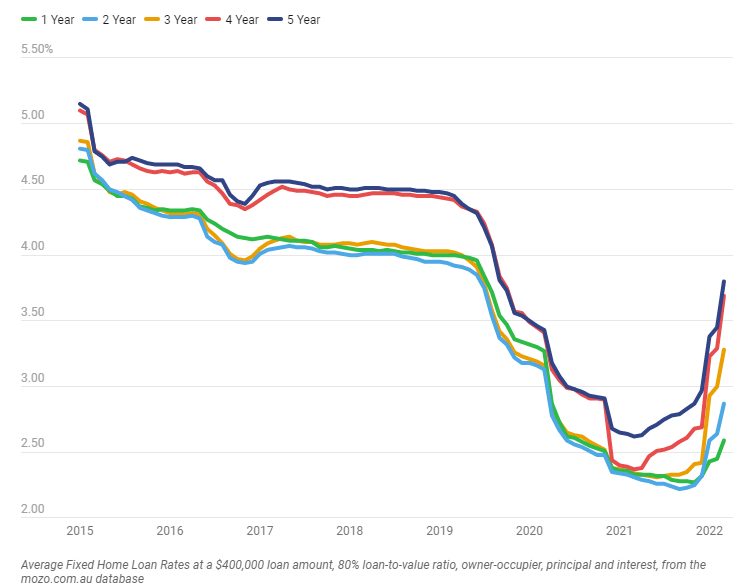

Earlier today I showed how fixed rate mortgages have ratcheted up, rising by 14% (1 year) to 45% (five year) since bottoming last year:

Now Citi banking analyst Brendan Sproules is warning that average mortgage repayments could jump by between 25% and 35% as special home loan deals reset:

While fixed rates protect borrowers from higher repayments, blunting the initial effect of rate rises, when fixed rate loans expiring in the second half of next year roll over, the annual interest repayment of around $27,600 on an average $620,000 mortgage at a 2 per cent rate would jump to an annual repayment of $34,600 assuming a variable rate of 3.75 per cent…

Before the pandemic, around 60 per cent of new mortgages were on variable rates and 40 per cent were fixed. But this flipped to around 80 per cent of new loans being on fixed rates during last year. A relatively large amount of banks’ overall mortgage books have been originated in the past 18 months, as refinancing surged.

“Here lies the conundrum for Dr Lowe,” Mr Sproules wrote to Citi clients over the weekend. “If the RBA raise rates too fast, 40 per cent of the book might be set for a rude shock when their fixed term (typically two years) expires.”

Advertisement

CBA head of Australian economics, Gareth Aird, made similar warnings last month:

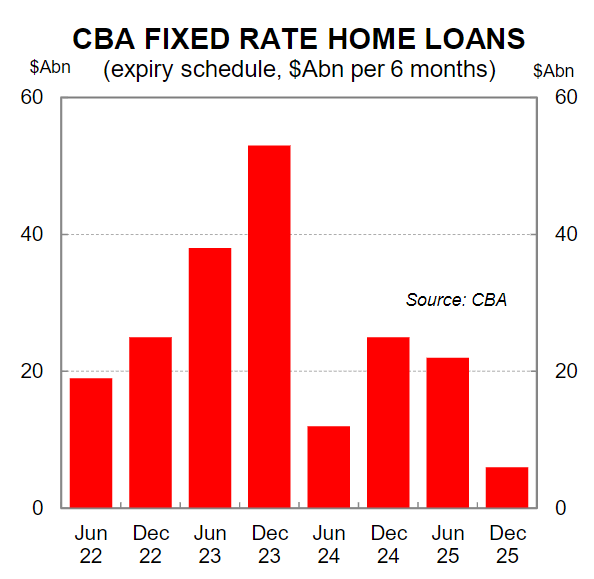

The fixed rate home loan expiry schedule means that over the next two years a very significant proportion of home loans will expire (see chart below for the CBA fixed rate loan book expiry profile). Based on CBA’s fixed rate home loan expiry schedule and share of the market there is likely to be around $A500bn of fixed rate mortgage loans expiring in Australia over the next two years.

