From Westpac’s Bill Evans:

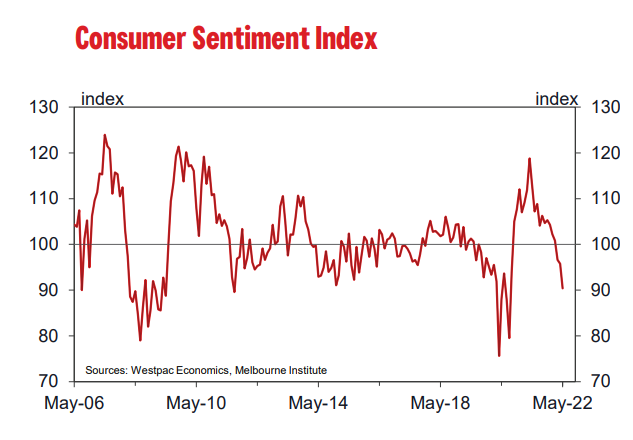

The Westpac-Melbourne Institute Index of Consumer Sentiment fell by 5.6% to 90.4 in May from 95.8 in April.

The Index is now at its lowest level since August 2020 when households were unnerved by the ‘second wave’ lockdown in Victoria. The weakness in this survey is not related to another pandemic shock but to the combination of rising cost of living pressures and the prospect of rising interest rates.

Excluding the shocks to confidence associated with the pandemic, this fall of 5.6% is the largest since a 6.9% fall in June 2015, when a steep fall in global share markets was triggered by concerns about the stability of the European financial system and a slowdown in China. That came shortly after May 2014 when a

poorly received Federal Budget smashed confidence by 6.8%.

The May print is 8.4% below the average seen in 2019, when consumer spending was generally described as lacklustre, essentially holding flat over the year. Consumer spending is much more buoyant over 2022 to date, as households respond to the reopening of the economy. This lift reflects a normalisation from the ‘low spending/high saving’ pattern seen during the COVID restrictions and is being supported by a large reserve of excess savings accumulated over the past two years.

The survey of 1200 respondents was conducted over the week May 1 to May 5, which covered the announcement by the Reserve Bank of the 0.25% increase in the cash rate from 0.1% to 0.35%.

Two stunning developments are clearly unnerving consumers.

Firstly, on April 27, headline inflation was reported to have lifted above 5% for the first time since 2007. Then, on May 2, the Reserve Bank raised the cash rate for the first time since 2010.

While headline inflation pressures may ease from this point, consumers are aware that the Reserve Bank plans to continue increasing the cash rate for some time. Westpac expects multiple increases through the remainder of the year with the cash rate peaking at 2.25% in May 2023.

Consumers also look to be bracing for a steep rise in interest rates. Our May survey found 77% of respondents expect mortgage interest rates to rise over the next 12 months, up from 70% last month.

But it is even more significant that 52% expect rates to rise by more than 1%, up from just 34% only one month ago.

Amongst workers, outright confidence levels are weakest for those operating in hospitality; retail; construction; education; health; the arts; and professional services while those in mining; IT; telecommunications and media; wholesale trade; and government are all registering solid positive reads.

The component detail shows a sharp rise in concern about the near-term outlook for family finances. The ‘family finances, next 12 months’ sub-index tumbled by 11.2% to 93.3, in contrast to the ‘family finances compared to a year ago’ sub-index which held steady, albeit at a relatively weak 79.6.

The prospect of rising interest rates is clearly weighing on respondents despite the prospect of higher bank deposit rates.

Assessments of the economic outlook also deteriorated. The ‘economy, next 12 months’ sub-index was down 5.8% to 90.4 and the ‘economy, next 5 years’ sub-index fell by 4.1% to 96.2.

The surge in prices continues to bite hard on attitudes towards spending, the ‘time to buy a major household item’ sub-index down by 5.7% to 92.6. To put this into perspective, this is near the low seen during Victoria’s ‘second wave’ outbreak in 2020, when health concerns were discouraging shoppers, and, prior to the pandemic, the lowest read since the GFC. The current level of this sub-index is 27% below its long run average of 126.3.

The sharp fall in confidence even spread to what have otherwise been very upbeat labour market expectations. The Westpac-Melbourne Institute Unemployment Expectations Index increased 10.5% to 109.6 (recall that a rise means more respondents expect a rise in the unemployment rate – a worsening outlook).

The index is still well below the long-term average of around 130 and remains a positive assessment of the labour market.

Not surprisingly, the prospect of rising interest rates is weighing heavily on confidence in the housing market.

The ‘’time to buy a dwelling’ index, which was already 40% below its most recent peak in November 2020, fell a further 1.5% in May. The Index, which is principally affected by affordability, is now at its lowest level since April 2008 when, due to rising inflation, the RBA felt obliged to raise rates in both February

and March despite the looming Global Financial Crisis.

The outlook for house prices is also starting to deteriorate more rapidly. The Westpac Melbourne Institute Index of House Price Expectations fell by 9.4% to 121.4. Most respondents still expect house prices to rise over the next year – indicated by an index read above 100. The latest read compares to the consistent

sub-100 prints seen in 2018 and 2019 when house prices were correcting by 12–15% in the Sydney and Melbourne markets.

While all major state indexes saw declines, the largest was in Queensland (–22%) which was coming off a very positive 154.8 in April. Falls in other states were more modest – Victoria (–6.2%); NSW (–4.5%) and WA (–5.4%). The indexes in Victoria (112.7) and NSW (116.9) are now well below the national average (121.41).

The Reserve Bank Board next meets on June 7. Having now begun its tightening cycle the Board is almost certain to follow up the move in May with a further move in June. The specific task of reducing demand-related inflation pressures and containing inflationary expectations is now at hand and the disturbing signal from today’s sentiment report should not dissuade the Board from that objective.

Today’s report highlights the sensitivity of Australian households to higher rates and rising inflation. Given the recent unexpectedly robust surge in inflation, arguably, the Board would have acted earlier had it expected such a development in the inflation picture (the annual increase in the Bank’s preferred measure of underlying inflation printed 3.7% for the March quarter, well above the 3% we calculate the Board would have been expecting).

Some catch up is the best approach for June.

We would prefer to see a policy lift of 40bps rather than the 25bps that the Governor recently intimated in his Press Conference when he referred to ‘business as usual’ for monetary policy. Such a move would swiftly remove the 65bps of rate cuts which were implemented during 2020 at the height of the

COVID emergency.

The Bank has recently lifted its forecast for underlying inflation in 2022 from 2¾% to 4¾% and is now assuming the daunting task of lowering that rate to 3% by mid-2024.

That requires more than a ‘business as usual’ approach.

The point at which interest rates become a damaging drag on the economy is unknown but it is prudent to balance the need for policy to catch up with the surety that rates are currently well below that inflection point. Leaving any catch-up moves to later in the cycle risks over-shooting that point.

This appears to be the approach being signalled by the US Federal Reserve for the early stages of its own tightening cycle, despite significant weakness in US measures of consumer sentiment.

The need to avoid an over-shoot later in the cycle is why, despite this disturbing tumble in Consumer Sentiment, we believe the prudent approach in June would be to lift rates by 40bps rather than the 25 bps that is currently favoured by most analysts.