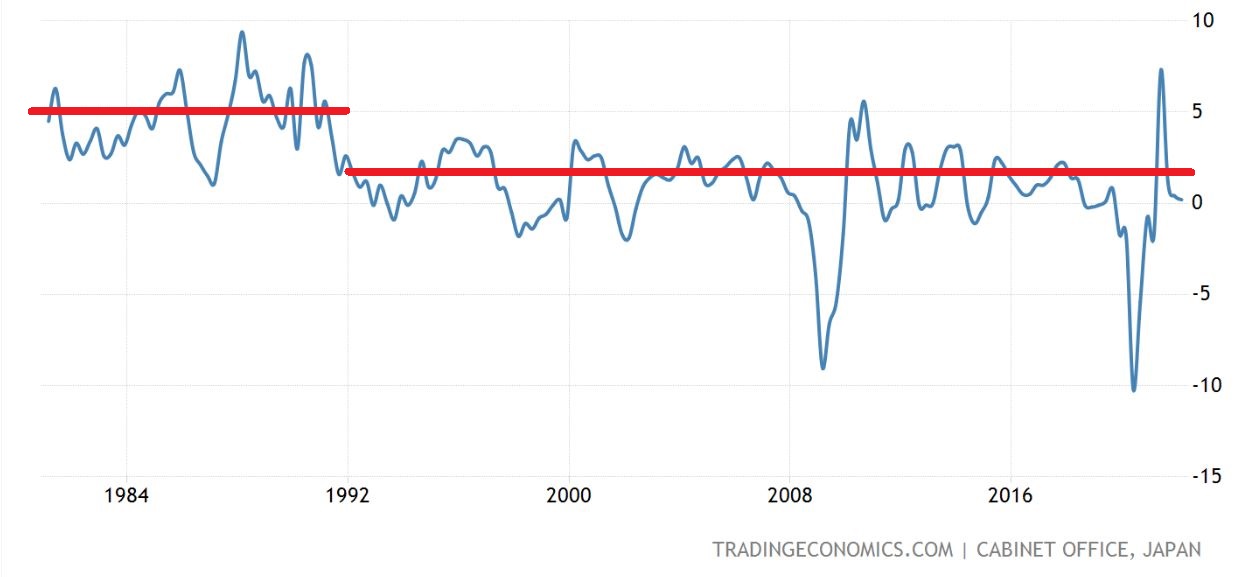

We’ve seen it before. In 1990, in Japan, the end of its property catch-up development phase was the end of its growth phase:

Now it is coming to China and the implications are the same. Jeffries:

