The ferrous complex rallied modestly over Easter, 2022:

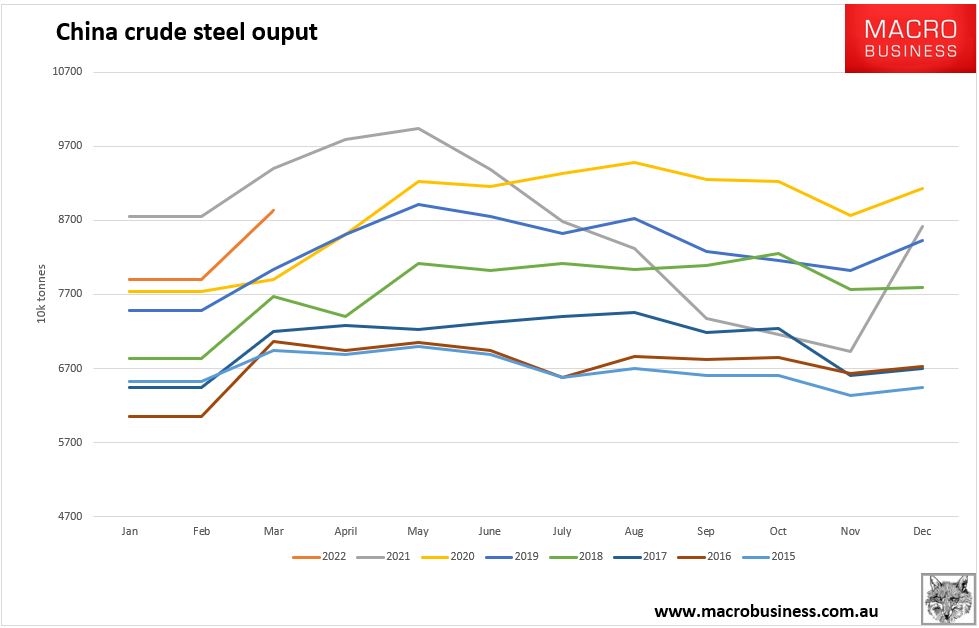

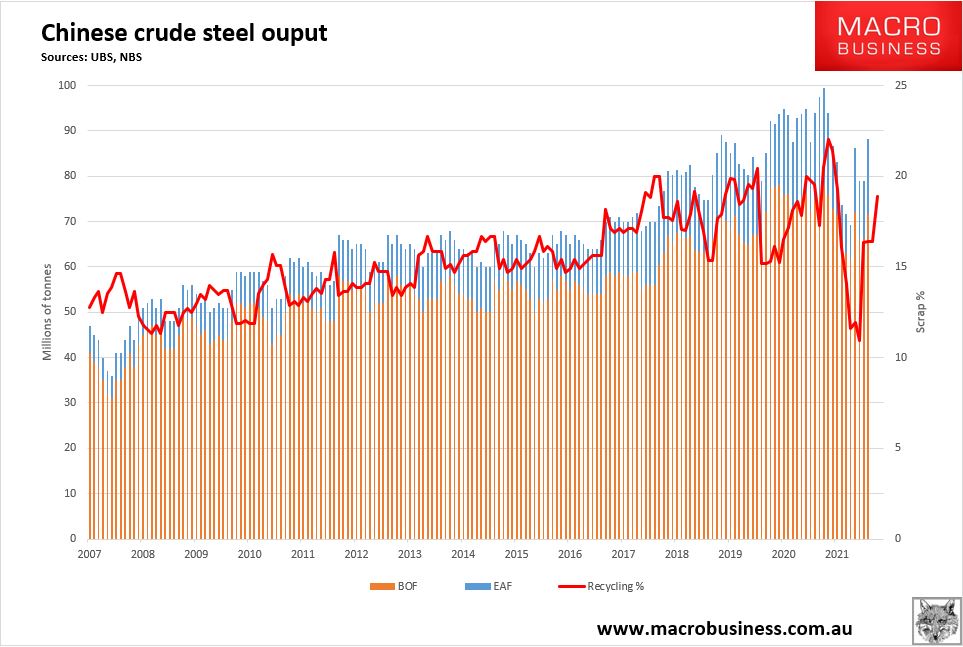

Yesterday’s China data dump revealed a few things. First, steel production has leaped:

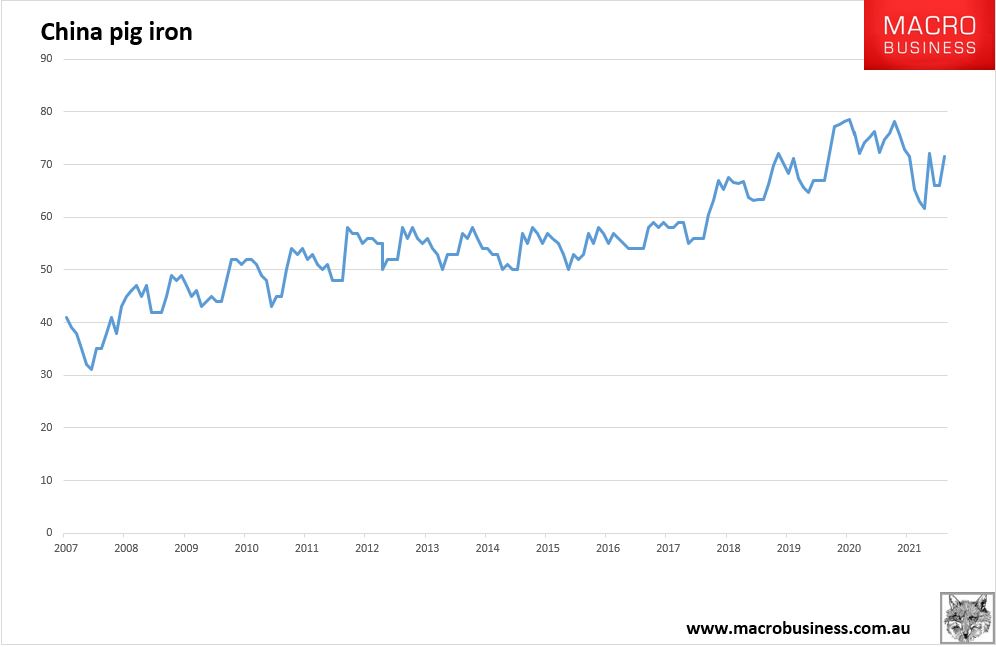

Pig iron output is running at about 2018/19 levels, down roughly 9% YoY or 30mt of iron ore through Q1:

Advertisement