New Zealand house prices are tanking.

Following 2.25% of rate hikes from the Reserve Bank, the REINZ House Price Index plummeted 5.4% over the June quarter, with every major urban district registering losses.

In a similar vein, June’s Trade Me property index posted a “record breaking” monthly fall of 1.9% amid “skyrocketing supply”.

The scale of decline has reduced many Kiwi vendors to tears, according to Harcourts real estate consultant Alison Hawkes:

Sales are plunging by double digits. Prices just fell the most in 13 years. And homes that would have previously sold in days are now sitting on the market for weeks…

“We have to tell vendors that the market has changed quite dramatically and quite quickly. It’s not always easy,” said Hawkes…

“There are a lot of tears. A few months ago they were tears of happiness, now they’re tears when they realize their family home isn’t worth what they thought it was.”

Meanwhile, Brad Olsen, principal economist at Infometrics, observed that sales volumes across New Zealand have plunged to levels not seen in more than a decade, which signals prices will continue to fall:

“If we look at sales volumes at the moment, we’re going back more than a decade to see sales volumes as low as they are now outside of Covid lockdowns… That is quite a significant shift.”

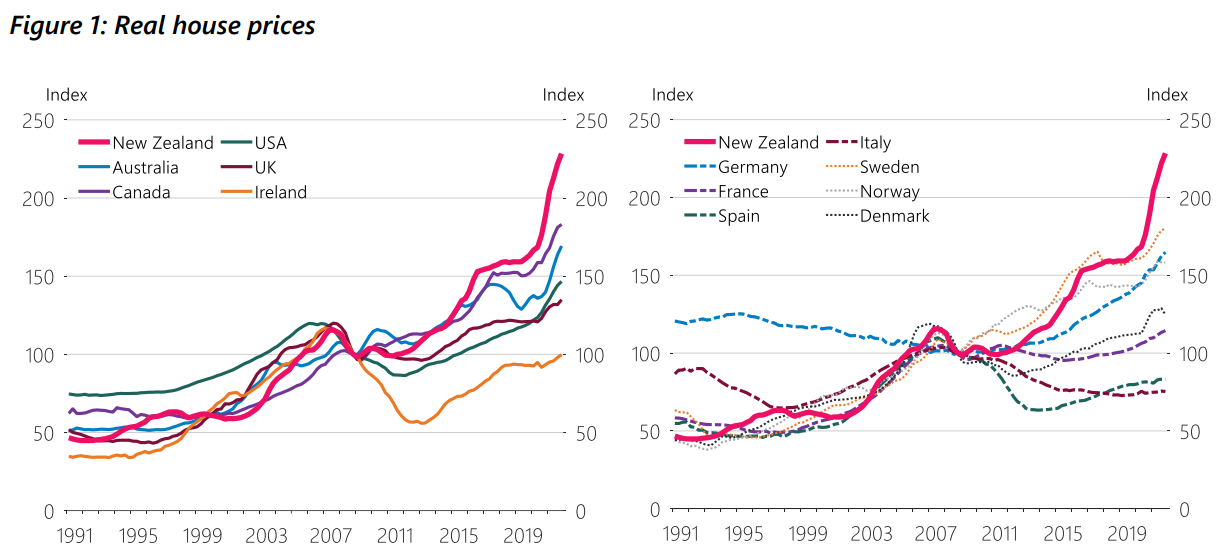

A year ago, New Zealand housing led the developed world in price growth, with values soaring around 40% over the pandemic:

New Zealand house prices experienced the strongest growth.

Now New Zealand’s housing market is considered the ‘canary in the coal mine’ for countries like Australia, given the Reserve Bank of New Zealand (RBNZ) was the first to hike interest rates.

A fortnight ago, the RBNZ stated that it would continue hiking interest rates aggressively in a bid to contain inflation, which hit a 32-year high 7.3% in the June quarter.

All of which means that New Zealand’s housing market will continue to plunge, inflicting more pain on the nation’s army of highly leveraged households.

After experiencing the developed world’s biggest boom over the pandemic, New Zealand’s housing market is now facing one of the biggest busts.