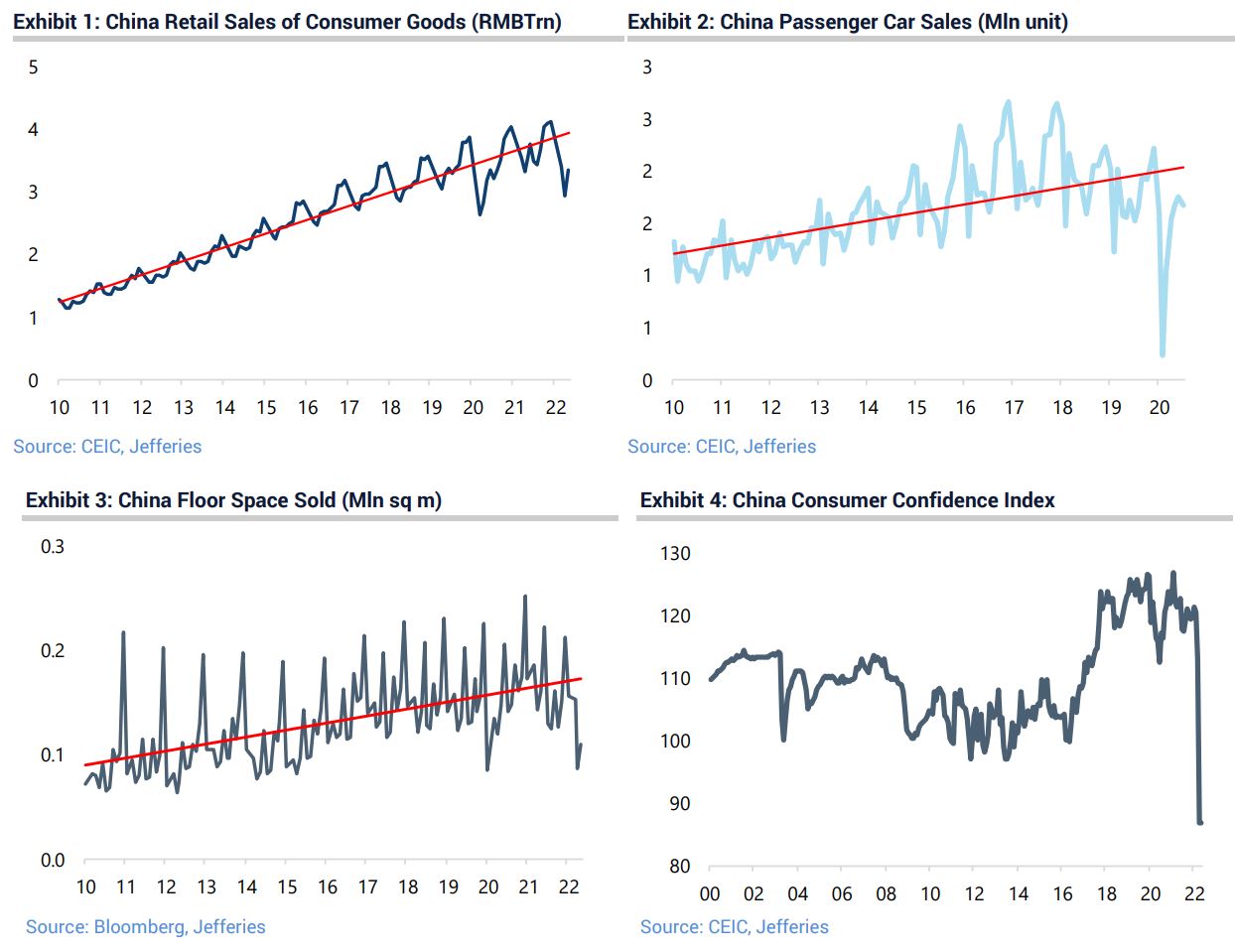

Although real money supply has begun to pick up, the money velocity of sectors connected to the real estate sector is experiencing a drought. In contrast to other economies, land sales make an enormous impact on local government tax revenues —often more than 30% of the total tax base. The earlier crackdown on the property sector, coupled with the Covid restrictions and weak employment conditions, has undermined demand for homes. In turn, land sales have collapsed (see RHS), and this has choked local government finances. We have highlighted previously the role of Local GovernmentFinancing Vehicles (LGFV) in both the local real estate market and the regional economy. In this sense, the authorities have recognized the need to break ‘the Gordian knot’ by allowing RMB1.5trn local government of special bond issuance in June for 2H22 infrastructure spending. They must hope that this kickstarts the velocity of money within the provinces, providing some relief to the banking sector, offsetting some of their exposure to the real estate sector. Ultimately, a turnaround in land sales will be needed to resuscitate local government purses.

Advertisement

As I have been saying, the recent bond infrastructure “stimulus” is simply replacing lost revenue with debt. It’s not stimulus at all.

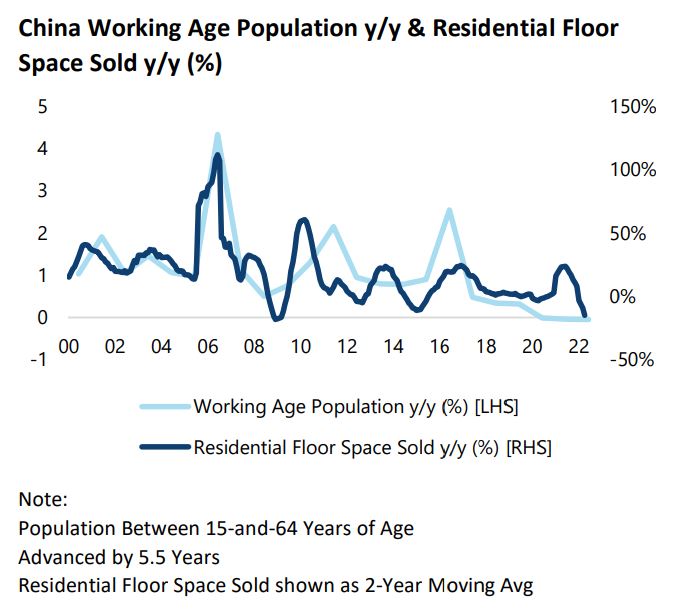

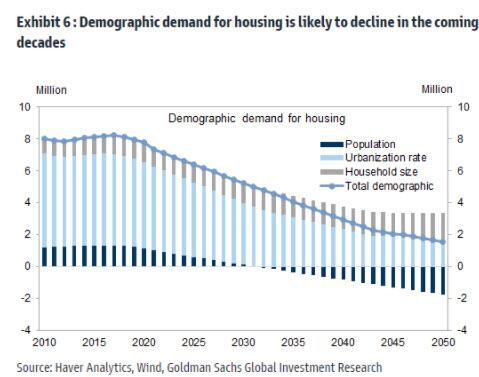

The larger problem is that this is all structural. The working age population is now falling in China so there is no household formation to drive over-building any longer:

