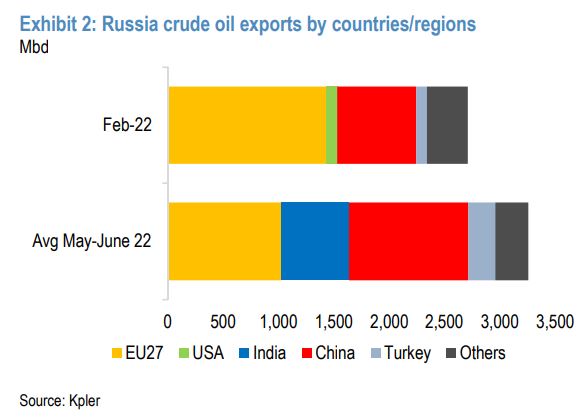

The view has largely played out. While Russia initially struggled to find a replacement for Western consumers of its oil products and has had to shut in refining capacity, Russian crude oil has not only found new buyers, waterborne flows of Russian crude are actually higher than they were before the Ukraine crisis (Exhibits 2 & 3). Not only are Russian crude oil deliveries resilient, but we are beginning to see signs that shipments of bottom-ofbarrel oil products like fuel oil are beginning to recover as well. Just last week, Russian dirty products flows climbed to 1.4 mbd, a pace of shipments we’ve only seen once since the beginning of the Ukraine War. While Russia dirty products shipments are still well below 2021 levels, any increase would likely allow Russian refiners to ramp up runs. Accordingly, Russian production of oil and condensates has stabilized at pre-war January levels, after declining 1 mbd in April.

In terms of insurance coverage, the state-controlled Russian National Reinsurance Company (RNRC) is now acting as the main reinsurer of Russian ships, including Sovcomflot’s fleet. In mid-June, Sovcomflot disclosed that it has insured all its cargo ships with Russian insurers and the cover meets international rules, likely enough to keep Russian vessels sailing around the world. To guarantee RNRC has adequate resources to provide reinsurance, Russia’s central bank in March raised RNRC’s capitalization to 300 bn rubles ($5 bn) and hiked its guaranteed capital to 750 billion rubles.

From its side, India is providing safety certification for ships operated by Sovcomflot, enabling oil exports to India and elsewhere. Certification by the Indian Register of Shipping (IRClass)—one of the world’s top classification companies—is the final link after the insurance coverage for gaining access to ports. Chinese insurers are also apparently looking to take on business that was previously covered by their Western counterparts, but they would likely require a sovereign guarantee.

Pricing impact:

Our view hasn’t changed. Markets need time to adjust. As the EU gradually transitions away from Russian energy sources, Russia will adjust oil flows toward other buyers and global ex-OEPC+ supply growth would have time to grow sufficiently to fill at least some of the Russia-sized hole in global oil supply. Demand will also begin to react to record-high oil product prices; the first cracks in the US gasoline demand are already visible. These conditions should be sufficient to stabilize global oil price in low $100s.

Punishing other countries that continue to do business with Russia will likely cause further chaos in oil markets, unhinging oil prices. The first time the EU announced an insurance ban, it moved the Brent crude price from $100/bbl at the beginning of May to $120/bbl. This week it contributed to a nearly $10 move from a low of $110/bbl last Thursday to $118/bbl today. By some estimates, about 40% of current Russian shipments, or about 1.3 mbd, could be lost, should oil eventually fall under Western secondary sanctions and a full insurance ban. Given the strained liquidity, for oil this represents a $140-150/bbl upside. This estimate does not include the loss of Kazakh volumes, which are hard to distinguish from the Russian-origin oil as it is shipped from the same port of Novorossiysk in the Black Sea. Ironically, the simplest way to bring oil prices—and Russian oil revenues—down is to produce more. The US has more than sufficient capacity to increase production itself.