Oil prices crashed overnight, with Brent down more than 10% from the morning highs on mounting global recession fears. However, Goldman Sachs believes oil’s fundamentals remain sound.

___________________________________________________________________________

Oil prices collapsed today, with Brent down more than 10% from the morning highs. We view this move as driven by growing recession fears in the face of low trading liquidity, with technicals exacerbating the sell-off. The declines in prices and refining margins since mid-June are now equivalent to the oil market pricing in an 1.1% downward revision to 2H22-2023 global GDP growth expectations. We believe this move has overshot – while risks of a future recession are growing, key to our bullish view is that the current oil deficit remains unresolved, with demand destruction through high prices the only solver left as still declining inventories approach critically low levels.

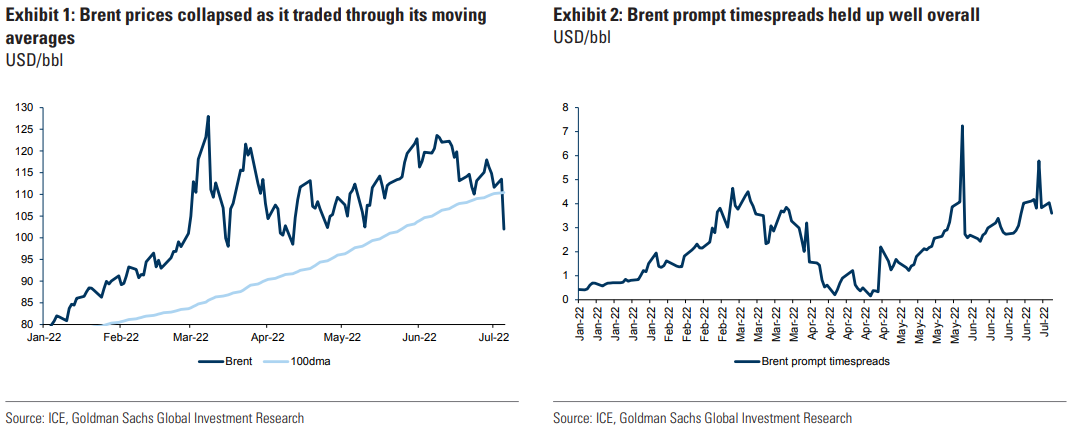

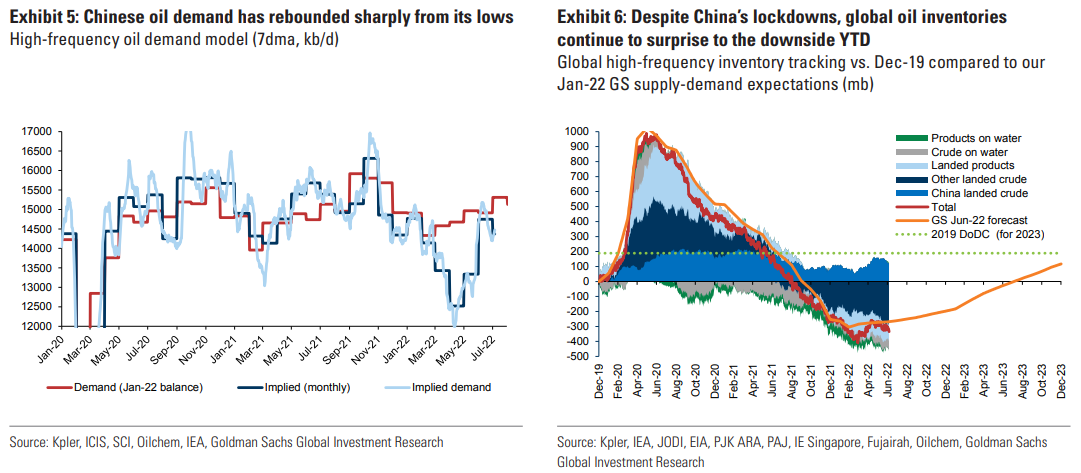

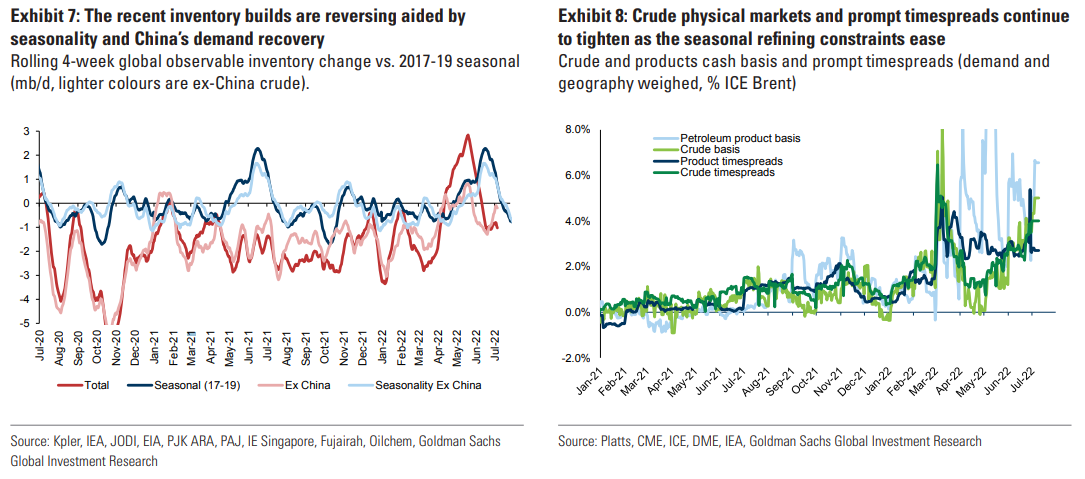

The fall in oil prices started at the US equity market open and coincided with a broad-based decline in other commodities and risky assets. As is repeatedly the case with oil, the move lower was