Alex Turnbull has written a nice piece on what’s coming from China. What matters in this is that China is developing a huge energy price advantage as it dislocates its local coal prices from the global shock delivered by Russian sanctions by buying cheap Russian energies and producing more of its own coal. This leaves it in a competitively advantageous position to export manufactured products, especially those most dependent upon energy input costs. That is, metals processing and similar.

On the other hand, Albo’s cowards are protecting Aussie war-profiteering in the same commodities impacted by Russian sanctions and exposing local energy-intensive manufacturers to European-level cost inputs.

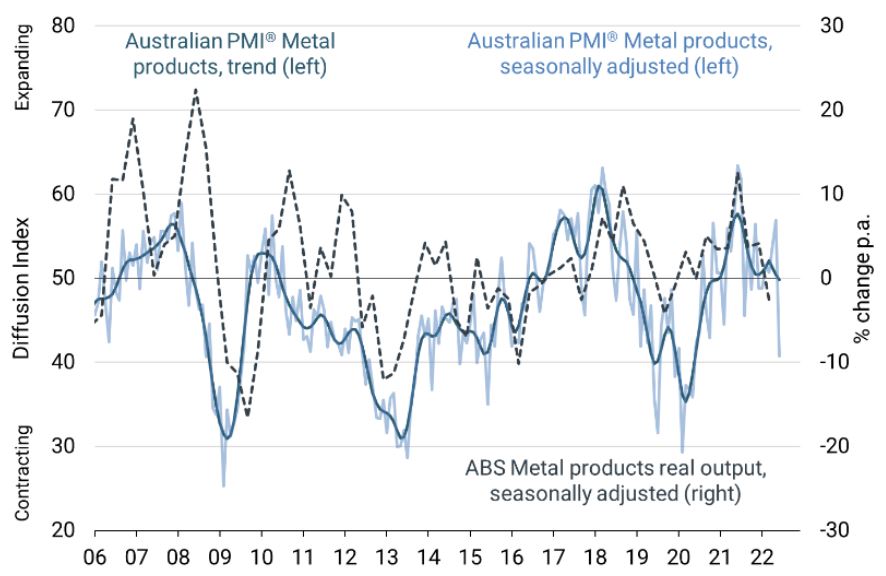

In short, Australian metals processing is about to be wiped off the face of the earth as it is supplanted by Chinese output. This is already apparent in the new PMI:

Needless to say, as our relationship with the CCP strucuturally deteriorates towards outright strategic competition, making ourselves ever more depedent upon Chinese produced metals is pretty mcuh as stupid as it gets.

—

China is Exporting Deflation (Again)

In a development that represents a return to “normal” China is exporting deflation again. This will lead to markedly lower goods inflation elsewhere and – pending improvements in current logistical constraints – much lower energy prices. Before showing all the examples and what this means let me be specific about what “exporting deflation” is.

- China’s input costs need to fall for external reasons, or margins need to fall for domestic producers due to lower demand.

- China then exports the surplus abroad.

- There is capacity for the world to import. This seemed obvious before COVID the logistical nightmares of the last few years but a combination of freight capacity and free trade allows this to happen. Shipping rates for containers from China to the US are now cheaper than they were a year ago according to Freightos so this applies once more – see below.

Lower Input Costs

Steel

China now is buying more coal from Mongolia and its coking and thermal prices have now dropped to levels last seen prior to the Ukraine invasion. This trend is not stopping in fact recent news of automated borders, rail and the like indicates it will continue. Steel in a blast furnace takes two principal inputs: iron and coke from coking coal. Both have dropped recently but coking coal has a genuine supply shock incoming from Mongolia and for seaborne, reduced imports. This is taking a simple cost index for steel much lower and depending on how much China’s real estate sector slows iron could well follow leaving steel prices back at prices last seen in 2015-2016. For now China steel futures in yellow are tracking costs lower and North American European prices are following.

A lot of things are made of steel, and a lot of those things are made in China or compete with China prices. Update your priors on the cost of infrastructure projects and cars accordingly.

