Of all of the economic evils of the Morrison Government, this one is the worst. The new outlook for the AEMO for gas:

In the short term, new greenfield infrastructure solutions are unlikely to be operating in time for the earliest identified risk of gas shortfalls, in winter 2023. Brownfield solutions, such as duplication of the Winchelsea compressor on the South West Pipeline (SWP), may still be possible and improve supply available to south-eastern demand centres. Otherwise, the most likely lever to mitigate these risks is demand management at times of peak gas demand (in particular, reducing how much gas is used at these times to generate electricity).

In some scenarios, AEMO forecasts a risk of gas shortfalls in extreme weather conditions from winter 2023. The risk arises in south-eastern regions where gas flow is constrained by existing pipeline capacity limits

New South Wales, the Australian Capital Territory, Victoria and Tasmania. The 2021 GSOO identified this risk but expected Port Kembla Energy Terminal (PKET) to be operating by winter 2023.

Developers now advise that they remain committed to the terminal and associated pipeline infrastructure, but insufficient customer contracts have delayed the relocation and operation of the floating storage and regasification unit (FRSU), and project works will not be complete until late 2023. AEMO now classifies the project as anticipated supply for winter 2024.

South-eastern gas production will drop significantly from 2023, and shallow liquified natural gas (LNG) storages will need to be managed so they can help mitigate shortfall risks. Since last year, some producers now expect more short-term south-eastern supply, and more pipeline capacity to move gas to the south-east has been committed, but this does not remove the risk entirely. .

Unlike the NEM, the gas markets have limited mechanisms to deliver broad consumer demand response. Co-ordinating gas and electricity systems will be important to achieve demand response

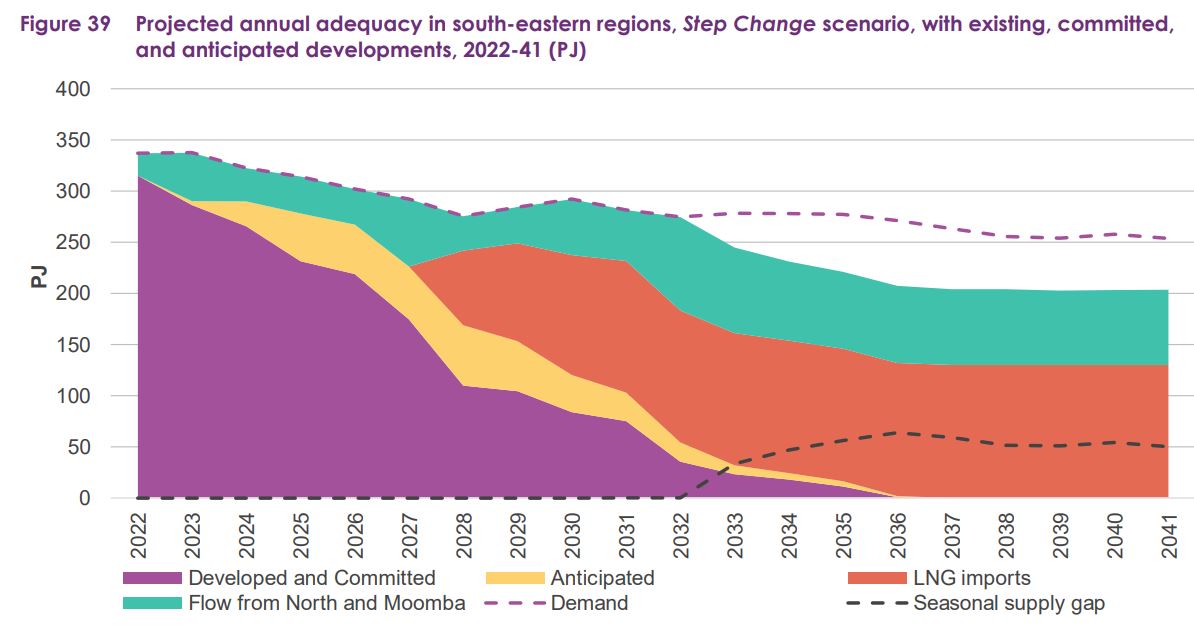

The above is the AEMO base case but it has worse scenarios. Even in this base case, the east coast is 50Pj short by the mid-2030s.

Even more terrifying, LNG imports cover 150Pj of demand within five years. The gas price in Asia today is $36Gj versus $14Gj here. It will come down but the Russian sanctions are likely permanent and some kind of geopolitical premium is as well. The local historic average is $2-3Gj.

Advertisement

There is, of course, plenty of cheap Aussie gas. It is coming out of the ground at a cash cost of $1Gj or less now that development costs are sunk.

But, the gas cartel is shipping it all to Asia via QLD:

1141Pj of gas last year.

757Pj of that went to China.

Advertisement

In short, the Morrison Government gas cartel is currently shipping gas to China to make weapons to threaten Australia and leaving ourselves so short that we can’t sustain our own industrial base to compete either economically or militarily.

The solution is domestic gas reservation, at a fixed price if necessary, of up to 200Pj per annum over the next twenty years. Take it from China and the price goes up in Asia costing us nothing.

In the midst of Cold War 2.0 it is preposterous to describe this as soverign risk. The risk is clearly to the sovereign as displayed in the Solomon Islands today.

Advertisement

Why are we committing this peculiar form of national suicide? This:

Everyone wondered whether there was some connection between the government’s direction and its financial indebtedness to the fossil fuel industry. But no one could prove it. Why? Because the Commonwealth doesn’t have real time disclosure of political donations.

Only now, long after the public’s attention has moved on, have those suspicions been confirmed. Thanks to the donations data recently made public on the Australian Electoral Commission site, we know that fossil fuel companies — and the gas industry in particular — were giving generously to both major parties at the time, a whopping $1,329,754 to be precise, with just over half of this from the gas industry.

The Coalition got the lion’s share ($731,534), although Labor collected the not-insignificant sum of $598,220.

If you add to the Coalition’s total for that year the just over $1 million the LNP harvested from fossil fuel via its fundraising entity Cormack, the Coalition’s indebtedness to gas, coal and mining in the 2020-21 period swells to $1,735,048.

Is this proof of corruption? No, but it certainly gives reason for voters to consider whether corruption has taken place. To wit, whether the gas-led recovery policy was designed and intended by the Morrison government to serve the public interest or private ones.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.