We all owe Vladimir Putin a drink. Ukrainian suffering aside, he has delivered the world an enormous favour in his bumbling invasion. How so?

First, this:

China’s top government officials have issued orders to prioritize energy and commodities supply security, sparked by concerns over disruptions stemming from the Ukraine-Russia war.

Government agencies, including the country’s top economic planning body — the National Development & Reform Commission — have been ordered to push state-owned buyers to scour markets for materials including oil and gas, iron ore, barley and corn to fill any potential gaps brought on by the conflict, according to people familiar with the matter. The officials made no mention of prices, the people said, indicating the cost of imports isn’t a focus right now.

Now imagine that this was transpiring against the backdrop of an invasion of Taiwan and nobody except Russia was prepared to supply China:

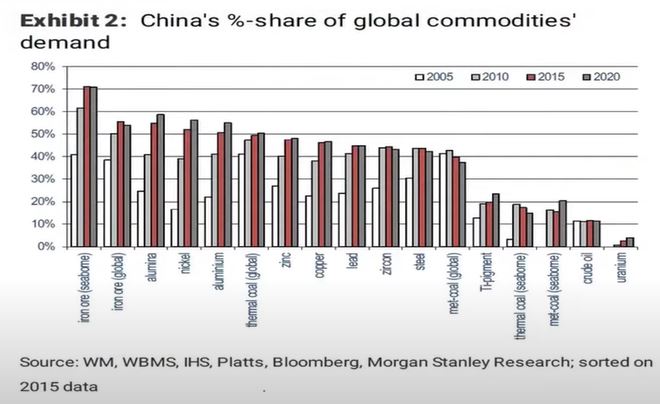

It’s a similar story in most soft commodities as well.

If China were to invade Taiwan and jeopardise the balance of power and peace in the Indo-Pacific then material commodity boycotts are a likely response from substantial portions of the international community. If we look at Russian oil exports today, even martial uncertainty is enough to destabilsie this trade, let alone official trade boycotts.

China’s ability to run its economy and feed its population is based upon the seamless supply chains of the global economy. If these are blocked in any meaningful sense then the Chinese economy will grind to an instant halt and its people begin to starve overnight.

China’s problems in managing a Taiwan invasion have gotten much more difficult post-Ukraine in another way as well. If the monetary sanctions applied to Russia were replicated for China, it would instantly lose access to a huge proportion of its foreign exchange reserves. It’s remarkably difficult to determine where these reserves are held these days. One-third is openly held in US Treasuries but the number is likely much higher thanks to China using third-party countries to hide the holdings. EUR holdings are also likely large.

If Europe were to join the US sanctioning the PBoC and freezing reserves, it would severely restrict the support it could provide to both currency and local banks. This would lead to credit rationing and acute domestic demand weakness.

Europe has always been the swing factor in this outcome. Would it support a strong US position on Taiwan given German exports to China? The Ukraine war has drawn Europe and the US back together strategically, in terms of energy trade and, perhaps most importantly, in the ideological and normative terms of forcefully protecting liberal democracy. In particular, Germany has undergone a regime change to a more hawkish strategic posture.

Third, I have underestimated the importance of the globalist mindset and technology. Russia has comprehensively lost the propaganda war in Ukraine. The same is the likely outcome in the event of a Chinese invasion of Taiwan.

There are caveats. Taiwan is not so clearly a sovereign state. Nor would it likely engender the same levels of sympathy given it is Asian not European (yes, a racist element). But I still think that China would lose the propaganda war and the result would be a considerable consumer boycott of Chinese-made goods worldwide.

In short, if the multilateral response to any invasion of Taiwan were managed correctly, every critical feature of Chinese economic engagement with the globe would all but collapse simultaneously. This would make the cost unbearable to the CCP as it risked a domestic revolution.

The reality of this threat of economic response must now be the thrust of all Indo-Pacific diplomacy. To ensure that such a coordinated boycott is locked and loaded and the CCP knows it.

Vladimir Putin may have just prevented WWIII.