The ferrous complex firm on May 16, 2022. Spot did not update:

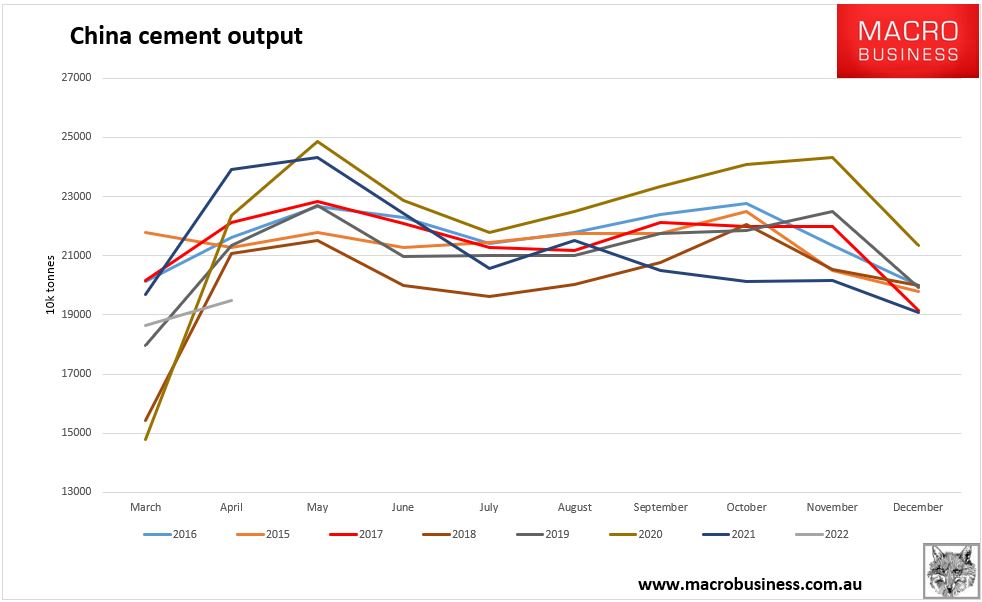

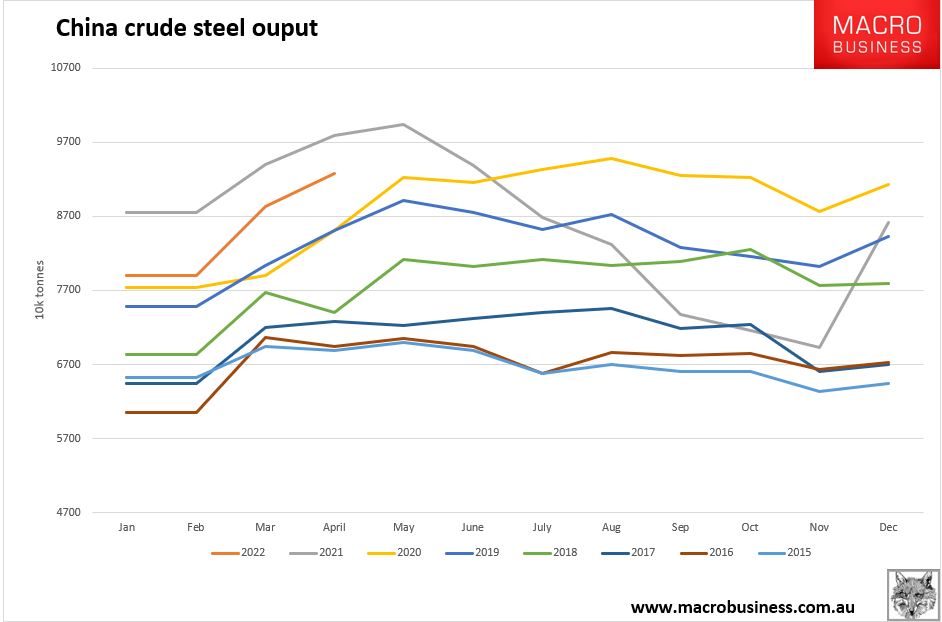

Yesterday’s China data has left me scratching my head. The numbers were disastrous across the board. With the exception of steel output which was only down 5%:

Advertisement

Versus cement down 19%: