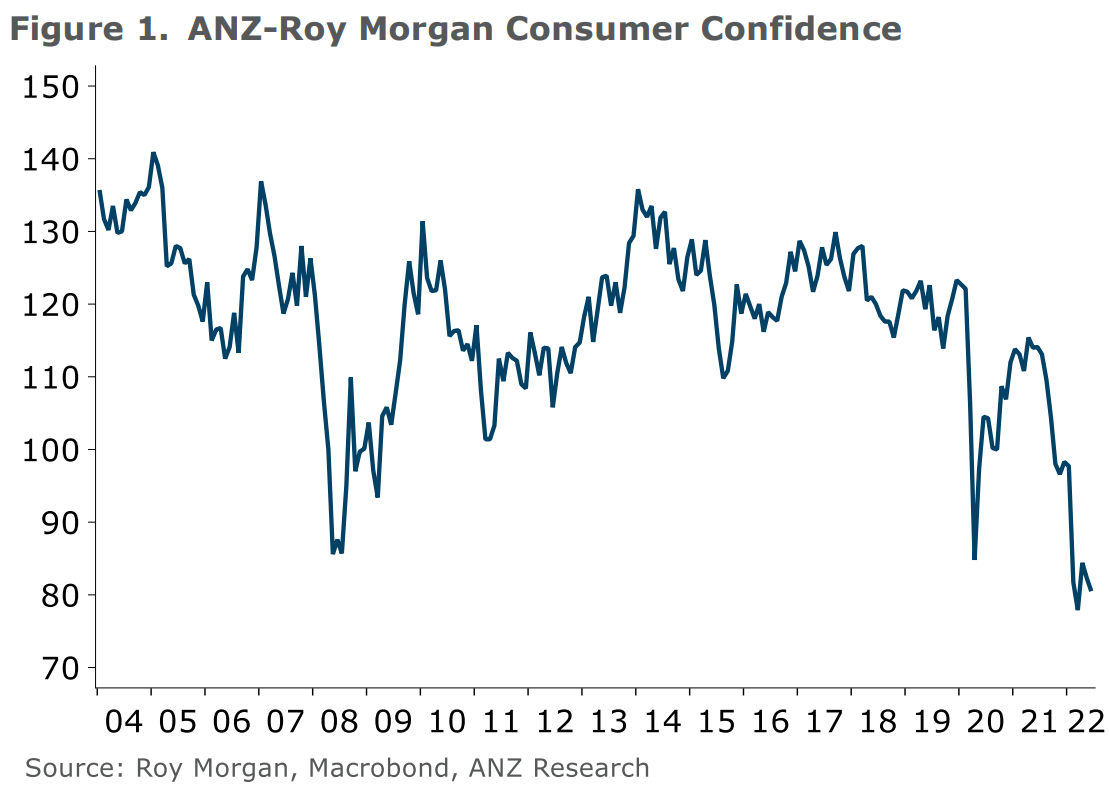

The latest batch of consumer confidence reports for New Zealand shows that Kiwis remain extremely depressed on the back of soaring inflation and interest rates.

ANZ-Roy Morgan’s confidence composite gauge is also pointing firmly towards recession:

Advertisement

Households are dealing with a lot right now: incomes not keeping up with inflation, lifting interest rates, falling house and other asset prices, and ongoing COVID and general economic uncertainty…

