The last deflationist standing is not going to fall unless something changes. Pantheon has the note.

—

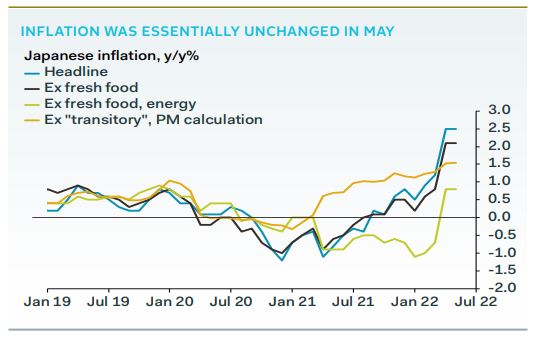

Japanese CPI inflation was unchanged in May, at 2.5% year-over-year, the second month above the BoJ’s 2% target. We now expect inflation to remain above target for the rest of the year, thanks to the ongoing weakness in the yen. But we still don’t expect a change from the BoJ, who have been consistent in their messaging. Inflation driven by cost shocks, and unaccompanied by wage growth, is not regarded as sustainable, and does not warrant tighter policy. Policy settings should remain on hold into 2023.