Michele Bullock, Deputy Governor at the Reserve Bank of Australia (RBA), has just delivered a speech playing down the risks of aggressive rate hikes on Aussie mortgage holders.

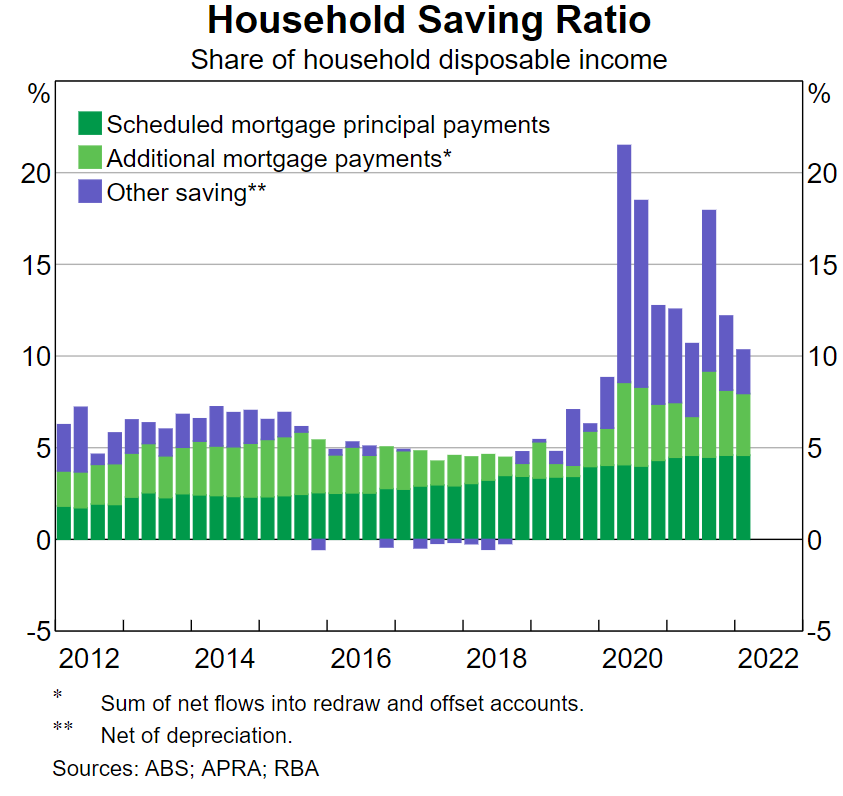

Bullock noted that only “around one-third of all households have housing debt”. Moreover, many have squirreled away savings over the pandemic and made additional mortgage repayments:

