By Gareth Aird, head of Australian economics at CBA. My view is that the RBA won’t lift rates until wage growth lifts above 3% (from 2.2% as at the September quarter), which suggests a June rate hike is too early. That said, Gareth Aird has access to CBA’s internal data, which shows wage pressures building fast. So if this translates into the official wage data, then RBA could hike early.

Key Points:

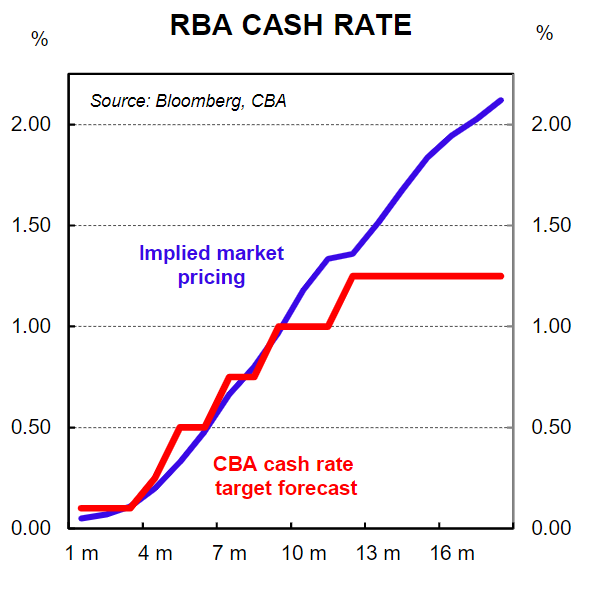

- We shift our central scenario for the first hike in the cash rate target to June 2022 (from August 2022).

- We expect the RBA to move to an explicit hiking bias at the May 2022 Board meeting.

- Our forecast profile now has the cash rate at 1.0% by end‑2022 (a 15bp increase in June, followed by two 25bp increases in Q3 22 and a further 25bp in Q4 22).

- We expect one further 25bp rate hike in Q1 23 that takes the cash rate to 1.25% ‑ our estimate of the neutral cash rate.

- The significant fixed rate loan expiry schedule over the next two years means that we do not expect the RBA to take monetary policy into contractionary territory.

A better understanding of the RBA’s reaction function

On Friday 11 February 2022 RBA Governor Lowe appeared before the House of Representatives Standing Committee on Economics.

The Governor was asked by the Chair of the Committee:

“Do you feel that you are now on track to sustainably getting inflation back on target, or would you like to see at least one or two more quarters before you could say that?”

The Governor replied:

“As I said in my introductory remarks, we can’t draw the conclusion yet. Aggregate wage growth is 2.3 or 2.4. That was the rate it was before the pandemic, and that delivered inflation below two per cent. The supply‑side problems I think are going be resolved. They talk about how electronics prices will come back down again. I don’t think car prices are going to keep going up at seven per cent a year. The board wants to see how those issues resolve. Is the stronger labour market going to translate to higher wages? Remember, we had a period of four per cent unemployment in New South Wales and Victoria a few years ago, and aggregate wages growth didn’t move. In WA now the unemployment rate is 3½ and wages are moving up, but not that much. So we want to see how that goes, and I think these uncertainties are not going to be resolved quickly. We are prepared to take the time, particularly given our inflation history and the prospect of low unemployment. Another couple of CPIs would be good to see.”

We interpret this statement to mean that the RBA will conclude that inflation is “sustainably within the target range” if the next two inflation prints are in line with their forecasts (provided wages growth continues to accelerate and the labour market further tightens, as we expect).

