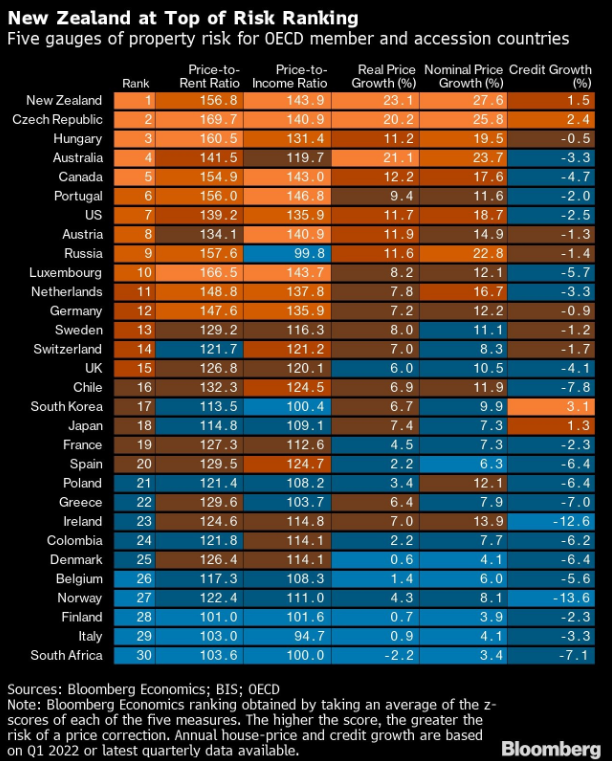

Bloomberg Economics has released its list of the world’s riskiest housing markets that are most vulnerable to a house price crash.

Not surprisingly, New Zealand has taken out first place after experiencing extreme price growth over the pandemic, which helped drive home valuations to absurd levels based on price-to-rent and price-to-income ratios:

New Zealand for the win!

The potential impacts of a severe house price correction are spelled out clearly by Bloomberg:

Falling home prices would erode household wealth, dent consumer confidence and potentially curb future development. Animal spirits are typically tamed when people are faced with higher repayment costs on an asset that’s losing value. And property construction and sales are huge multipliers of economic activity…

If 2021 was the year New Zealand’s house-price growth reached dizzying heights, with an annual increase of close to 30 per cent, 2022 is shaping up to be the year the music stops — and the abrupt change has left people scrambling…

Economists expect New Zealand house prices will fall about 10 per cent this year and may eventually drop as much as 20 per cent from their late 2021 peak…

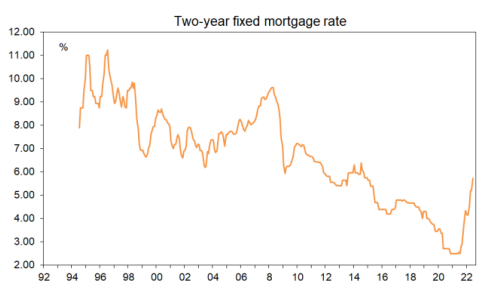

“There are going to be house buyers who have just entered the market in the last year or so who started off with a mortgage rate of 2.5 per cent and all of a sudden they are rolling off on to a mortgage rate closer to 6 per cent,” said Jarrod Kerr, chief economist at Kiwibank in Auckland. “There is going to be some pain for sure.”

New Zealand’s median dwelling price has already plunged 9.2% from the November 2021 peak with the stock of unsold homes also ballooning.

The bulk of Kiwi borrowers are also on fixed rate mortgages of two years or less, which means that Kiwis that originated mortgages at rock-bottom pandemic rates have yet to impacted by the Reserve Bank’s aggressive monetary tightening.

This situation will change at the end of this year when these cheap fixed rate mortgage terms begin to expire and borrowers are required to refinance to significantly higher (double) mortgage rates. That is when the impact of the Reserve Banks monetary tightening will truly be felt across the economy via a sharp contraction in consumer spending.