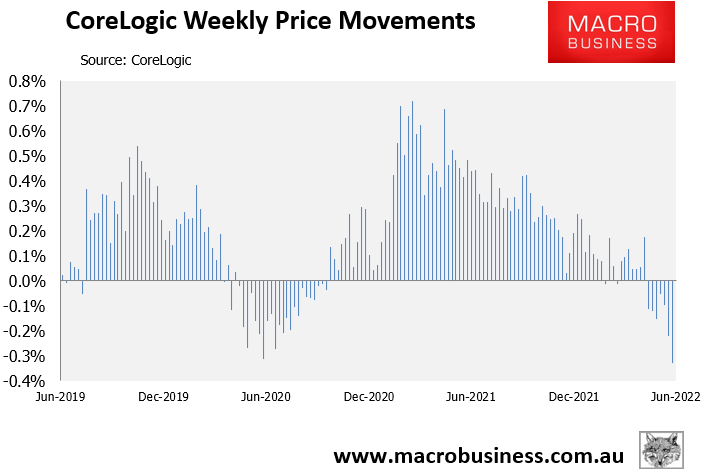

CoreLogic’s daily dwelling values index tanked in the week ending 23 June, plunging by 0.33% across the five major capitals – the biggest weekly decline since January 2019:

Biggest weekly decline in house prices since January 2019.

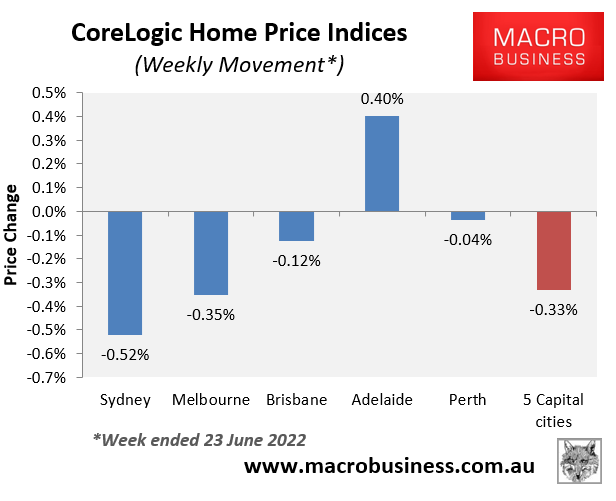

Every major capital city market experienced price falls, with the exception of Adelaide:

Adelaide the last housing market standing.

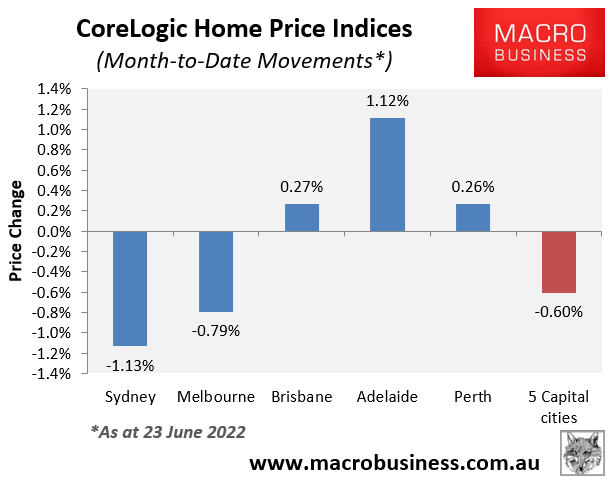

Sydney and Melbourne house prices are tanking, down 1.13% and 0.79% respectively so far in June, which has dragged values at the 5-city level down 0.60%

Big corrections underway for Sydney and Melbourne.

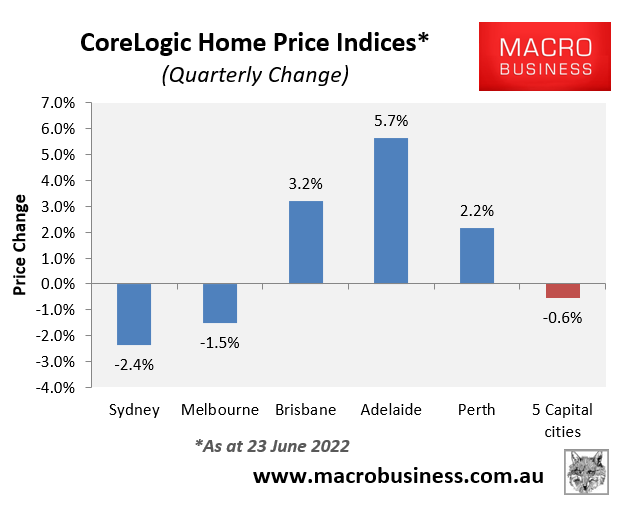

Quarterly values also continue to plummet, with Sydney down 2.4% and Melbourne’s down 1.5%. These falls have offset increases across the other markets, driving values down 0.6% at the 5-city level:

Sydney and Melbourne lead the housing correction.

Sydney dwelling values have fallen 2.7% since peaking in mid-February, whereas Melbourne’s are down 1.7% from its peak.

The great Australian housing correction has clearly begun, led by Sydney and Melbourne. How deep it goes will depend on how aggressively the Reserve Bank hikes interest rates.

If the futures market is correct, and mortgage rates more than double to 7.5% by mid-2023, then both cities are staring at the prospect of their biggest price crashes in 100 years.