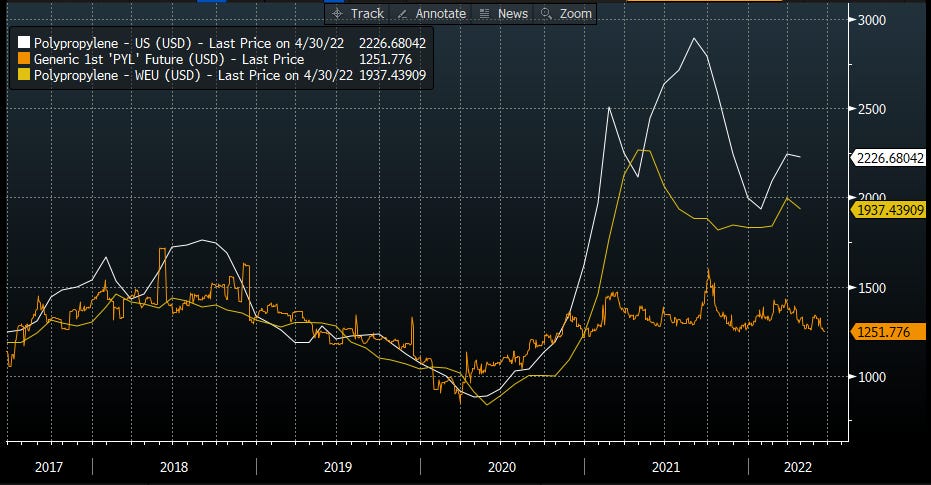

Plastics and Chemicals

China helpfully has a liquid futures market for key plastic resins that make up much of global plastics production that can be readily compared to international prices. Something is clearly going on right now: China prices are collapsing, US prices are up, but not absurdly so and Europe is suffering a terrible price shock because gas is a key input. The underlying cause is the Ukraine invasion: China can import cut price gas and crude from Russia, the US uses local gas and crude and Europe pays obscene prices for whatever Russian gas it can still get. Prolypropylene goes into everything and has wildly different prices globally which as not happened before (Europe in yellow, US in white, China futures in orange).

I would be shocked if China did not export a lot of plastics until this arbitrage closes. Europe needs the supply and the less it produces domestically until it has more LNG importing capacity, the better it can survive this winter. The upshot is that plastic prices go down and track the Ukraine shock less and China’s domestic costs more with significant impacts on producer prices and in time, consumer prices.

