Gareth Aird, head of Australian economics at CBA, has hosed predictions that interest rates could climb to 2.5% or above, for the simple reason that Australian households are far too indebted to endure such rate rises without causing a hard landing for the economy:

Money markets have priced a more aggressive tightening cycle than I believe is necessary to cool the economy and inflation across the medium term.

For context, financial markets expect the cash rate to be about 3 per cent by the end of the year, which implies further rate rises of 265 basis points in just seven months. In contrast, Commonwealth Bank economists expect the RBA to deliver a further 100 basis points of rate hikes this year (we expect 25 basis point hikes in June, July, August and November). It is easy to forget the cash rate was just 0.75 per cent on the eve of the pandemic…

The Australian household sector is one of the most indebted in the world. This means rate rises have a more powerful impact on our household sector than they do in almost any other jurisdiction. In addition, the policy transmission mechanism from the cash rate to home borrowers is much more direct in Australia than it is for many other central banks as the bulk of our debt is floating.

It is worth noting the percentage change in interest rates is incredibly large for each absolute increase in the cash rate given the starting point for rate rises was a record low cash rate. So the interest cost on debt will go up quickly in percentage terms. For example, a 200-basis-point cash rate rise from near-zero has a much bigger effect than, say, moving from 4 per cent to 6 per cent…

Home prices recently have begun to decline in Sydney and Melbourne. And there are already signs of consumer anxiety creeping into survey data. Rising consumer prices and higher mortgage rates will do that. Discretionary expenditure can suffer as a result, which in turn adversely affects employment…

Such a situation is unwanted and can be avoided… There is no need to engineer a hard landing in the economy to lower the rate of inflation across the medium term.

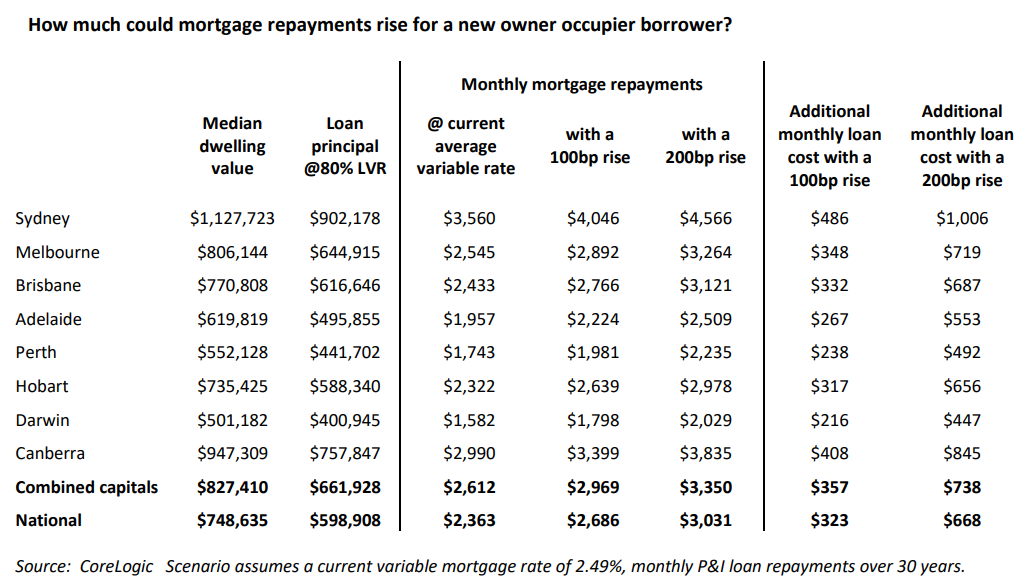

As shown this morning, if interest rates were to rise by 200 basis points, then monthly mortgage repayments would surge by 28%, representing a $668 a month increase in repayments across the median priced Australian home:

Such an steep rise in repayments would crush household finances, smash consumption, send house prices sharply lower, and risks driving the economy into an unnecessary recession.

For this reason, the CBA’s 1.25% projected peak in the RBA cash rate is far more realistic.