The Reserve Bank of Australia’s (RBA) aggressive monetary policy tightening of recent months is likely to see the nation’s quarterly mortgage interest bill rise to a record $19 billion by the end of 2022.

Judo Bank economic adviser Warren Hogan expects the cash rate to rise by 50 basis points to 1.85% in August. Hogan says the RBA should then pause rate increases for several months to assess the impact on the economy; he cautions that increasing the cash rate too quickly will heighten the risk of recession in 2023:

“What they have done so far is utterly appropriate, but now is the wrong time to continue to jack up rates by 50 basis points at every meeting,” he said. “If rates get to 3-3.5 per cent by the end of this year, there’s probably a better than even chance of having a shallow recession in early to mid-2023.”

Mr Hogan estimated if rates ended the year at 2.6 per cent, households would be paying a total of $18.9bn in mortgage interest by the December quarter – $8bn, or 75 per cent, more than a year earlier.

That would eclipse the previous quarterly mortgage bill high of $17.8bn in September 2011.

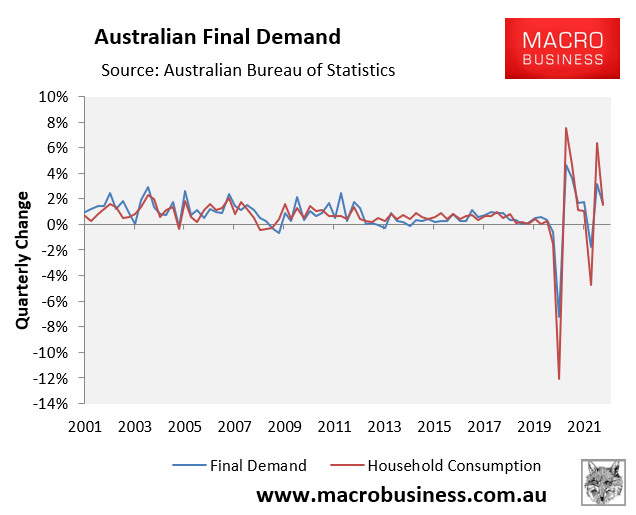

Household consumption is the Australian economy’s biggest growth driver, accounting for around 55% of growth on average. Therefore, where household consumption goes, the economy generally follows, as illustrated in the next chart:

Household consumption drives Australia’s growth.

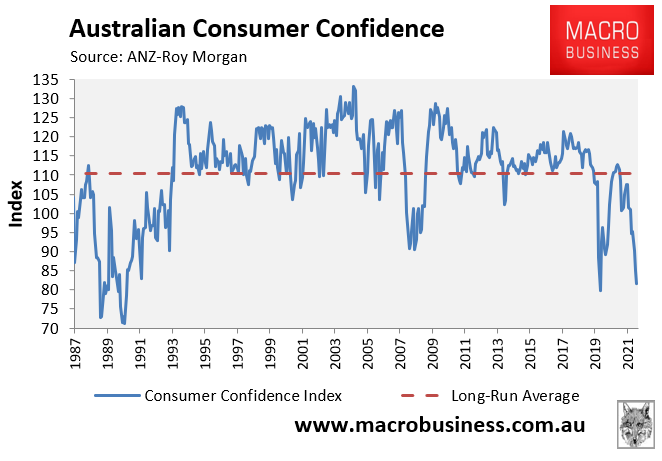

It is also worth remembering that the RBA’s monetary tightening began with Australia’s consumer confidence already at recessionary levels, running well below the Global Financial Crisis:

Australian consumer confidence is already at recessionary levels.

Therefore, the RBA must tread very carefully on interest rates. If it hikes too aggressively, it risks tanking both household consumption and house prices, and risks driving the economy into an unnecessary recession.

Judging by Tuesday’s speech by deputy governor Michelle Bullock, it appears the RBA does not grasp the gravity of the situation.