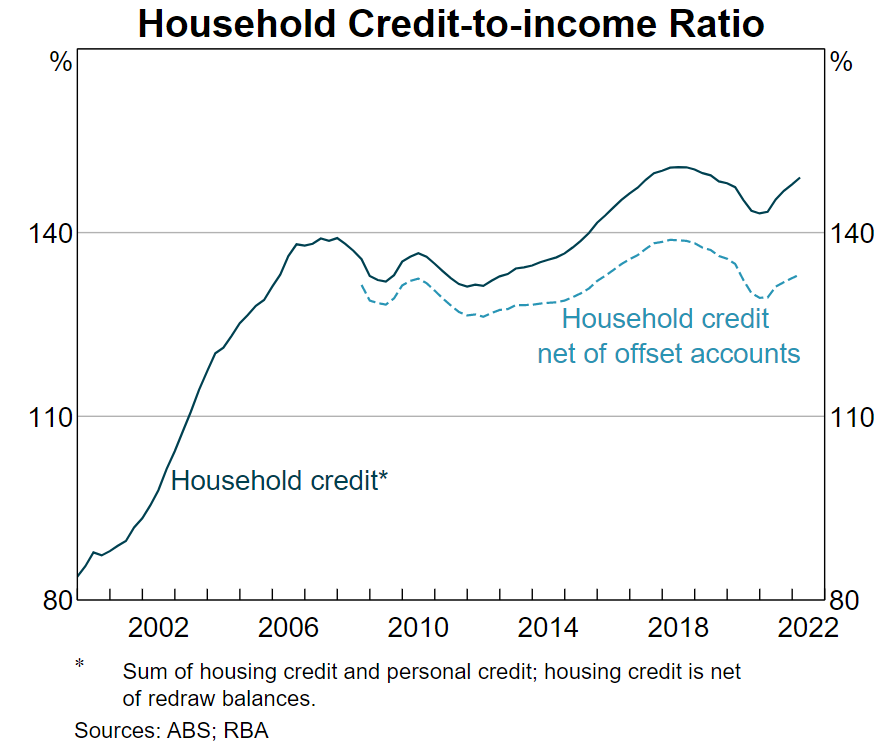

Accordingly, “the ratio of household credit to income is actually a fair bit lower than the headline figure and is around the same as its 2007 level”:

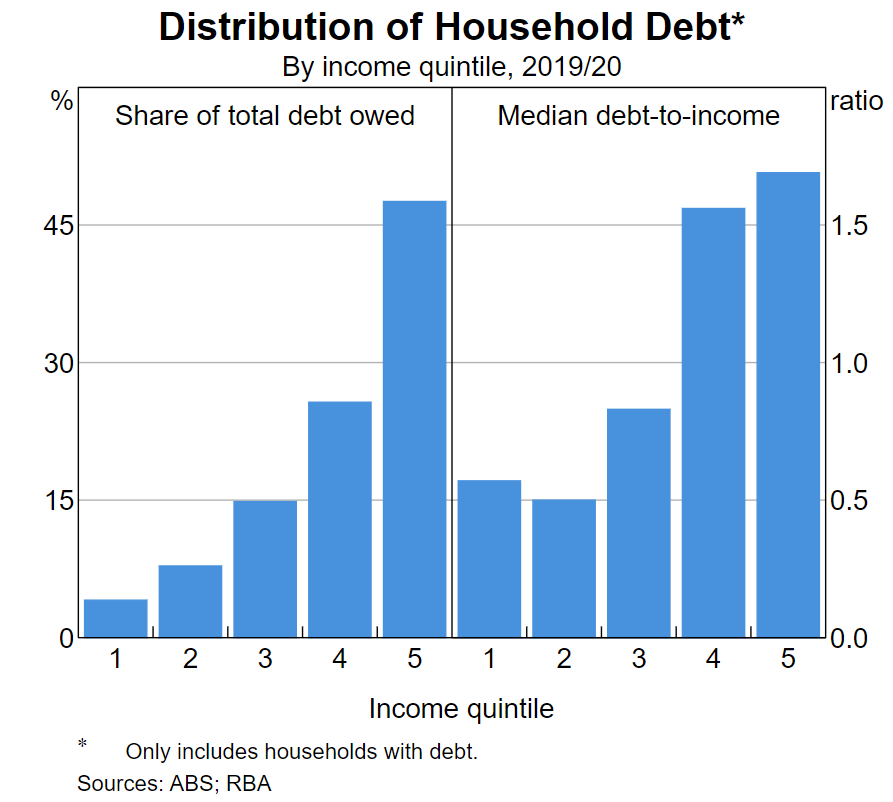

Moreover, “almost three-quarters of debt outstanding is held by households in the top 40 per cent of the income distribution”:

