According to JP Morgan, there are signs that rampant global food inflation – which has been running at multi-decade highs – is starting to ease, led by agriculture prices. JP Morgan’s model is pointing to “a big move down in consumer food inflation over the next six months”, which “would lower food’s

contribution to headline CPI”.

________________________________________________________________________________________________

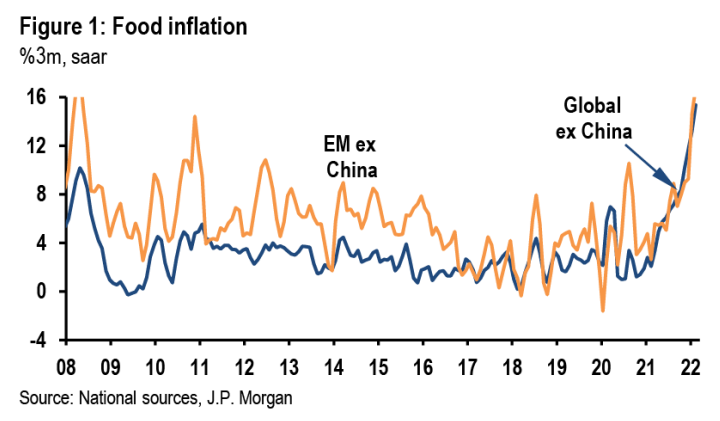

Food prices have been an important driver of this year’s CPI inflation surge. Global food inflation picked up to a 15%ar in the three months to May—a multi-decade high—and its breadth across countries and regions is remarkable. EM ex. China’s food CPI is up 18%ar, DM is up 14%ar, and even China rose 18%ar in the three months to May (Figure 1).

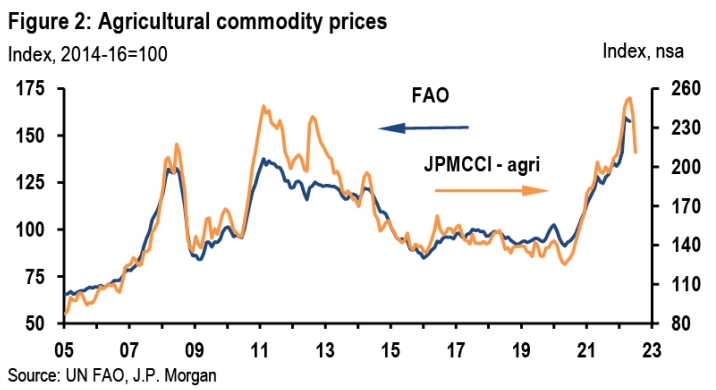

While consumer food inflation remains strong, run rates on agriculture prices have been coming off sharply. After surging 20% in the first four months of the year, the J.P. Morgan agri commodity index fell 5% in June and is tracking a 10% drop in July as wheat prices correct lower. The FAO food index—a more direct measure of global food prices—is likely to follow a similar, albeit less volatile, pattern (Figure 2).

Assuming agri prices stabilize, food inflation is set to come off the boil. Momentum in food CPI already looks to be waning in a number of EM countries since May, even as over-year-ago rates continue to increase. Given the larger share of food in EM consumption baskets the resulting moderation in headline inflation could be sizable, especially in EMEA, which is most sensitive to wheat prices. A moderation in inflation could also remove pressure on central banks although upside risks remain for economies more prone to FX volatility.

Base case: food inflation has peaked

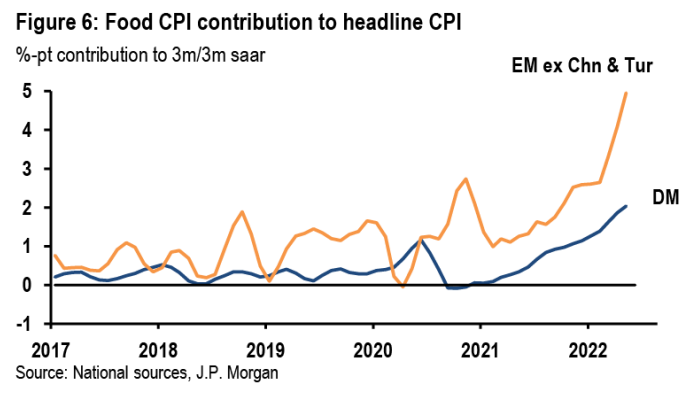

Our model for the global food CPI, which incorporates commodity prices, the economic cycle, and exchange rates across 26 countries points to a big move down in consumer food inflation over the next six months. Assuming agriculture prices stabilize at current levels, global food inflation would halve from 13%ar in 2Q to 5.5%-6%ar in 4Q. This would lower food’s contribution to headline CPI from 3%-pts to 1.5%-pts. In EM, a similar-sized decline in food inflation would drag headline inflation down by an even larger 2%-pts…

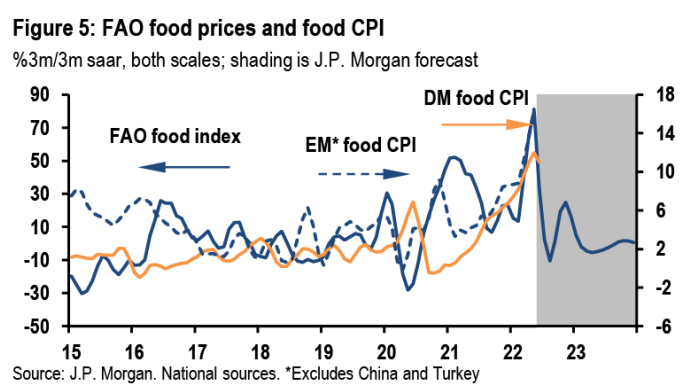

Our commodity analysts are forecasting a renewed leg up in several key agricultural commodity prices over the summer. Namely, they look for supply shortages to boost wheat and corn prices 10%-15% in 3Q22 from their June levels and see prices elevated well into 2023. Even with this rise, our translation of their forecasts for wheat, corn, sugar, vegetable oil, and meat prices into the FAO points to a sharp downward trajectory in 2H (Figure 5). The relationship between the FAO food index and EM food CPI has been remarkably strong since 2017 (correlation 0.66) with the bulk of passthrough occurring within one to two months. In DM the passthrough takes longer with the peak impact coming after six months.