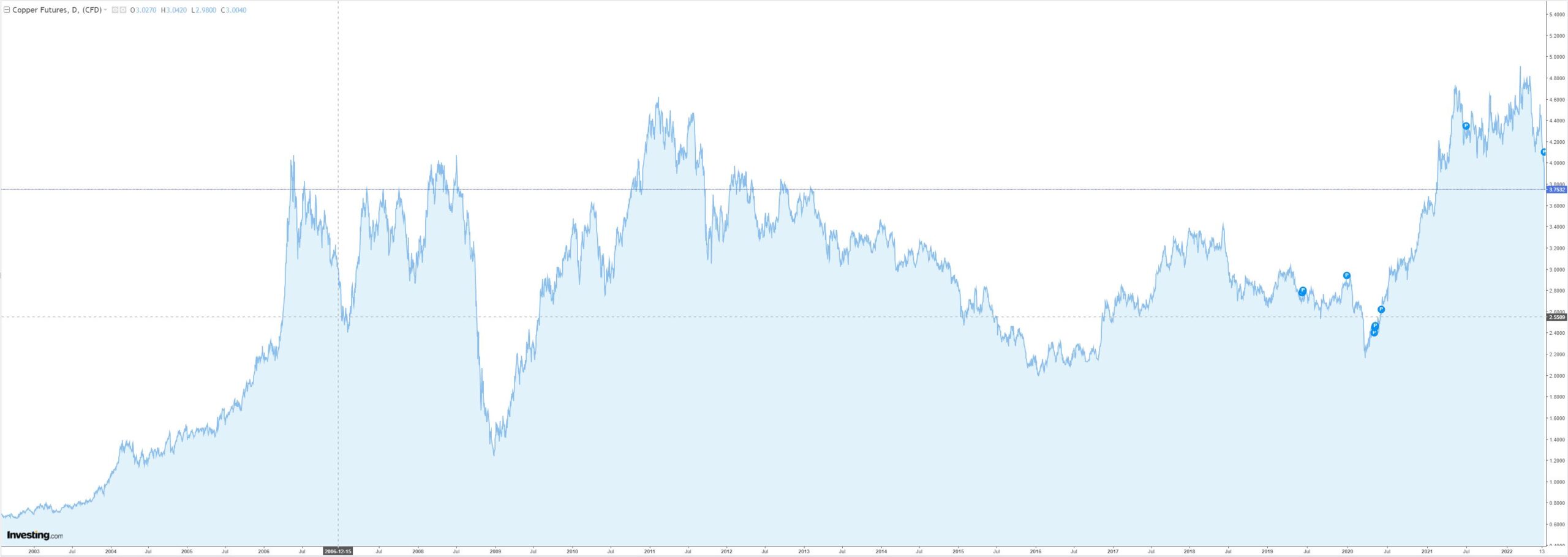

The copper chart is not pretty. After being driven to all-time highs by Wall Street spruikers it is now crashing:

The long-term story for copper is no shortages at all. The great EV and power transformations can largely be absorbed by recycling.

There is also plenty of supply coming on stream in the next few years. Societe General has it.