Christopher Joye, portfolio manager at Coolabah Capital Investments, has warned that Australian housing values could plummet more than 30% if the Reserve Bank of Australia (RBA) lifts interest rates in line with the market’s expectations:

Aussie house prices could fall by more than 30 per cent if the Reserve Bank of Australia’s fulfils uber-aggressive market expectations for an increase in its cash rate from the post-pandemic nadir of 0.10 per cent all the way to 4.25 per cent. This would translate into an increase in the cheapest discounted variable mortgage rate from around 2.25 per cent to 6.50 per cent, or possibly higher given bank credit spreads (or funding costs) have widened sharply…

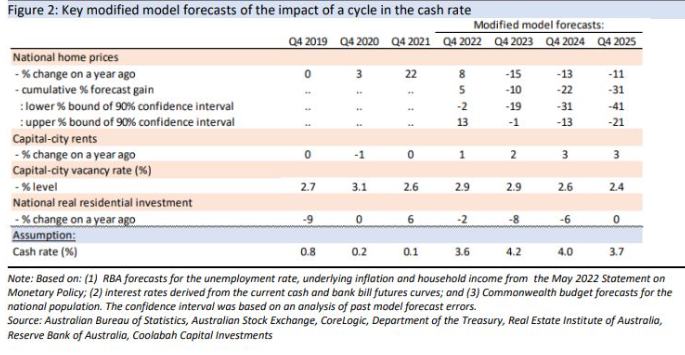

Coolabah Capital Investments has analysed the impact of temporary changes in interest rates on the housing market, focusing on current market pricing of a broad peak in the cash rate of 4.25% over 2023 followed by rate cuts in 2024 and 2025. This analysis suggests that this cycle in interest rates still has a significant effect in the short term, pointing to a large correction of about 30% in national home prices over the next four years (or circa 40% from late 2022 onwards). There is significant uncertainty around the model’s forecasts, but the results suggest a large short-term correction is in store as the RBA takes back its emergency policy stimulus…

Given the dramatic rise in the interest rate sensitivity and debt levels of households, there is a case for the central bank to carefully evaluate shifts in behaviour in response to tighter policy.

At this juncture, the RBA does not seem concerned about the consequences of policy overreach, and—based on Governor Phil Lowe’s public remarks—it wants to quickly lift its cash rate back to 2.5 per cent. It presumably believes it can do this without materially adversely impacting the economy. This would mean raising the cheapest discounted variable mortgage rates up to around 5 per cent.

This column’s view is that a record, 15-25 per cent decline in Aussie house prices, coupled with rapidly shrinking superannuation balances, will persuade the RBA that there is merit in pausing its hiking cycle to assess the impact of these changes on household behaviour.

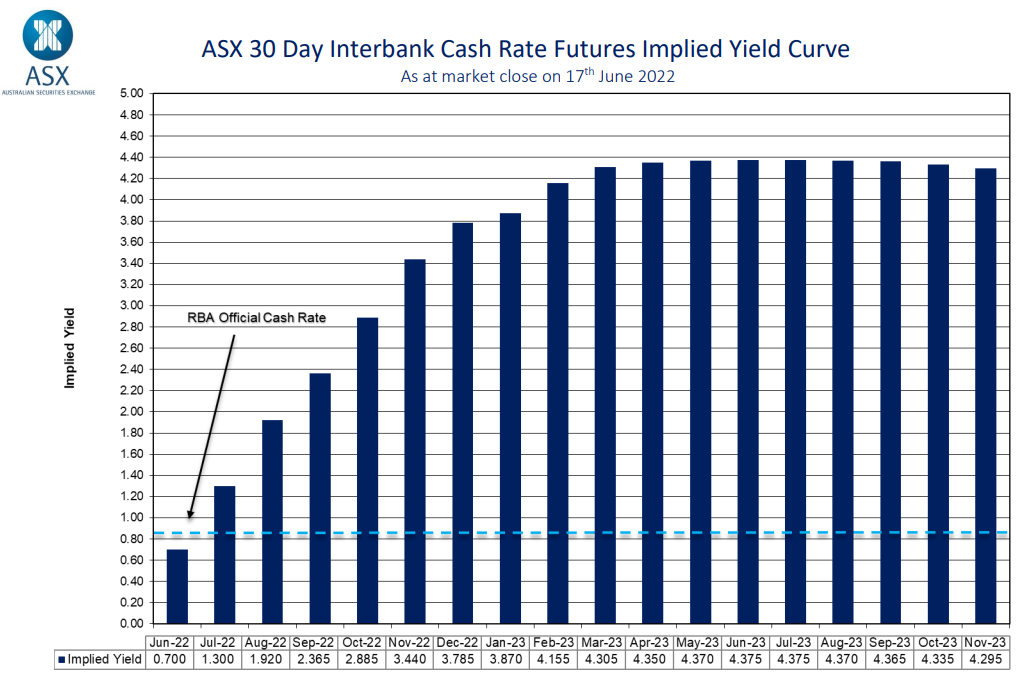

The latest futures market forecast for Australian interest rates is presented below:

Fastest rate rises in Australia’s history.

Advertisement

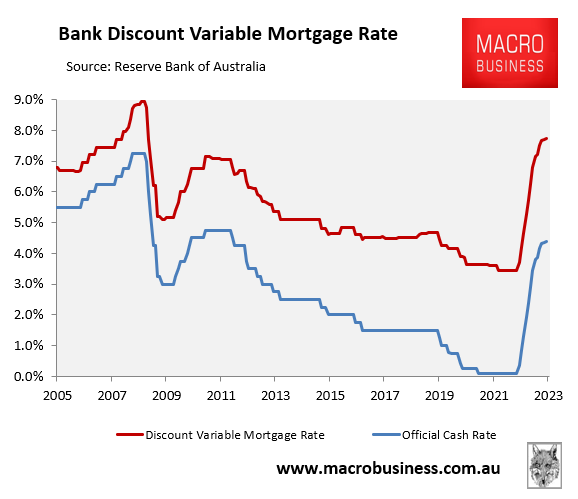

As you can see, the market is tipping a 3.8% official cash rate (OCR) by December and 4.4% by May 2023. If true, this would push the average discount variable mortgage rate to 7.7% – more than double its pandemic low:

Fancy a 7.7% mortgage rate?

In its latest Financial Stability Review, the RBA estimated “that a 200-basis-point increase in interest rates from current levels would lower real housing prices by around 15 per cent over a two-year period”. This was based on a similar model to that used by Coolabah Capital Investments.

Advertisement

Thus, the futures market’s bullish 4.4 per cent OCR would ‘crash’ Australia’s housing market, with real house prices falling by more than 30% in real terms and by more than 35% in nominal terms, under the RBA’s own modelling.

More than $3 trillion of value would literally be wiped from Australia’s $10 trillion housing market.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.