Advertisement

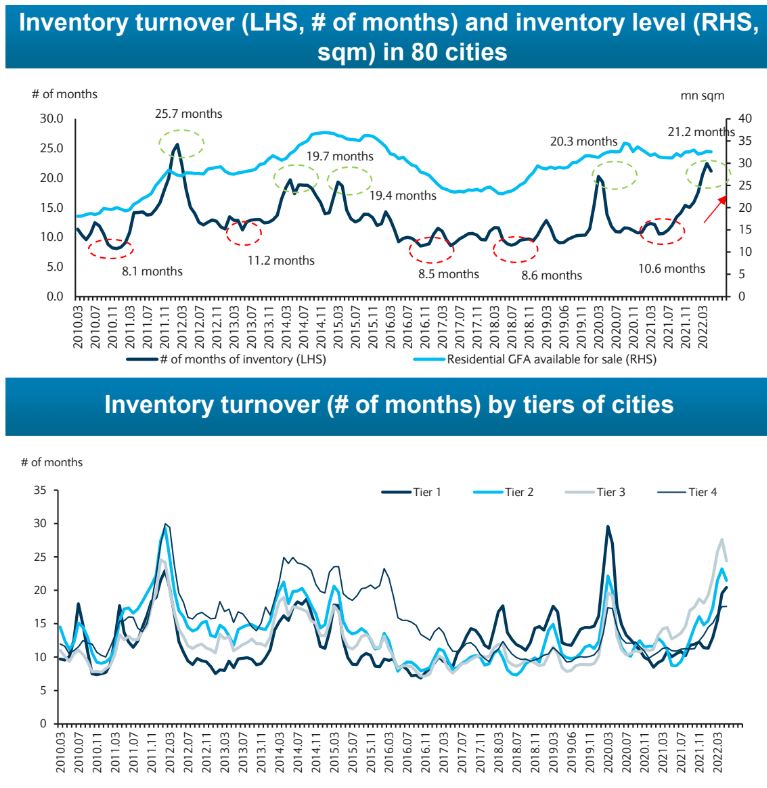

And there is already a vast surplus:

Given the structural nature of this adjustment, China needs a land tax to substitute for crashed land sales otherwise infrastructure building will also fail.

The spillovers are vast. 70% of household wealth is tied up in realty so it’s going to weigh on any attempt to rebalance towards consumption, not least as the population ages:

Advertisement

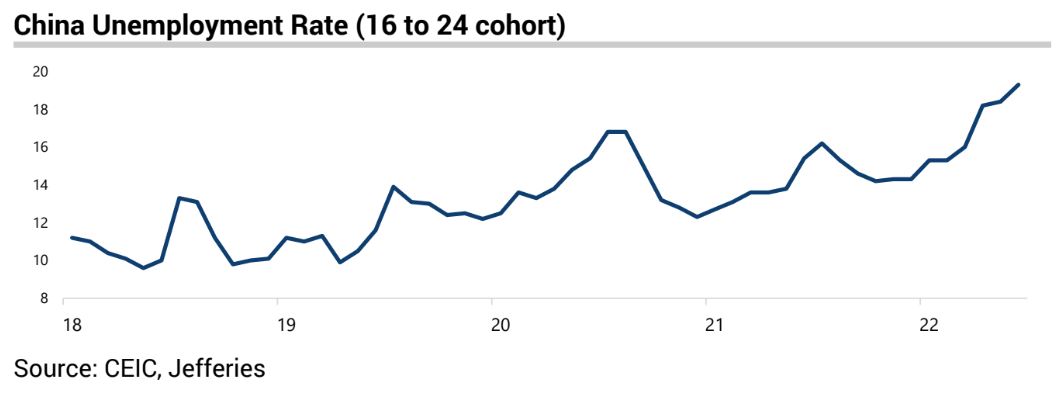

And unemployment is fast becoming a big problem:

It’s not beyond China to throw the kitchen sink at another property stimulus. But it is unlikely to work as well again given how strident and repetitious has been the CCP’s stomping on realty speculation, for both punters and developers.

Advertisement

And why would it do it anyway? It will only make the ultimate problem much worse, as this correction is amply demonstrating, especially since the underlying demographic drivers can no longer support it.

More likely is that China is ready to pay the piper for ending its giant property buildout. Future construction will be supported by more debt in LGFV but they, too, are out of profitable projects so even this is unlikely to be sustained.

My own view is that the only way out is a much lower CNY as interest rates just keep on falling.

Advertisement

The implications of this for China-centric commodities are all bad:

Property is 40% of Chinese demand and 20% of global so if sales remain at half mast then demand is down 10% globally. Especially so for coking coal, iron ore and copper.

A falling CNY is almost as bad as it makes locally produced commodities more competitive.

A falling CNY always means a stronger DXY and given commodities are priced in US dollars, that will drain the financial bid for commodities as well.

Wall Street’s post-Ukraine commodity mania – captured best by a foaming at the mouth Goldman and Zoltan Poszar’s argument for a commodities-based Bretton Woods III – may actually mark the top in a forthcoming twenty-year bear market in dirt.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.