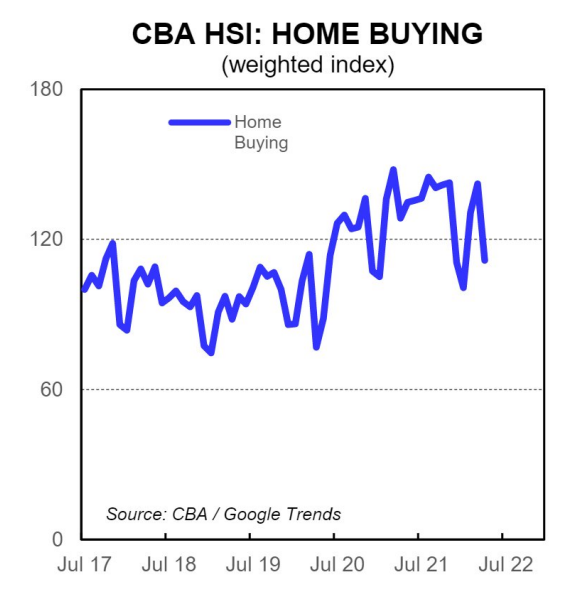

New data from the CBA shows that home buying intentions dived 21.5% in April to be 13.1% lower year-on-year, with accelerating declines expected now that interest rates are rising:

The home buying spending intentions index fell 21.5% in April… April is normally a seasonally weak month, but this month was weaker than average.

Home loan applications were weaker on the month in April. Google searches related to housing were also generally weaker across the different categories.

Relative to April 2021, Home buying intentions are lower at -13.1%/year and down 25% since the peak in March 2021.

Dwelling prices have continued to moderate and we would expect this to accelerate now the RBA has commenced its hiking cycle.

AMP chief economist, Shane Oliver, also believes that home buying intentions will crater as mortgage rates lift:

“I think the drop in home buyer demand has further to go as interest rates are just starting to rise at a time when affordability is already worsening”.

“The price falls will likely intensify as the pool of buyers dwindles as it gets harder for people to enter the market.”

Advertisement

Meanwhile, the PropTrack Housing Market Indicators Report was released yesterday and found that sales volumes in April were 15% lower year-on-year, driven by heavy falls across Sydney and Melbourne.

Enquiry volumes for all buyer types were also 22.4% lower compared to April 2021 and have almost halved from peak levels recorded last year.

Commenting on the results, PropTrack senior economist Eleanor Creagh noted that “price growth has slowed and stalled across the country particularly in Melbourne and Sydney”. Moreover, ” with interest rate rises, we are going to see borrowing capacity reduced and that will weigh on the housing market in the months ahead, with rising fixed mortgage rates and affordability constraints”.

Advertisement

Finally, Westpac’s “time to buy a dwelling” index, which was already 40% below its most recent peak in November 2020, fell a further 1.5% in May to it lowest level since April 2008.

With mortgage rates on the rise and house prices now expected to fall, home buyer demand should collapse. How far depends on whether the RBA takes a measured approach to rate rises, or hikes aggressively.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.