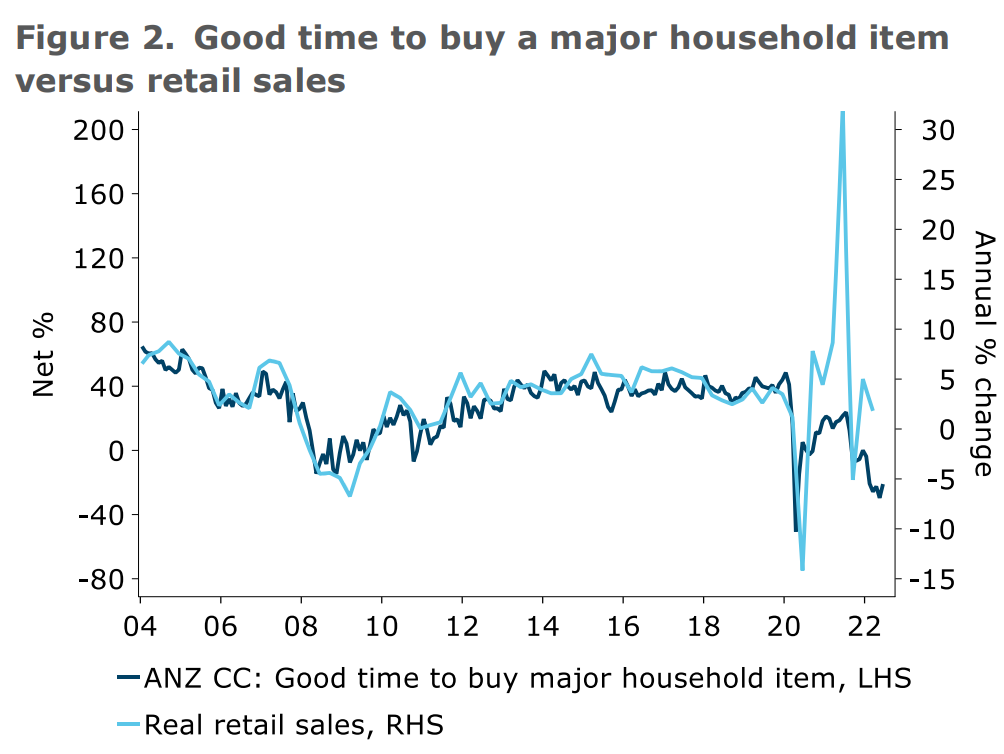

Overall, these data are sending sobering signals about the outlook. In particular, retail spending could soon find itself on the ropes if consumers follow through with their stated answers to the question of whether it is a good time to buy a major household item. So far, spending has been holding up (figure 2), but this is an ominous sign for retailers nonetheless…

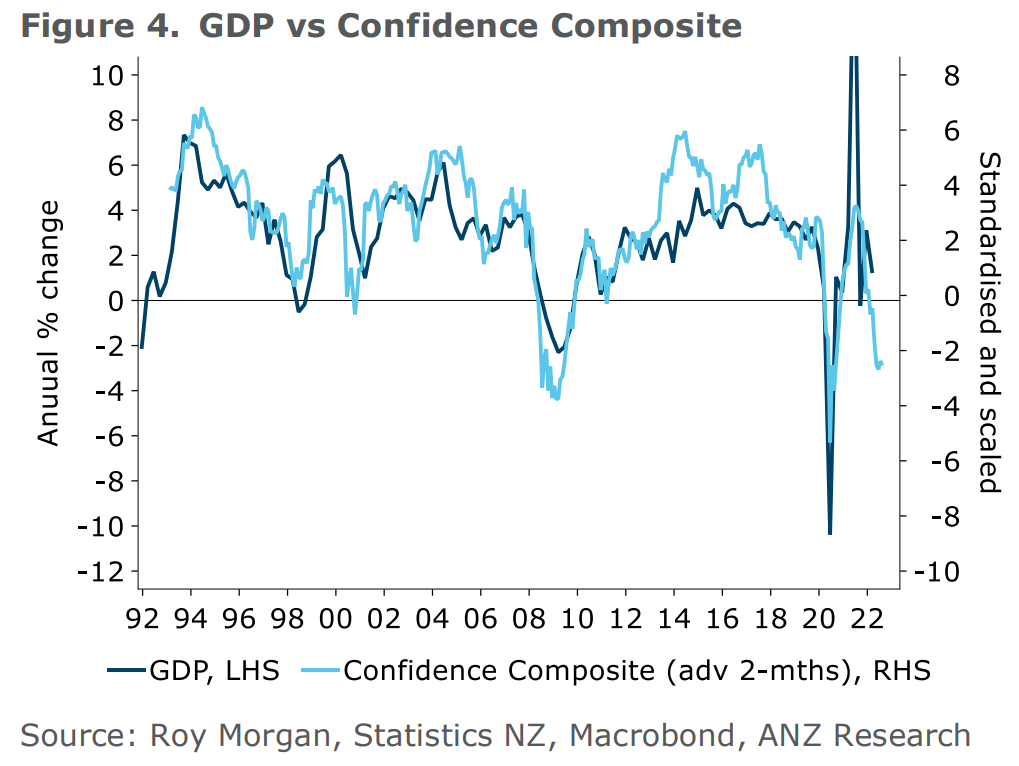

Our confidence composite gauge combines lagged Business Outlook expectations and intentions with consumer sentiment (figure 4). Still at recessionary levels, it continues to highlight downside risks to the outlook…

The latest Westpac McDermott Miller Consumer Confidence Survey also recorded the worst kiwi consumer confidence reading in records dating back to the 1980s, alongside the lowest “Good time to buy a major household item” result on record, which is the strongest indicator for household consumption.

New Zealand’s poor consumer confidence is understandable. It is also likely to get even worse.

