In Tuesday’s media conference following its decision to lift the cash rate by 0.25%, Reserve Bank governor Phil Lowe said it was “not unreasonable” to expect the cash rate to climb to 2.5%:

“How quickly we get there, and if we do get there, will be determined by how events unfold,” [Lowe] added, pointing out that 2.5% is the middle of the bank’s target band for inflation, meaning that when the cash rate gets there it will be zero in inflation-adjusted terms, rather than negative as it is at the moment.

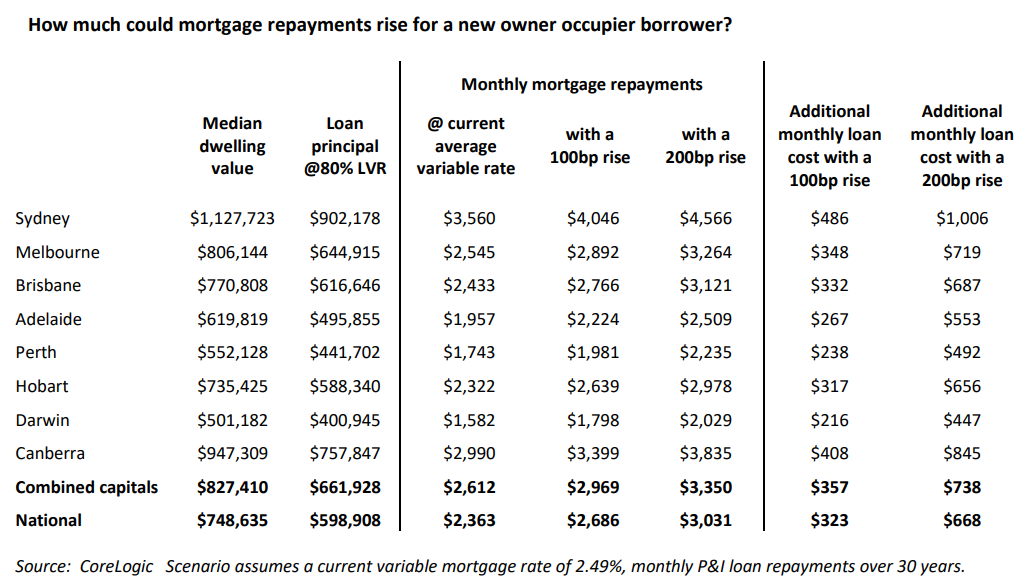

CoreLogic has provided a useful summary of what rate rises mean for the typical Australian mortgage borrower:

How much will your mortgage repayments rise?

If mortgage repayments were to rise by 100 basis points, then repayments on the median priced Australian home would surge by $323 a month, and by $357 across the combined capital cities. This would represent a 14% increase in mortgage repayments.

If rates were to rise by 200 basis points, then monthly repayments would surge by $668 a month nationally, and by $738 across the combined capitals, representing a 28% rise in mortgage repayments.

While not illustrated above, average mortgage repayments nationally would surge by $848 a month and by $937 across the combined capitals if rates were to rise by 250 basis points. This would represent a 36% increase in mortgage repayments.

As shown above, the dollar increase in mortgage repayments would be much higher in Sydney, owing to its status as Australia’s most expensive market with the most indebted households.

If Phil Lowe believes Australian households could absorb a 36% increase in mortgage repayments without crashing house prices and plunging the economy into recession, I have a bridge to sell him.