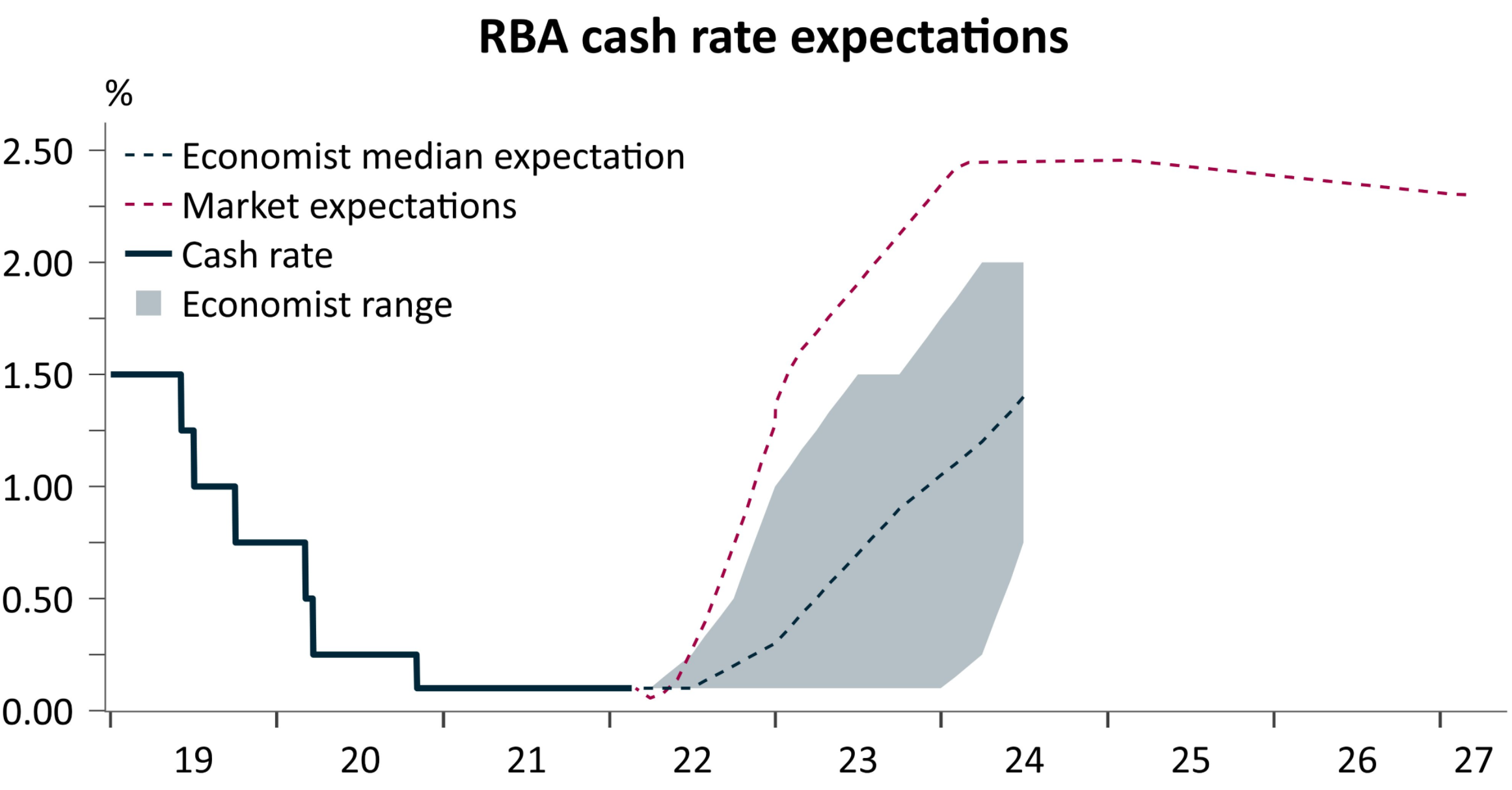

As shown in the next chart, the median economist is tipping the cash rate to rise by around 1.25% by 2024, whereas markets are tipping rates to rise by around 2.5%:

Advertisement

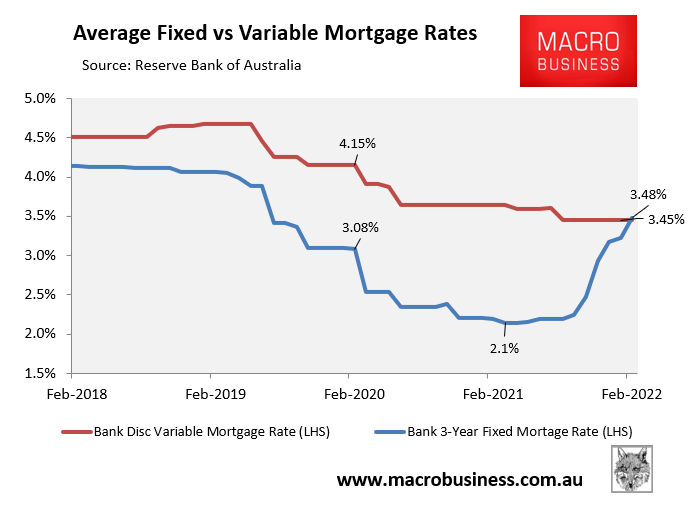

Currently, the average discount variable mortgage rate is tracking at 3.45% – well above the fixed rates taken out earlier in the pandemic:

Advertisement

Thus, if economists and/or the market is correct, many fixed rate borrowers will face skyrocketing repayments when it comes time to refinance. In turn, the increasing repayment burden (for new and refinancing borrowers) would hammer house prices, and dramatically slow the economy.

For these reasons, I cannot see the RBA lifting the cash rate by more than 1.0%, since the impact would be too severe.

Therefore, expect shallow rate rises and not until the end of the year, given the the mortgage market is already tightening independent of the RBA.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.