Advertisement

Like everybody else across the globe, Kiwis are experiencing soaring cost-of-living on the back of global supply shocks. These shocks have sent inflation soaring, which has prompted the Reserve Bank of New Zealand (RBNZ) to aggressively hike interest rates.

New Zealand’s official cash rate (OCR) has soared from 0.25% in August to 2.0% currently, which has sent fixed mortgage rates (which comprise the majority of mortgages) to around 6%.

Worse, the RBNZ’s ‘forward track’ guidance has the OCR nearly doubling to 3.9% by June 2023, which would mean the tightening cycle is only around half way through.

Advertisement

As the majority of New Zealanders are on fixed rate mortgages of less than two years, most that originated mortgages at rock bottom rates over the pandemic are yet to be impacted the OCR hikes. But they know that Judgement Day is coming and they will soon be forced to refinance at double mortgage rates, which helps to explain why Kiwis are so depressed.

Related to the above, house prices have fallen heavily in response to rate hikes, down 9.2% from their November 2021 peak. The stock of unsold homes has also ballooned as buyer demand has collapsed. The housing correction is certain to worsen as monetary policy tightens, with New Zealand facing its biggest house price correction in generations.

The upshot is that Kiwi’s major asset is plunging in value at the same time as their cost-of-living (including mortgage costs) are soaring. In a nation so obsessed with housing, this is a recipe for dissatisfaction and pessimism.

Advertisement

Finally, ANZ’s latest business outlook survey showed that residential construction intentions have collapsed, slumping to -50 in May from -37 in April. This, in turn, points to a sharp slowdown in building activity.

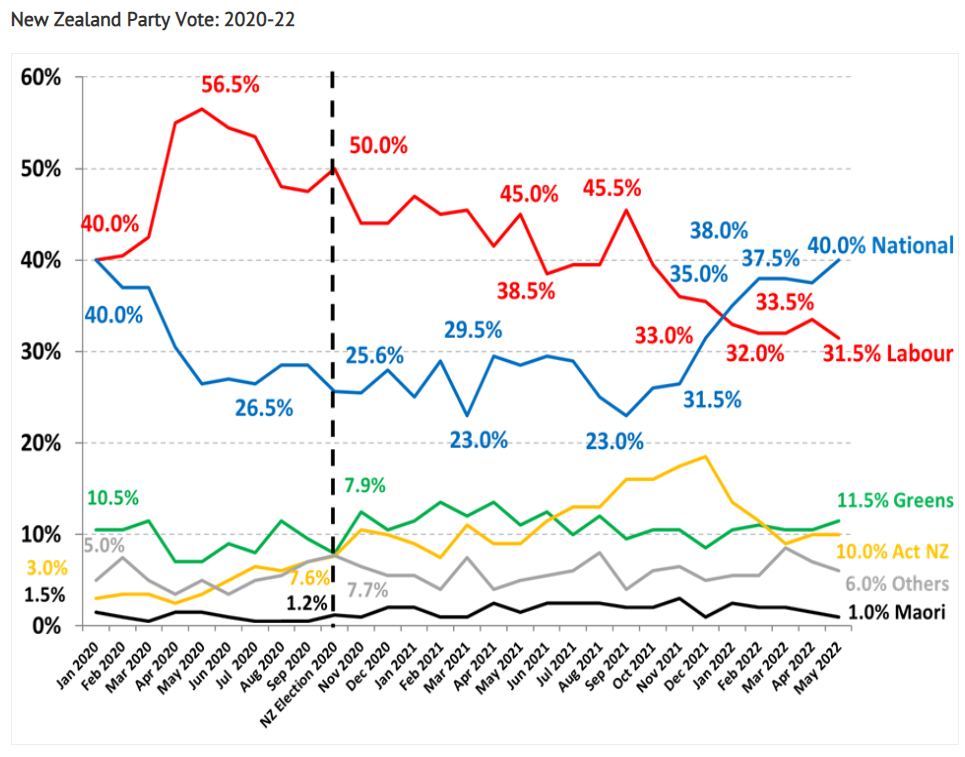

The timing could not be worse for the incumbent Ardern Labour Government, whose voter support has already collapsed since the RBNZ commenced its rate hiking cycle in October:

Kiwis no longer love Jacinda Ardern’s Labour.

Advertisement

As shown above, Labour’s party vote has collapsed from 45.5% immediately before the RBNZ’s first rate hike to 31.5% in May – a massive 14% decline.

With the next New Zealand election due in late 2023, and Kiwis confronting soaring mortgage costs, plunging house prices, and a potential recession, Jacinda Ardern is staring at near certain electoral defeat. Worse, she can’t do much about it, given the RBNZ holds the interest rate lever.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.