The ferrous complex was mixed on Friday 30th of April, 2022:

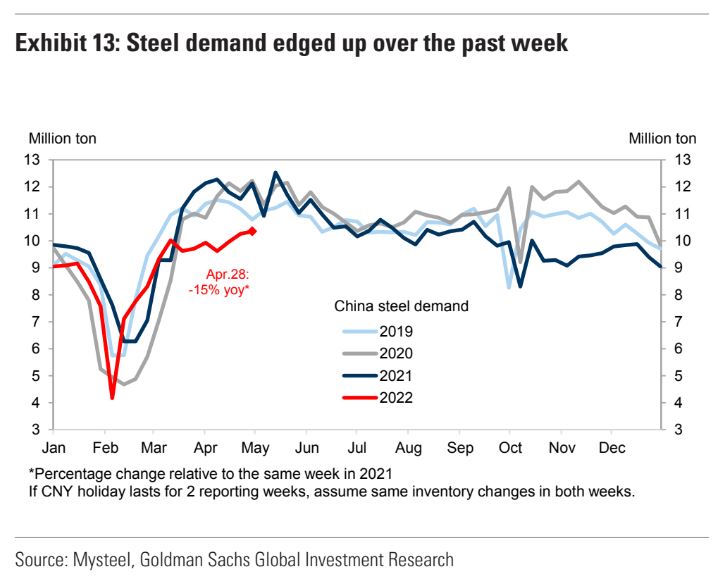

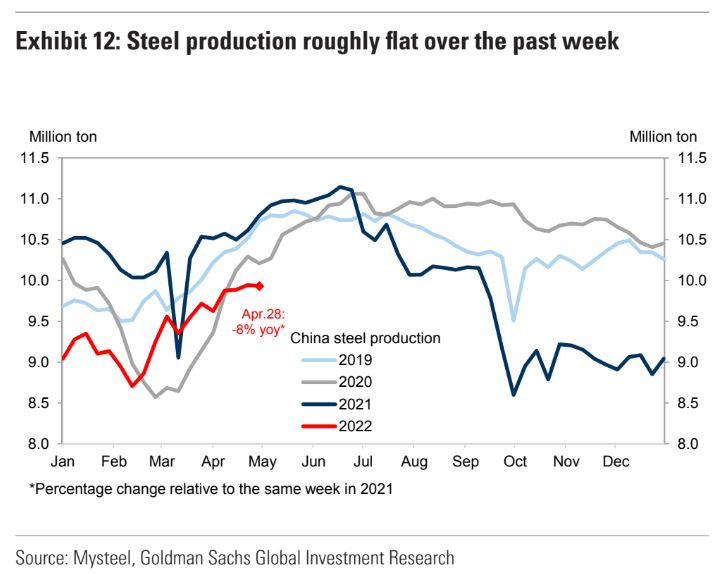

But the data remains terrible. Mysteel surveys show demand and output way down on last year:

Production down 8% is the equivalent of 140mt less iron ore needed. The latest recycling shutdowns is roughly 40-50mt so there is an abundance of iron ore supply versus last year.

Advertisement

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.