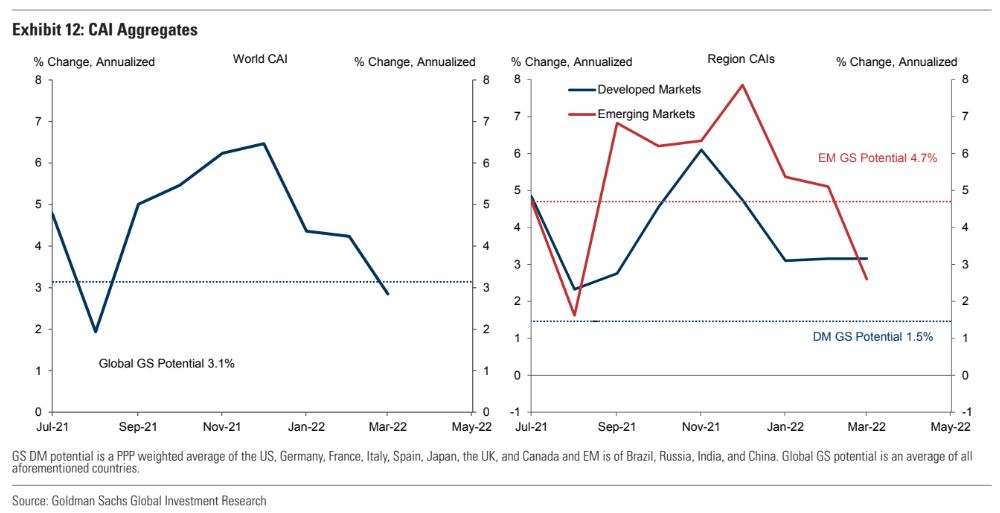

Goldman has some useful charts that capture the moment. Its current activity indexes are crashing

Especially for EMs which did their monetary tightening last year:

Advertisement

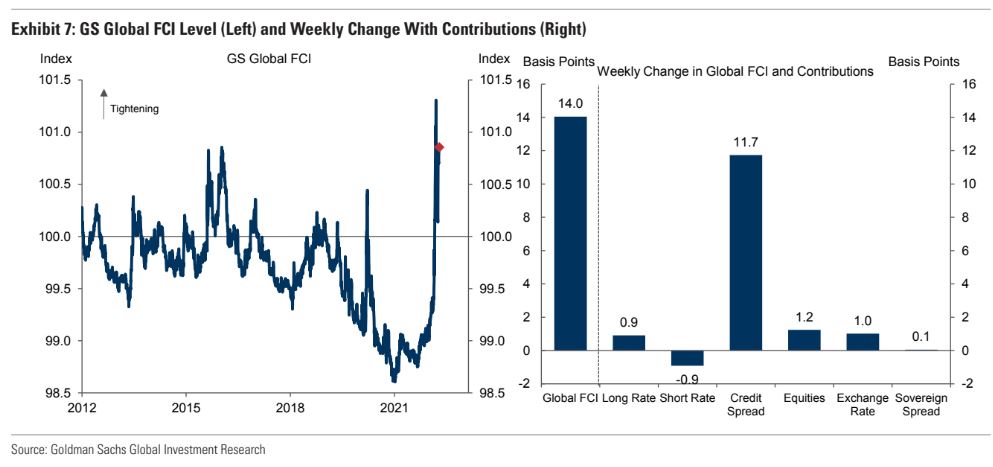

With the US about to tighten financial conditions like you would not believe: