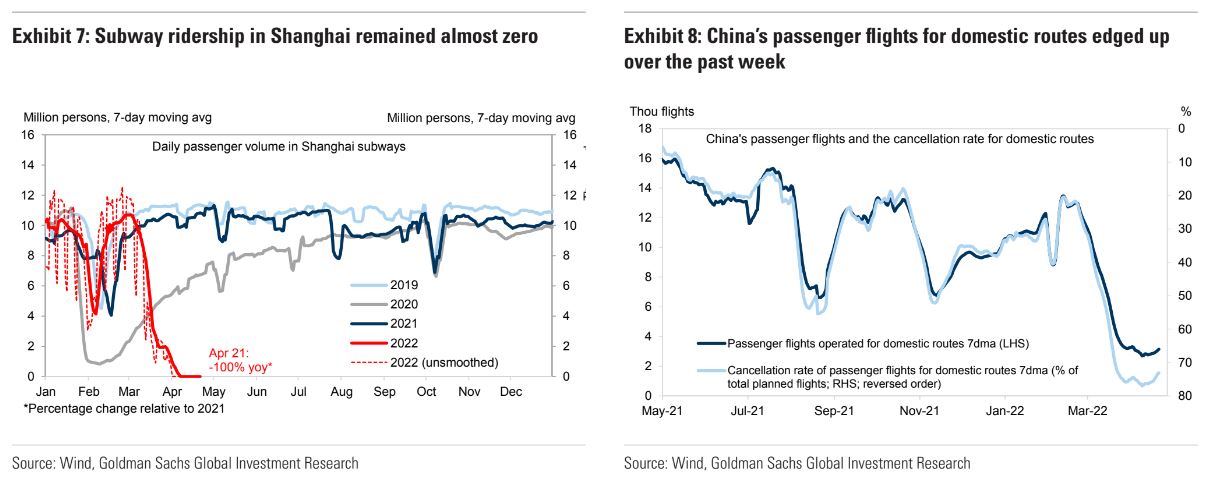

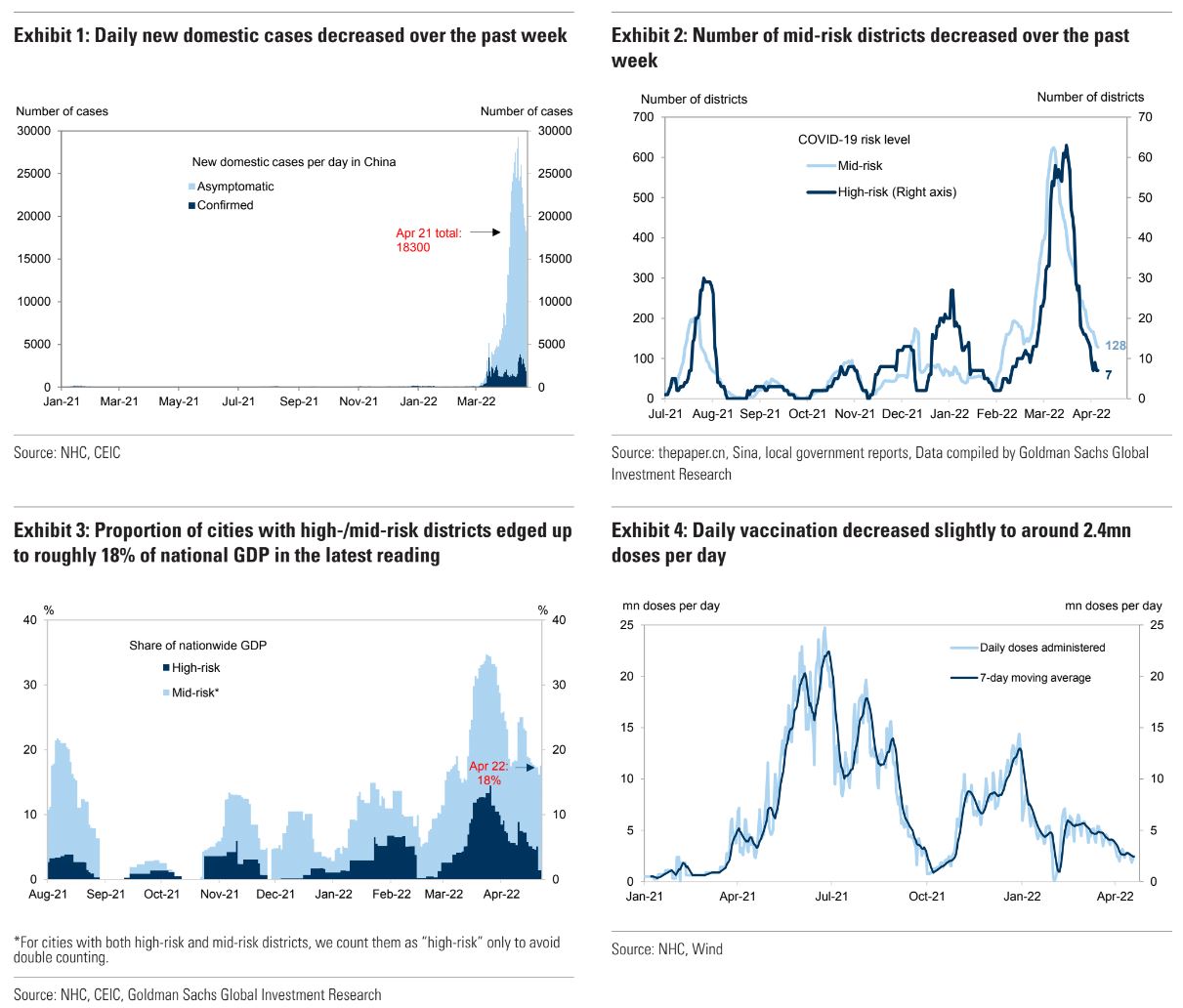

Chin is both winning and losing its battle with OMICRON. On one hand, case numbers are falling:

But they can’t stamp it out and Beijing is now being drawn into lockdowns.

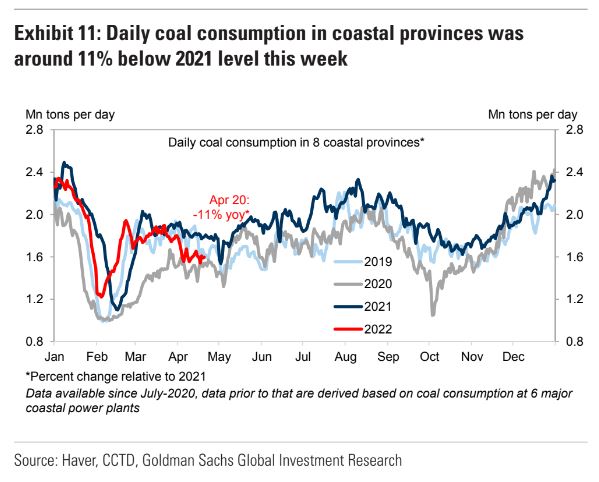

On the other hand, the economic spillovers are mounting:

Advertisement

Chin is both winning and losing its battle with OMICRON. On one hand, case numbers are falling:

But they can’t stamp it out and Beijing is now being drawn into lockdowns.

On the other hand, the economic spillovers are mounting:

The full text of this article is available to MacroBusiness subscribers