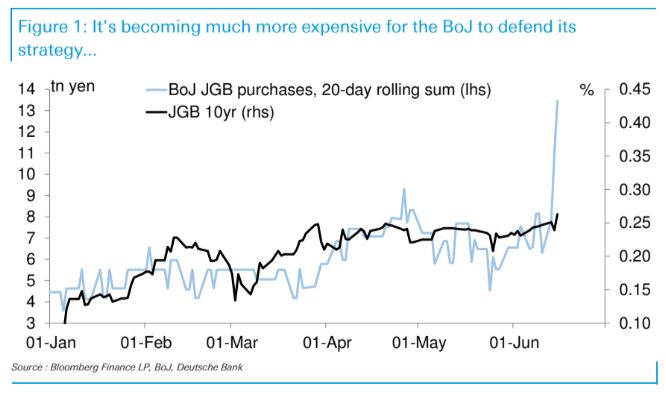

The topic of today’s CoTD is the BoJ who meet on Friday. Nothing much is expected from them but let’s look at the wider context. As of last night, so far in 2022, 10yr yields in the US, Germany, France, the UK and Italy were up +196bps,+193bps, +219bps, +162bps and +300bps, respectively. Meanwhile 10yr JGBs are up just +19bps, and having traded in a very narrow 5bps range since the middle of March just below the BoJ’s 0.25% target. This target is becoming more expensive to defend as the global yield sell-off has escalated.I ndeed the Yen has fallen nearly -20% since March as they are becoming the last man standing on QE. However, there is absolutely no sign that the BoJ is about to change course but as a tail risk, it’s the first thing I look at every morning when I wake up to write the Early Morning Reid. Although the house view is that the BoJ won’t change tact until H2 2023, at various points this year there were no signs the ECB or the Fed were prepared to be anywhere near as aggressive as they now look set to be. Both have aggressively backtracked on their own forward guidance. This leaves the BoJ as the outlier and having to spend a phenomenal amount defending their target. So if you’re looking for something to reset global yields even higher, or a not too outlandish tail-risk event, then this is one to track over the next few months.

Actually, I think this is more likely to be the high for yields globally if it were to happen. The final poetic capitulation of the end of the Japanese “widowmaker” trade.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.