then exacerbated by technical factors and trend-following CTA flows, such as Brent trading through its 100-day moving average, as well as through the strikes of puts with large open interest (where negative gamma effects invariably accelerate large price sell-off). It is important to finally note that this sell-off occurred amidst seasonally low post-July 4 trading liquidity. From this perspective, this sell-off in oil prices is not all that surprising, similar in set-up and magnitude as the one after Thanksgiving 2021, most recently.

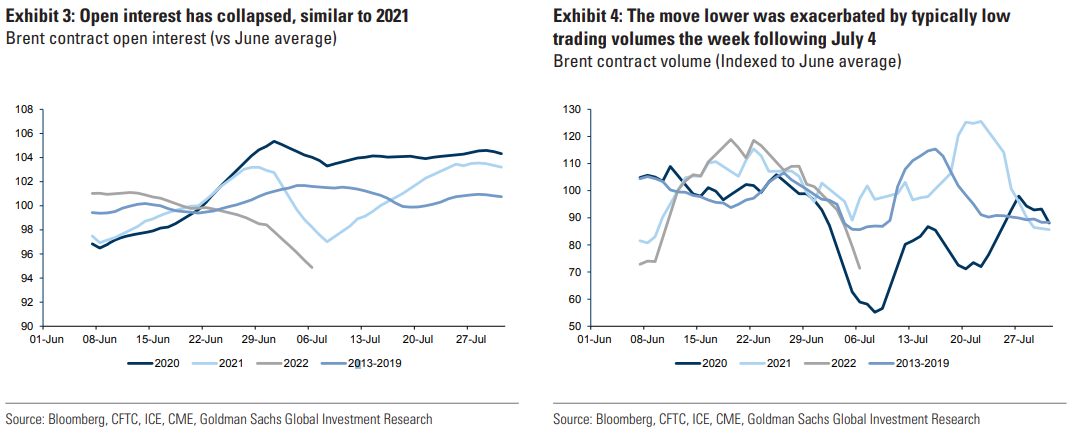

Fundamentally, we find little catalyst for today’s move, with the morning offering instead news of rising geopolitical tensions in Iran and record strong Saudi OSP to Asia, reflective of strong crude demand by refiners. Case in point, front-month Brent time spreads, diesel and gasoline cracks all weathered the fall in flat price, only down slightly on the day. In fact, the most notable move in oil prices in the past few days was the strength in crude timespreads and physical prices, reflective of a market still in deficit. This is consistent with our tracking of oil fundamentals, with an estimated global c.1 mb/d deficit in June, with China back to drawing inventories as well.

