After 18 months of FOMO, Aussie home buyer sentiment has well and truly shifted to Fear of Overpaying (FOOP).

New data from Domain shows that the number of property searches fell significantly in April compared to the same time last year in every state except the Northern Territory:

Australian property search volumes have fallen sharply.

Searches fell most heavily in NSW and Victoria, which are now leading the nation’s property downturn.

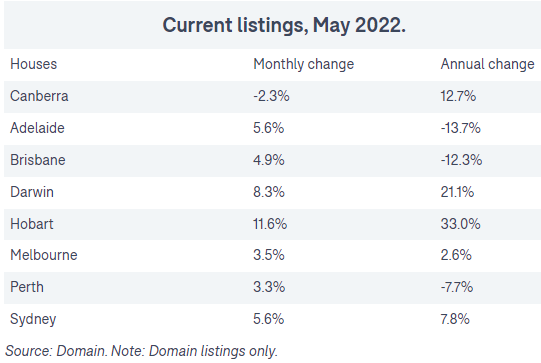

Meanwhile, the reduced buyer interest has driven property listings up across almost every market:

Property listings are rising across Australia.

Commenting on the results, Domain chief of research and economics Dr Nicola Powell said that “homes are coming onto the market quicker than they are purchased”, and “they’re taking longer to sell”.

This above Domain data does not fully capture the Reserve Bank of Australia’s latest rate hikes, which have only just begun.

Expect to see more buyers remain on the sidelines as they wait for house prices to bottom. And given the extreme interest rate forecasts, the bottom could be a long way down.