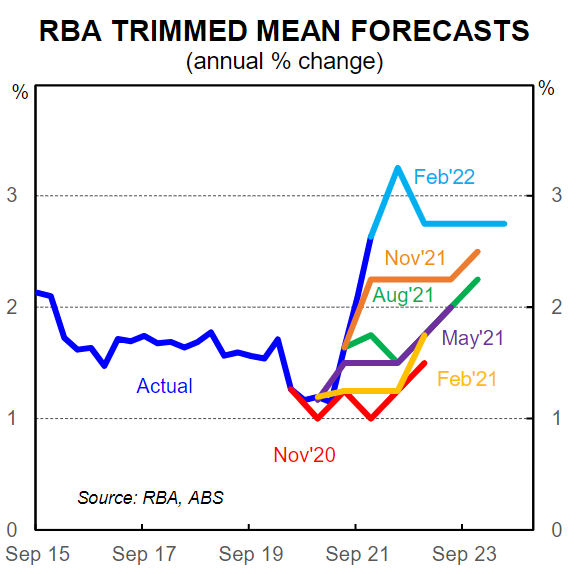

Based on the Governor’s comments last week we believe the RBA’s central scenario and reaction function is consistent with a first increase in the cash rate in August 2022 (the Q1 22 CPI prints 27 April and Q2 22 CPI prints 27 July). But the RBA’s forecast for inflation is different to ours.

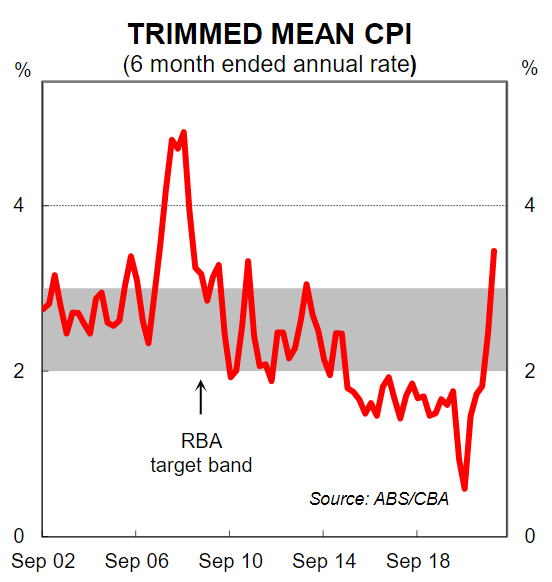

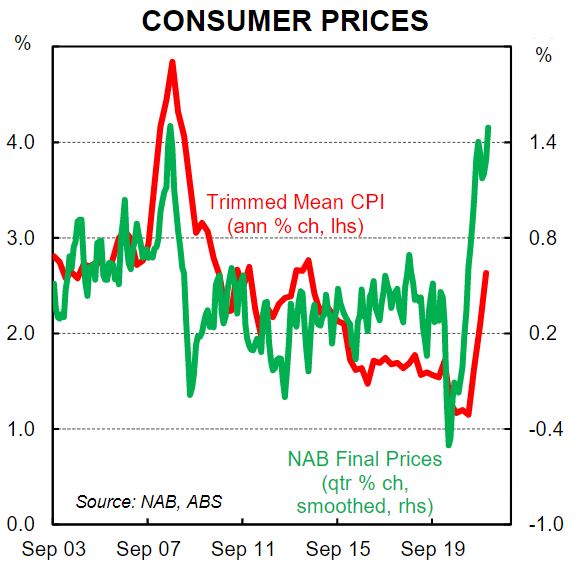

The RBA has forecast trimmed mean inflation to be 3¼%/yr at mid‑22, which implies quarterly increases of 0.75% in both Q1 22 and Q2 22. That is significantly below our forecast for underlying inflation.

Our preliminary estimate is for the Q1 22 trimmed mean CPI to increase by 1.2%/qtr, which would take the annual rate to 3.5% (a six month annualised pace of 4.4%).

