Finally, some reality set in for the ferrous complex on June 20, 2022:

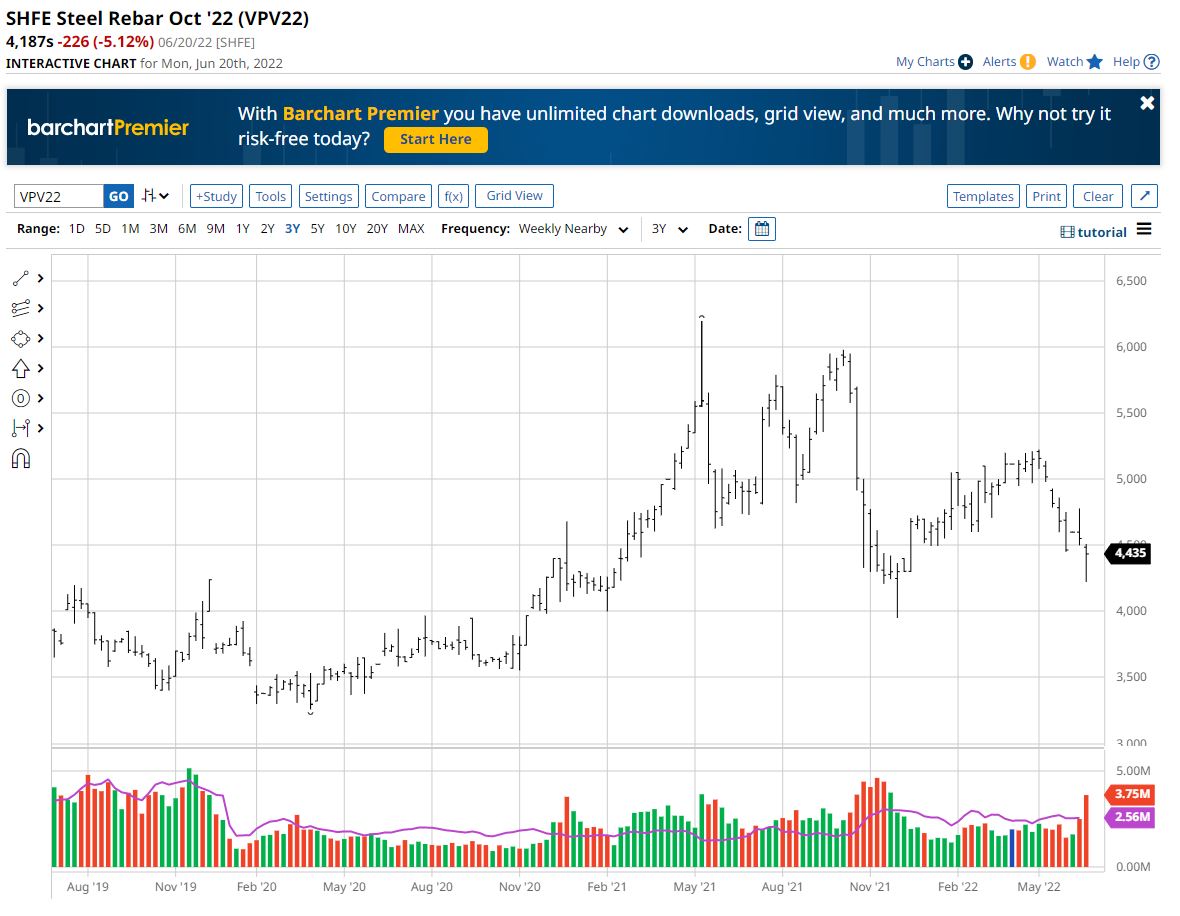

The rout is being led lower by steel prices in China:

Advertisement

I don’t think that it is unreasonable to expect a return to the 3500 range for rebar. To wit:

Finally, some reality set in for the ferrous complex on June 20, 2022:

The rout is being led lower by steel prices in China:

I don’t think that it is unreasonable to expect a return to the 3500 range for rebar. To wit:

The full text of this article is available to MacroBusiness subscribers