Capital Economics’ senior economic adviser, Vicky Redwood, has tipped house prices to fall across several developed nations.

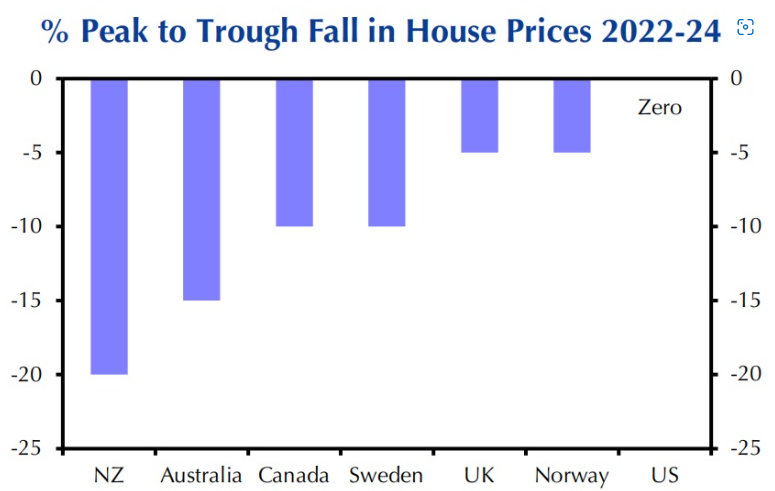

House prices in New Zealand are forecast to fall by 20% peak-to-trough, whereas is Australia prices are tipped to fall by 15%. 10% peak-to-trough falls are predicted for Canada and Sweden, whereas UK and Norway house prices are tipped to fall by 5%:

“House price inflation in these countries is already easing. Australia, New Zealand and Canada have seen outright monthly falls in prices. There are also signs of a slowdown in housing demand and sales.

“We have now pencilled in house price falls over the next year or two, ranging between 5% and 20%, in New Zealand, Australia, Canada, Sweden, the UK and Norway.

“And the risks are skewed towards even bigger falls.

“After all, even these drops will reverse only part of the rise seen over the past couple of years. And interest rates may rise further than we expect – in which case, price falls would spread to other countries including the US. (We currently expect house price inflation there to slow to zero.)”

Capital Economics notes that the fall in house prices will drag on economic activity. It also “expects rates in Australia and New Zealand to fall by end-2023” – something MB has also suggested will happen.

Advertisement

While New Zealand’s monetary tightening started six months earlier than Australia’s, unlike Australia the majority of mortgages in New Zealand are fixed rate not floating. This means that there should be a faster transmission between rising interest rates, mortgage repayments and house prices in Australia than most other economies (including New Zealand).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.