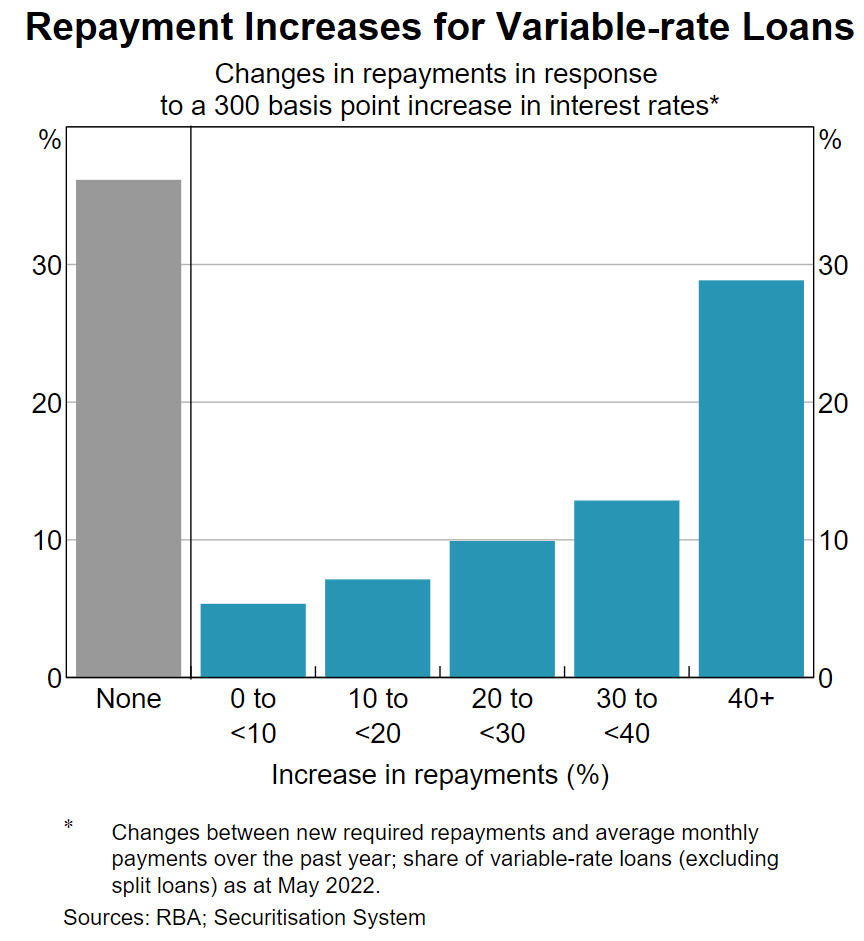

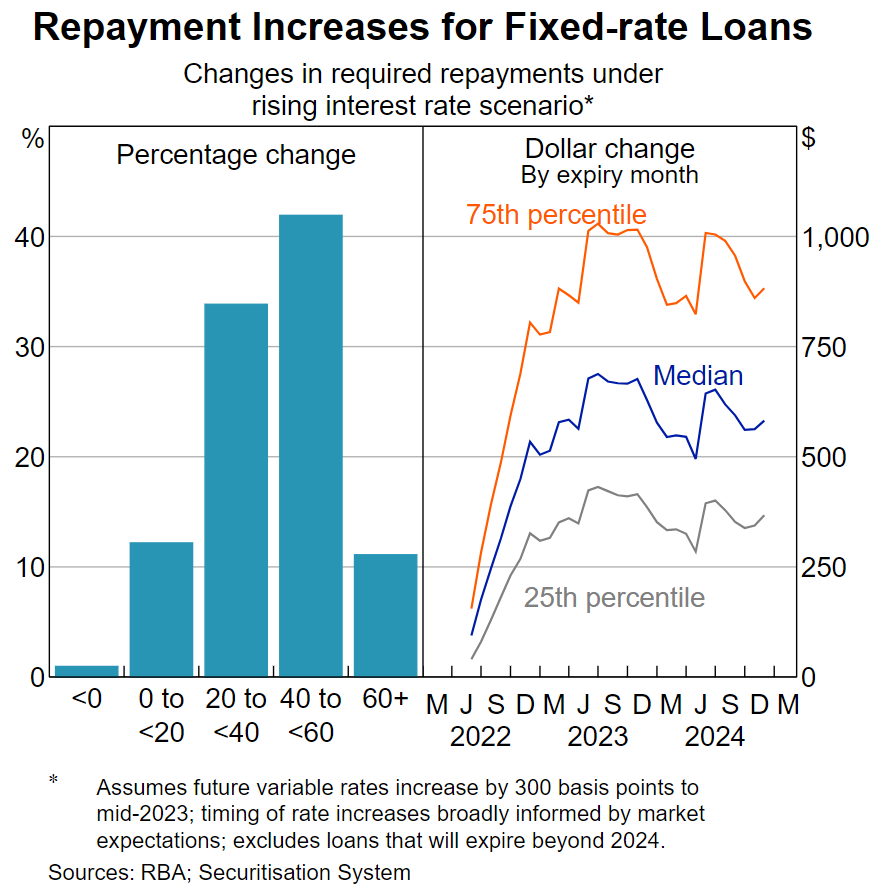

Nevertheless, “just under 30 per cent of borrowers would face relatively large repayment increases of more than 40 per cent of their current payments” if interest rates were to rise by 300 basis points – as predicted by financial markets:

