The ferrous complex was mixed on May 26, 2022:

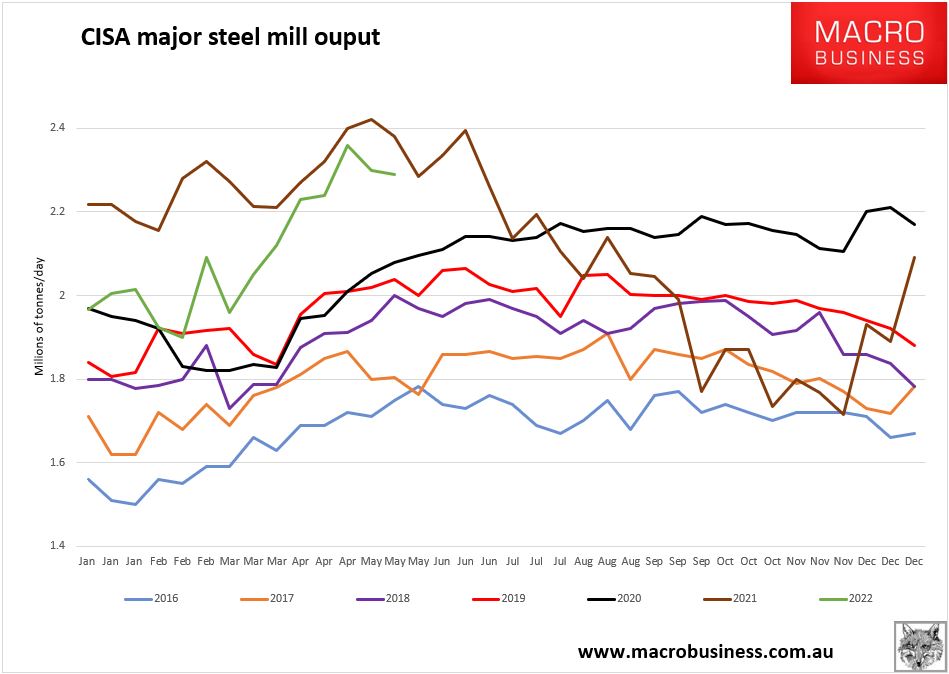

Here’s the latest CISA data. Production is far too high still:

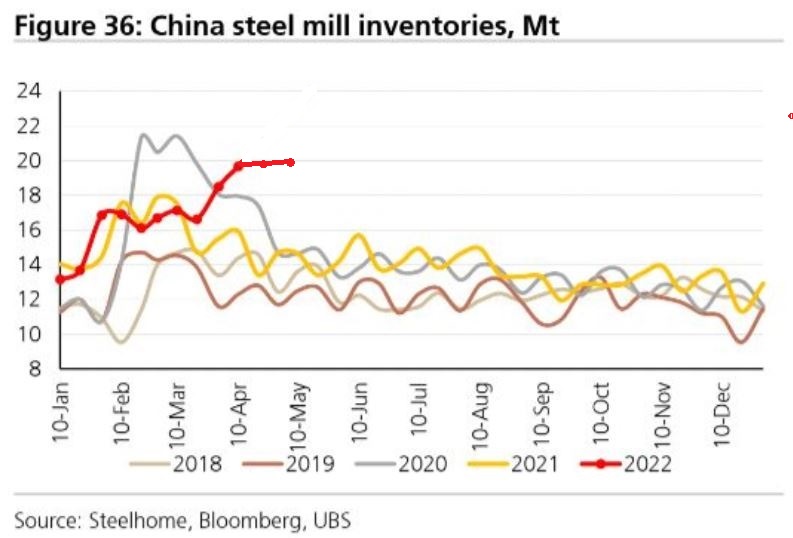

As are inventories (I’ve adapted a UBS chart):

Advertisement

The ferrous complex was mixed on May 26, 2022:

Here’s the latest CISA data. Production is far too high still:

As are inventories (I’ve adapted a UBS chart):

The full text of this article is available to MacroBusiness subscribers