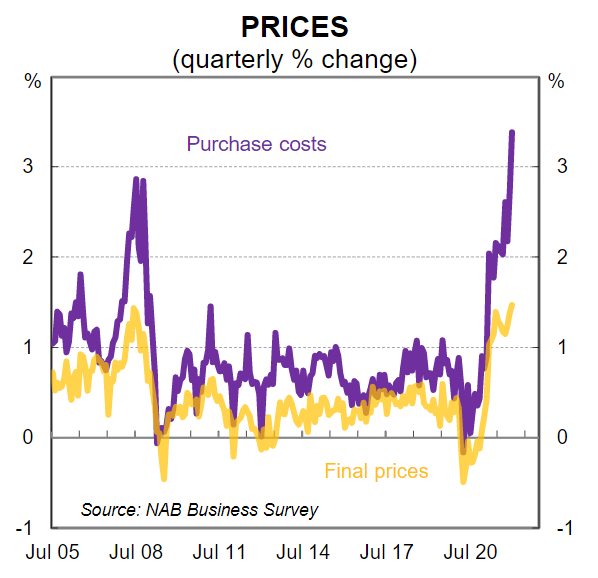

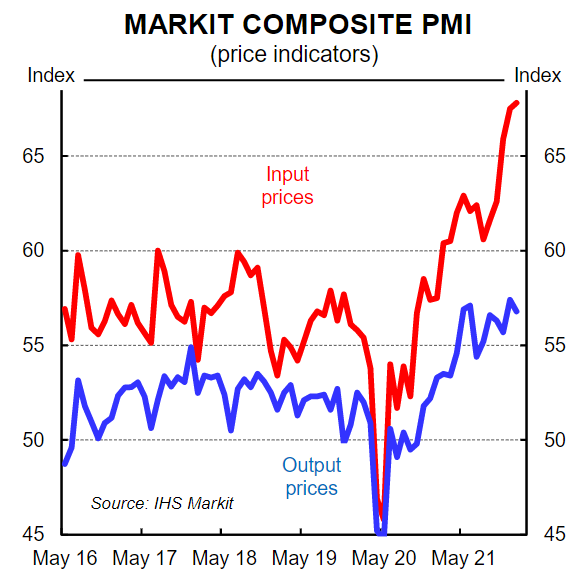

We are very comfortable with our expectation that the Q1 22 underlying inflation data will be a lot stronger than the RBA’s forecast. Private surveys that contain inflation gauges indicate the inflationary pulse has accelerated so far in 2022 (see charts below). Input costs have risen very swiftly and this is feeding through to faster growth in output prices.

If the Q1 22 CPI prints in line with our forecast the RBA will not need an additional CPI to conclude that inflation is “sustainably within the target range”. The RBA will simply need to be satisfied that wages growth is moving towards the desired levels.

Why not lift the cash rate in May?

The Q1 22 CPI prints the week before the May RBA Board meeting. Three days after the May Board meeting the RBA will release updated economic forecasts in their quarterly Statement of Monetary Policy (SMP).

On the surface the May Board meeting looks like a logical time for the RBA to commence a tightening cycle based on our expectation for the Q1 22 CPI. But the RBA is likely to wait for one final piece of data before increasing the cash rate – the Q1 22 Wage Price Index (WPI) that prints 18 May.

We expect the Q1 22 WPI to indicate wages growth is running at a six month annualised pace of over 3%. Such an outcomes will mean the RBA can conclude that inflation is “sustainably within the target range” at the June Board meeting and therefore commence normalising the cash rate.

Our expectation is that the RBA will shift to an explicit hiking bias at the May Board meeting following a big upside surprise on the Q1 22 underlying CPI.

We anticipate that the Governor’s post meeting Statement from the May 2022 Board meeting will contain words to the effect of: “if the upcoming wages data is consistent with inflation sustainably within the target range the Board will consider the case for higher interest rates at the June Board meeting”.

What does the tightening cycle look like?

Picking the exact timing of rate hikes through a tightening cycle is false precision. But economists need a forecast profile. Our central scenario sees the RBA deliver a 15bp increase in the cash rate in June 2022, which would take the cash rate to 0.25%. We expect that to be followed by two 25bp increases in Q3 22 and a further 25bp hike in Q4 22, which would take the cash rate to 1.0% by end‑22. We expect one further 25bp rate hike in Q1 23 that takes the cash rate to 1.25% ‑ our estimate of the neutral cash rate.

At this stage we do not anticipate that the RBA will need to take monetary policy to a contractionary setting.

