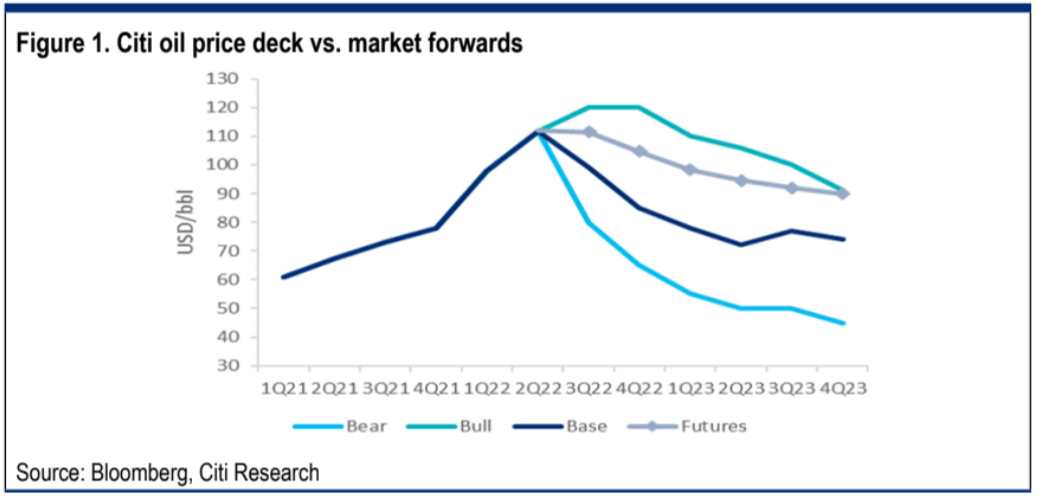

Citi believes a global recession could drive oil prices to $US60 a barrel by year end and to $US45 a barrel by end 2023. Here’s hoping:

It has become common wisdom to compare oil markets today with the energy crises of the ‘70s – the spike following the OPEC oil embargo (1973-74) and the further spike along with the Iran-Iraq War (1980), both of which induced recessions and were accompanied by high inflation and record high interest rates. As in the ’70s, so today there are significant changes in energy supply chains that distorted markets and supported higher prices. However, there are also differences that make a comparison with the deflationary aspects of the Great Financial Crisis seem a more appropriate analogy for 2022-23.

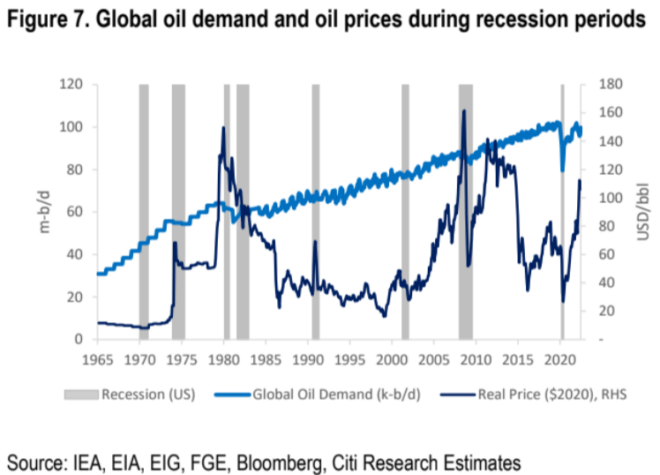

Like then, so today high energy prices preceded the events that triggered a recession. Brent crude oil breached $140/bbl in Jul’08, equivalent to over $160/bbl in real terms, only to fall to $40/bbl by year-end before re-balancing at $90/bbl deferred and remaining there for the next four years.

Most analyses of oil markets emphasize the consequences on prices of further supply disruptions. In this report we focus on the potential consequences of an increasingly likely recession. In a recession scenario with rising unemployment, household and corporate bankruptcies, commodities would chase a falling cost curve as costs deflate and margins turn negative to drive supply curtailments.

Recessions see commodity demand decline and surpluses develop. Surpluses require prices to fall until supply is curtailed, falling below production costs to restore equilibrium. During recessions, production costs tend to fall, as energy prices are important cost inputs to other commodities, creating a pro-cyclical downward loop for prices.

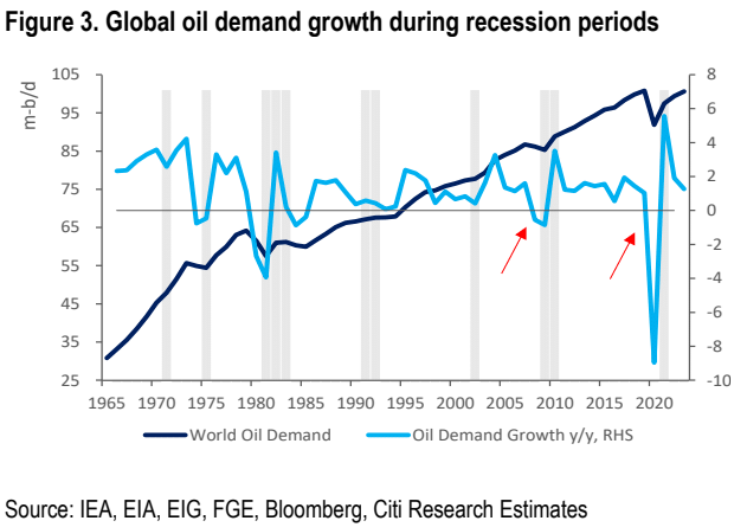

For oil the historical evidence suggests that oil demand goes negative only in the worst global recessions. But oil prices fall in all recessions to roughly the marginal cost — We run a historical analysis on global oil demand impacts through previous recessions based on US recession over the last 60 years. The historical evidence suggests that most downturns are accompanied by demand slowdowns. The Financial Crisis and the pandemic outbreak are two notable exceptions, while the Second Oil Crisis preceded a permanent demand destruction in the power sector, which back then consumed 30% of oil supply.

It looks as though for this year and into 2023 Russian crude oil exports may remain robust, even if refined product exports may fall. Therefore, further global oil demand weakness should spell higher inventories and weaken oil prices. Yet, the distortionary impacts of Europe boycotting increasing volumes of Russian oil should continue to be headwinds for global oil prices. In a recession scenario, we would see oil prices falling to $65/bbl by year end and potentially to $45/bbl by end-2023, absent intervention by OPEC+ and a decline in short-cycle oil investment.