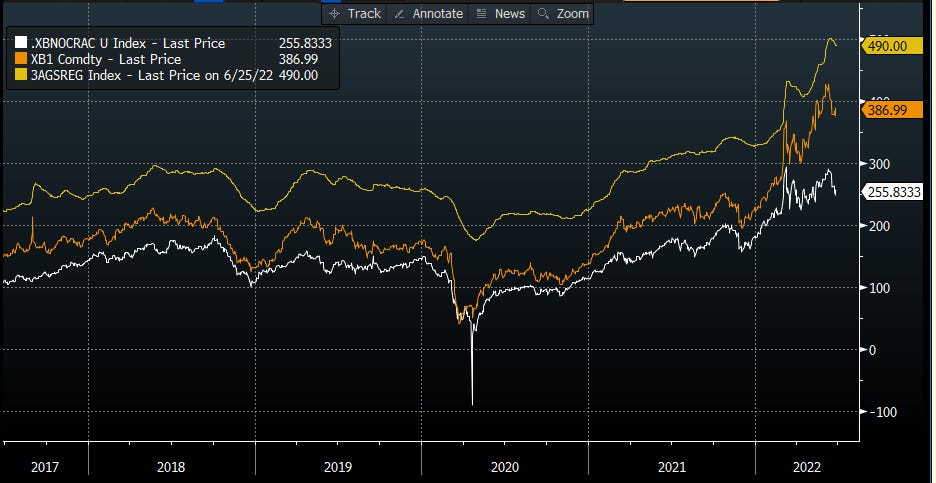

China has a major opportunity here to signal a diplomatic switch which astute China watchers are seeing in some personnel changes in the Chinese government. China has a genuine oversupply of refining capacity and until 2021 was a major exporter of refined products like diesel and gasoline. The pain at the pump in the US is as attributable to genuinely tight crude markets as it is to a squeeze in refining capacity especially in Europe which has led to Europe importing those products from the US in turn spreading the pain. This can be seen in the “crack spread” or the difference between refinery outputs – gasoline, diesel and the like – and oil, the refinery input. Below are retail gas prices in yellow in cents, futures prices for gasoline in orange and gasoline without the crack spread in white. A normalization in spreads would take gas down to 310c or so – or barely above the pre Ukraine conflict pricing.

If China were to want to signal that is not on a unity ticket of economic warfare against the West in conjunction with Russia then expanding fuel export quotas would be a good way to do it. Gasoline and diesel prices could fall 15% or more providing substantial relief to economies that are major importers of China’s exports – in turn providing some stabilization to its own economy. If not it would be wholly reasonable for the EU and US to conclude China is committed to a campaign of gray zone economic warfare against them in conjunction with Russia. It is not hard to conceive there being even further strategic disengagement with China if that were the case.

China has an opportunity to show where it sits now: it can be militarily disengaged with the conflict while trading with everyone, an enviable position to be in and something the west should tolerate since China is clearly buying Russian exports at much lower prices now. Unlike Saudi Arabia which may or may not have much spare production capacity, China’s refining capacity is known and underutilized and its export quotas are lower than they were previously. It is hard to say no because unlike Saudi Aramco capacity the Shandong Teapot refiners are not a state secret.

Other Metals

China’s relatively slower cadence of growth is pushing copper prices lower in turn lowering the cost of key inputs for the energy transition. Far be it from me to determine China’s housing policy but a country whose population has peaked and whose key homebuying cohort is shrinking quickly does not need a housing construction boom. Below you can see the size of the classic homebuying cohort of young adults – it is shrinking quickly, and fertility rates are barely over 1 in most of China according to official data and alternative sources show numbers even lower – check Yi Fuxian’s work for examples. I cannot rule out China backsolving for growth using apartments, but I can support China backsolving for growth using renewables which structurally reduce fossil imports and energy inflation.

Coal

Thermal coal prices are higher than they have ever been as Russia makes up 300 million tonne of a 1.1bn tonne export market. China has responded by mining more of its own and importing vastly less – this year is tracking to have the lowest imports in well over a decade and the imports China is taking are from Mongolia and Russia which are otherwise lost to global markets. Australias output is still recovering but the big squeeze on thermal coal is likely to stick as Asian countries switch to burning more coal than gas. Not much joy here as yet but if China were not importing vastly less than last year coal would probably be a lot higher.

Is China Going to Export the Surplus?

Thus far things are looking positive. China is importing more coal from Russia and Mongolia and investing in making that easier. Similarly, it is exporting less from Indonesia in yellow below and exporting more steel in white below. Trade data for plastics, aluminium and other products that may be in surplus due to China’s real estate slowdown will be telling over the coming months. In normal circumstances this might be seen as bad and an excess capacity problem but today that is not the case. These are energy intensive products and they displace fuel demand elsewhere. China should get a free pass this this shock is over. This will also helpfully smooth the impacts of China’s real estate slowdown for China domestically – something they are concerned about.

In marked contrast to last year China is a very beneficial and benign influence on inflation dynamics now. If this can be maintained through this winter as LNG export terminals are built in the US and import terminals and FSRUs are built in Europe this is likely to moderate the inflation shock markedly. This in turn is going to give Russia vastly less leverage: Putin likely has one shot on goal to break Europe’s will this winter and if he fails he will likely never again get a chance. China could push its foreign policy back towards highly commercial self interest and impartiality, something that would be very desirable if it wants to retain good relations with Europe. One way or another we are going to see where China stands on this invasion through energy policy and one can only hope we see a return to China looking after China’s interests and not those of Russia at the expense of its own.