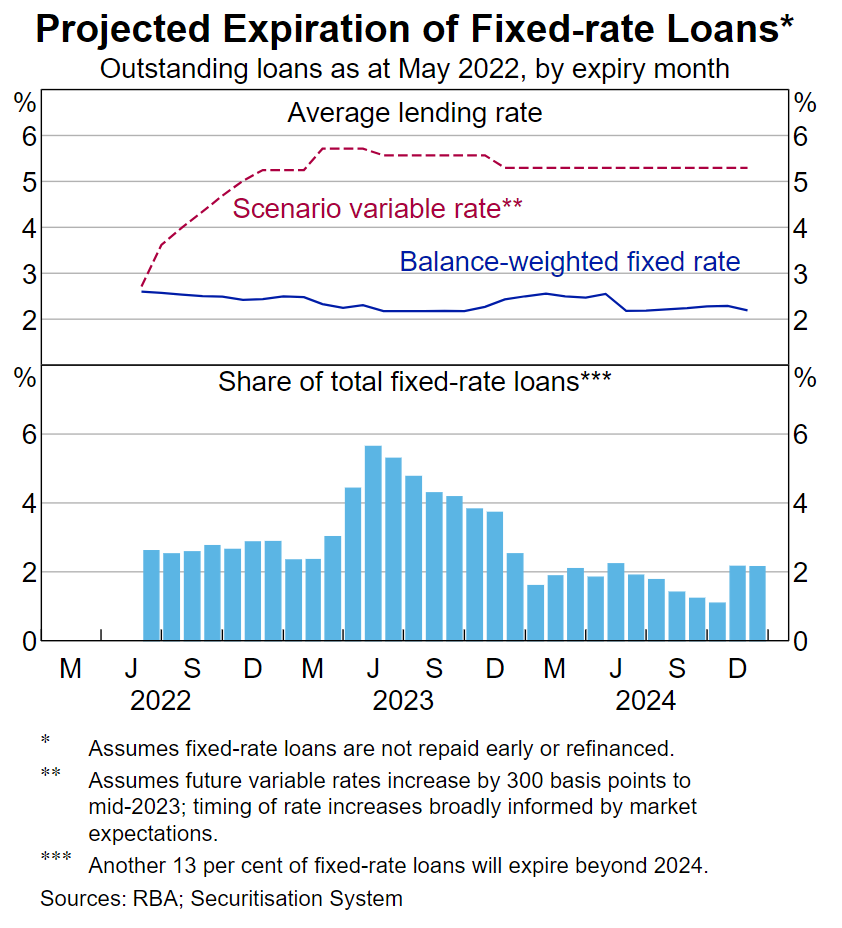

Furthermore, “the majority of currently outstanding fixed-rate loans are due to roll off within the next two years, with the greatest concentration of loans due to expire in the second half of 2023”:

Therefore, “assuming all fixed-rate loans roll onto variable mortgage rates and new variable rates are broadly informed by current market pricing, estimates suggest that around half of fixed-rate loans (by number) would face an increase in repayments of at least 40 per cent”:

Overall, Bullock concludes that there is nothing to see with respect to the impact of rate rises on the household sector:

I would conclude that as a whole households are in a fairly good position. The sector as a whole has large liquidity buffers, most households have substantial equity in their housing assets, and lending standards in recent years have been more prudent and have built in larger buffers for interest rate increases.

Much of the debt is held by high-income households that have the ability to service their debt and many borrowers are already making repayments well above what is required. Furthermore, those on very low fixed-rate loans have some time to prepare themselves for higher interest rates.

I obviously strongly disagree. You cannot hike mortgage repayments so aggressively without severely denting household consumption – the economy’s biggest growth driver.

Either way, it will be interesting revisiting this speech in a year’s time to see how it has aged. Either Bullock will be right, or I will be.