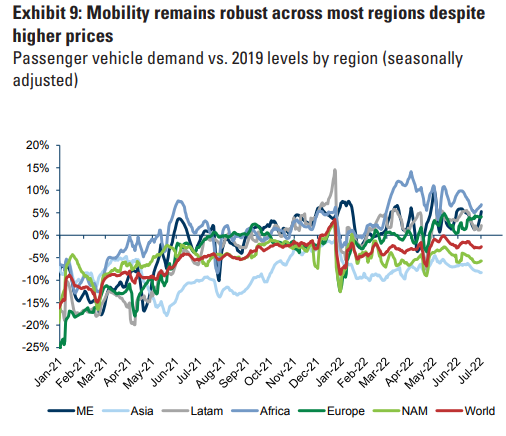

With concerns focused on the potential for a recession, we update our tracking of oil demand. Our mapping of daily mobility points to demand holding despite the surge in retail prices in June, with global jet fuel demand continuing its impressive recovery. Specifically, we estimate that onroad June demand was up c.2% year-on-year exc. Asia, consistent with (1) 2Q real global GDP yoy growth exc. China of 5% and (2) 0.9 mb/d of price driven demand destruction (based on global retail prices at a consumer Brent equivalent level of $170/bbl in June and our estimated 4% price elasticity for road fuels1). The $25/bbl decline in consumer fuel prices from June to July – based on the latest move in both refinery margins and Brent prices – would in turn support total oil demand by 0.8 mb/d based such an elasticity, with governments set to further stimulate demand through gasoline tax cuts. Stated another way, the move lower over the past two weeks is equivalent to the oil market downgrading its growth expectations by c.1.1%, all else constant.

While the odds of a recession are indeed rising, it is premature for the oil market to be succumbing to such concerns. The global economy is still growing with the rise in oil demand this year set to significantly outperform GDP growth, buttressed by the post-COVID re-opening in Asia-Pacific as well as the resumption in international travel. In addition, China’s demand rebound from its aggressive lockdowns is coming in ahead of our expectations, with its large stimulus further helping local demand improve later this year. As a result, we still expect that global oil demand will rise by a larger than seasonal 2.3 mb/d from 2Q22 to 3Q22 (at $120/bbl). This is what the oil market needs to solve for, with this demand rebound greater than the expected increase in supply in coming months. At the even lower spot prices, we estimate this deficit to reach 0.6 mb/d, an unsustainable outcome in our view given already record low inventory levels (vs. our $140/bbl 3Q22 Brent forecast which instead solves for no more inventory draws).

While our view remains that higher consumer prices are required to balance the oil market this summer, we acknowledge that significant and large shocks continue to distort fundamentals. So far, Russian exports have beaten our expectations given the lack of oil sanctions. However, this has been fully offset by production losses in Libya and Ecuador, with Saudi also producing less than expected in June based on ship tracking data. While it is hard to assume such supply disappointments continue, we note that rising social unrest at elevated fuel and food prices make such issues likely to reoccur. Of greater persistence, the rebound in Chinese demand appears to be exceeding our expectation so far, creating upside risks in 2H22 given the ongoing stimulus, as well as loosening Covid restrictions.

Our conviction remains on expressing our bullish view through Brent timespreads and long petroleum product flat price trades. As we discussed in our latest deep dive, the ramp-up in refinery runs this summer far exceeds the potential upside risks to Russian exports and downside risks to Chinese or global oil demand. This is driving crude inventories lower and to already record strong Brent timespreads (despite still being nearly a month away from expiration). An environment of tight physical markets but weak macro expectations would end-up having to resolve itself through extreme backwardation, a continuation of the trading pattern of the past year. From a directional perspective, we continue to recommend expressing our bullish view through long diesel/gasoil year-end trades, as it is ultimately the level of product prices (not crude) that needs to achieve the necessary level of demand destruction.