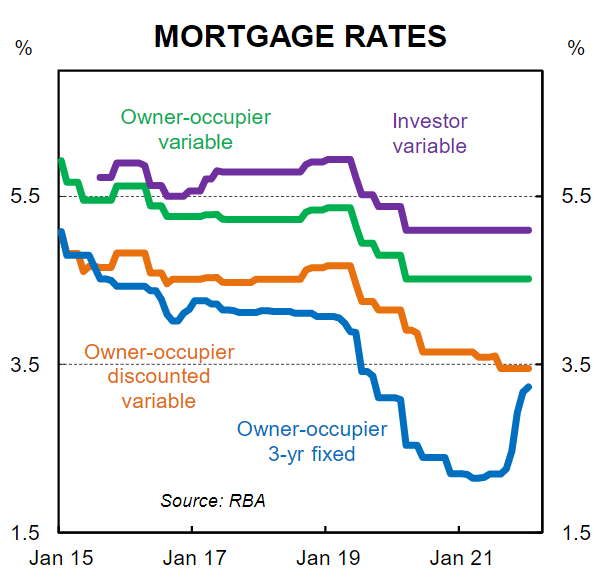

The economy is not static. Interest rate increases will generate changes in behaviour, which in turn will impact economic outcomes. For context, we estimate there are over one million home borrowers who have never experienced an increase in mortgage rates.

The RBA will need to assess the impact of rate hikes on the economy, particular the household sector and the housing market, as they move through the tightening cycle. This means the central bank is likely to be patient and a gradual and shallow rate hike trajectory is our base case.

We expect the RBA to stop their tightening cycle in early 2023 when the cash rate hits 1.25%. At that point the annual rate of wages growth should be comfortably above 3%. But this does not mean that the RBA will continue to raise rates. Indeed we believe they will not need to.

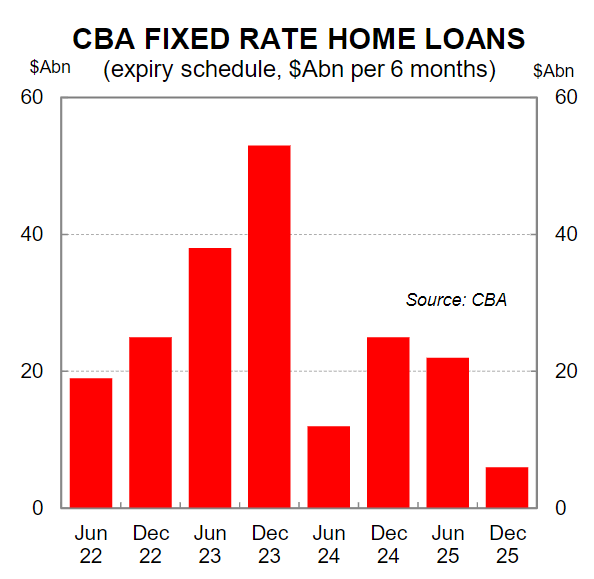

The fixed rate home loan expiry schedule means that over the next two years a very significant proportion of home loans will expire (see chart below for the CBA fixed rate loan book expiry profile). Based on CBA’s fixed rate home loan expiry schedule and share of the market there is likely to be around $A500bn of fixed rate mortgage loans expiring in Australia over the next two years.

We estimate the average loan rate of the fixed rate mortgages currently in the system sits between 2.25% and 2.5%. This rate is expected to be significantly lower than both the standard variable rate and fixed rates over H2 22 and 2023. As a result, borrowers rolling off fixed rates will be refinancing their loans at a materially higher interest rate, which will have a significant impact on the interest cost of debt and household finances.

The peak expiry of fixed rate home loans occurs through 2023. This means that a natural tightening in financial conditions will happen through 2023 even if the RBA remains on hold following its final anticipated rate hike in Q1 23.

The economy is also expected to deal with the headwind of an orderly correction in home prices in 2023. Our forecast is for a 10% decline in national dwelling prices over 2023 as higher interest rates weigh on the demand for credit.

In summary there will be a variety of forces at work on the Australian economy in 2023 that will exert a cooling effect on demand, which in turn will alleviate inflation pressures. We therefore do not agree with market pricing that the RBA will continue to hike the cash rate throughout 2023.

Of course there is a risk that the economy requires the cash rate to be taken into contractionary territory over 2023. But that is not our base case.