New Zealand’s housing market suffers biggest price fall on record

On Wednesday, the Real Estate Institute of New Zealand (REINZ) released its May price results, which reported that median prices nationally tanked by 4.0%, taking cumulative losses since November 2021 to 9.2%.

In a similar vein, the Trade Me Property Price Index for May also recorded the steepest monthly decline on record, with national average prices falling 2%:

Trade Me Property sales director Gavin Lloyd said it was the largest month-on-month drop the website had recorded, and showed the tide was turning after relentless price growth over the past couple of years.

“Often, prices cool a little as we go into the colder months, but last month’s data is beyond anything we’ve seen in previous years,” he said. “The whole market is in flux, and we’re seeing this reflected in every corner of the country.”

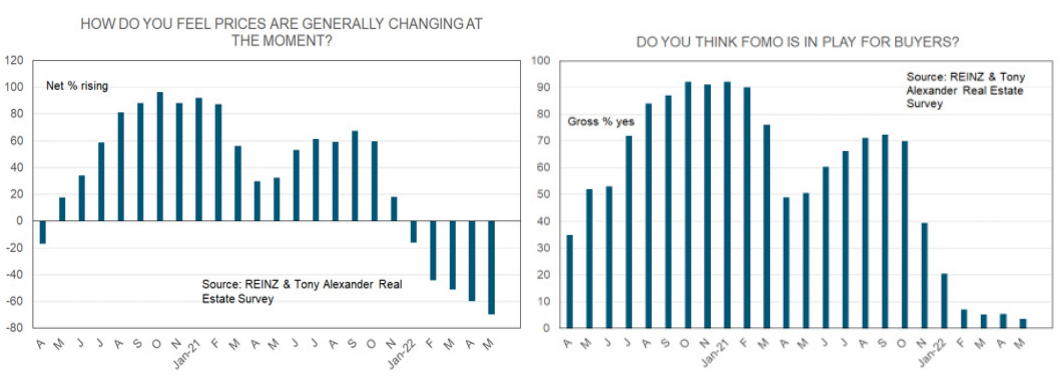

The fall in prices follows the largest lift in the number of homes for sale on record, which has eliminated buyers’ “Fear of Missing Out” (FOMO):

Nationwide, the number of properties for sale increased by 48% in May compared to the same time last year. That was, again, the largest percentage jump recorded by Trade Me and resulted in a record-breaking number of listings.

Every region had more properties for sale in May than they did at the same time last year…

Lloyd said in addition to the cooling prices, demand for properties dropped by 9% nationwide, compared to the same time last year…

“Having more options than ever before is taking the pressure off buyers and eliminating the fear of missing out that was behind much of the price increases over the past couple of years…

“As a result, the market has seen a remarkable shift, putting buyers well and truly in the driver’s seat.”

Trade Me’s results correspond with the REINZ’s June survey of licensed real estate agents, which reported widespread price falls amid vanishing FOMO:

Kiwi buyers go cold on New Zealand property.

In short, New Zealand looks to be experiencing a sharp housing correction on the back of 1.75% of official interest rate hikes by the Reserve Bank since October 2021.

The correction will intensify if the Reserve Bank follows through with its ‘forward track’ guidance and lifts the official cash rate from 2.0% currently to 3.9% by September 2023. If that happens, New Zealand faces a full blown house price crash.